Disliked{quote} Report on GATE development So Far 23 Sept to 10 Oct 2025. Ideally GATE development shows improvement week over week which it is. The caveat is this is 100% Gemini LLM managing the trading with myself defining the boundaries it has to work in. Comparative Trading Report: Sept 24 – Oct 3 vs. Oct 6 – Oct 10, 2025 Executive Summary This report analyses and compares the trading performance across two distinct periods: Period 1 (24 Sept – 3 Oct 2025) and Period 2 (6 Oct – 10 Oct 2025). The analysis reveals a significant improvement in performance...Ignored

Trading Performance Analysis: GATE SPX500

(we still have one more day of trading)

https://www.forexfactory.com/bl4ckp3n9u1n/264212

My goal is to bring the account back to break even next week as this started off with $200. At the time of posting the Balance is $187.57 (-$12.43 profit)

Report Date: October 16, 2025

Subject: Comparative Performance Review for Weeks of Oct 6-10 and Oct 13-16, 2025.

Instrument: SPX500

Strategy: "GATE" Gemini Algorithmic Trading System (Versions v9.x - v11.x)

1.0 Executive Summary

This report provides a comparative analysis of the trading performance for two consecutive periods: Week 1 (October 6-10, 2025) and Week 2 (October 13-16, 2025).

Week 1 was a challenging period characterized by high trading frequency, significant drawdown, and a net loss of -$7.73. Performance was volatile, with the "Risk Sentinel" module frequently intervening, resulting in numerous small to medium-sized losses.

Week 2 demonstrated a significant performance turnaround, concluding with a net profit of +$13.00. This positive shift correlates with the deployment of an updated trading algorithm (GATE v11.x). While this week also experienced a substantial single-trade loss, the system's ability to secure larger and more consistent wins resulted in a superior profit factor and overall positive return. The data suggests the strategy update in Week 2 led to more effective profit capture and potentially improved trade management, despite facing similar market volatility.

2.0 Performance Analysis: Week 1 (October 6 - 10, 2025)

This period was characterized by intense, high-frequency trading. The system, primarily running on GATE versions 9 and 10, actively managed a fluctuating market, leading to a mixed but ultimately negative result.

2.1 Key Performance Metrics (Week 1)

Starting Balance: $182.30

Ending Balance: $174.57

Net Profit / Loss: -$7.73

Total Closed Trades: 71

Winning Trades: 37 (52.1%)

Losing Trades: 34 (47.9%)

Win Rate: 52.1%

Gross Profit: $39.54

Gross Loss: -$47.27

Profit Factor: 0.84

Average Win: $1.07

Average Loss: -$1.39

Largest Win: $6.78 (Oct 10)

Largest Loss: -$7.95 (Oct 7)

2.2 Narrative Analysis (Week 1)

- Trading Activity: The system executed a high volume of 71 trades over five days. Lot sizes were small, typically ranging from 0.01 to 0.03, indicating a scalping or high-frequency strategy.

- Strategy Behavior: The trading log reveals several distinct exit reasons:

- [tp ...]: Standard take-profit orders, which accounted for most winning trades.

- [sl ...]: Stop-loss orders, responsible for the two largest losses of the week (-7.95 and −7.95 and −5.11).

Risk Sentinel: This appears to be a dynamic risk management module that closed a significant number of trades. These exits were predominantly losses, suggesting the module is designed to cut trades before they hit a predefined stop-loss when market conditions turn unfavourable. - GPO (General Pattern Orders): Exits like "M5_V_SHAPE" and "meta_failed" indicate a pattern-based logic is also at play.

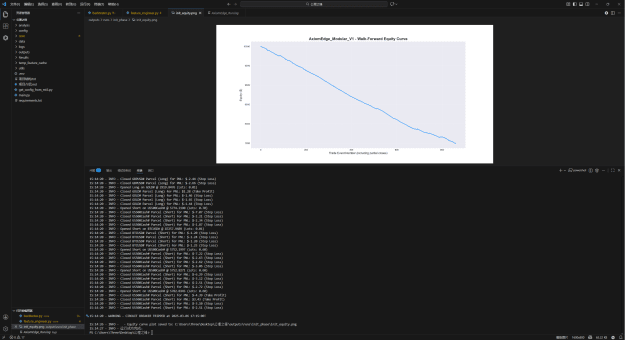

- Performance Trajectory: The account experienced a significant drawdown mid-week, particularly on October 7th, with the largest loss of -7.95. The week concluded with a highly volatile session on October 10th, where the system booked three large wins (7.95.The week concluded with a highly volatile session on October 10th, where the system booked three large wins (5.40, $6.78, 3.07) but also a significant loss(−3.07) but also a significant loss(−5.11), ultimately failing to recover the week's losses. A Profit Factor of 0.84 signifies that for every dollar of risk, the system only generated $0.84 in profit, confirming an unprofitable performance.

3.0 Performance Analysis: Week 2 (October 13 - 16, 2025)

This period marked a notable shift in performance. A key observation is the update of the trading algorithm, with comments changing from "GATE v10.x" to "GATE v11.0.x" starting October 14th.

3.1 Key Performance Metrics (Week 2)

Starting Balance: $174.57

Ending Balance: $187.57

Net Profit / Loss: +$13.00

Total Closed Trades: 35

Winning Trades: 20 (57.1%)

Losing Trades: 15 (42.9%)

Win Rate: 57.1%

Gross Profit: $40.82

Gross Loss: -$27.82

Profit Factor: 1.47

Average Win: $2.04

Average Loss: -$1.85

Largest Win: $6.25 (Oct 14)

Largest Loss: -$8.90 (Oct 14)

3.2 Narrative Analysis (Week 2)

- Trading Activity: Trading frequency decreased significantly to 35 trades over four days, roughly half the volume of the previous week. This suggests the newer version of the algorithm may be more selective in its trade entries.

- Strategy Behaviour:

- System Update: The clear transition to GATE v11.x is the most critical factor. This update appears to have directly influenced the trading outcomes.

- Risk vs. Reward: The average win of 2.04 is nearly double that of Week1 (2.04 is nearly double that of Week 1 (1.07), while the average loss ($1.85) remained proportionally higher but was overcome by the improved winning performance.

- Major Loss Event: The system incurred its single largest loss of the entire two-week period (-$8.90 on Oct 14). However, unlike in Week 1, the system recovered from this drawdown effectively. It immediately followed with a series of strong wins, including the week's largest gain of $6.25.

- Performance Trajectory: The week started with a few losing trades but quickly found its footing after the system update. Despite the large "Risk Sentinel" loss on October 14th, the system consistently generated profits, leading to a steady equity curve growth for the remainder of the week. The Profit Factor of 1.47 indicates a healthy, profitable strategy where every dollar risked generated $1.47 in return.

4.0 Comparative Analysis & Conclusion

Week 1 (Oct 6-10)

Week 2 (Oct 13-16)

Net Profit / Loss:

Week 1:-$7.73

Week 2: +$13.00

Change: + $20.73

Profit Factor

Week 1: 0.84 (Unprofitable)

Week 2: 1.47 (Profitable)

Change: + 75%

Win Rate

Week 1: 52.1%

Week 2: 57.1%

Change: + 5.0%

Total Trades

Week 1: 71

Week 2: 35

Change: - 50.7%

Average Win$

Week 1: 1.07

Week 2: $2.04

Change: + 90.7%

Average Loss

Week 1:-$1.39

Week 2: -$1.85

Change: - 33.1%

Largest Loss

Week 1: -$7.95

Week 2: -$8.90

Change: - 11.9%

Key Findings:

- Profitability: The primary difference is the shift from a net loss to a substantial net profit. Week 2 outperformed Week 1 by $20.73.

- Strategy Efficacy (Profit Factor): The most significant improvement was the Profit Factor, which moved from an unprofitable 0.84 to a robust 1.47. This indicates the GATE v11.x system is fundamentally more effective at generating profits relative to its losses.

- Trade Selectivity: The 50% reduction in trade frequency suggests GATE v11.x employs a more refined entry logic, avoiding the lower-quality setups that may have contributed to the "churn" and net loss in Week 1.

- Reward-to-Risk Profile: While the average loss increased in Week 2, the average win nearly doubled. This improved reward profile was the key driver of profitability, as winning trades contributed more significantly to the bottom line, easily offsetting the losses.

Conclusion:

The performance data strongly suggests that the upgrade to the GATE v11.x algorithm was a successful and pivotal event. While Week 1's strategy was active but inefficient, Week 2's strategy was more selective, resilient, and ultimately profitable. It successfully navigated market volatility to achieve a positive return, recovering from a significant loss that the prior week's system may have struggled with.