Attached Image (click to enlarge)

Whats your best money management method? 52 replies

How to flow with the order flow? 26 replies

Money Management / Risk Management 24 replies

Money management model for multiple strategy trading method 16 replies

Most popular money management method. 7 replies

Attached Image (click to enlarge)

https://www.forexfactory.com/attachm...l?d=1721753447

WWW.AVIELFOREXLEARNINGEDGE.COM

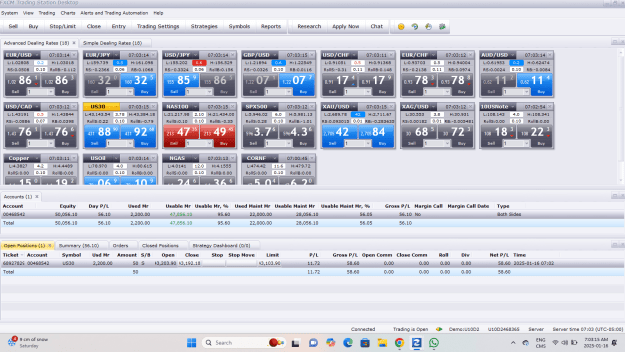

All SCREEN SHOTS show ALL Forex trades BEFORE and AFTER the FOREX Traes !!!

NOTE from BWM: This $50,000 US dollars FXCM UK Demo account was opened on January 15, 2025.

In the last 20 years, TOP FOREX traders rarely earn over 5% a month or 60% a year and NEVER more than 3 years in a row. There are reasons for this.

My students are expected to earn 5% a month under my guidance for 90 days, the length of my hands-on teaching.

Forex trading presents vast opportunities for profit through its high liquidity and leverage options. However, it also carries inherent risks, demanding a thorough understanding of market mechanics, disciplined trading strategies, and effective risk management. As a dynamic and complex financial market, Forex offers global challenges and rewards to participants.

WWW.AVIELFOREXLEARNINGEDGE.COM

News from around the world. Please CLICK on the link below.

https://finviz.com/news.ashx?v=2

5-Minute Chart of Dow 30 - Our X-Ray Photo - Please CLICK on the LINK below.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

Please sign up for our 90-day Forex Trading and Information course by sending E Transfer of 125.00 Canadian dollars to Tobyruth11@yahoo.com

"Trader", does not mean that the sole objective is to make money. The moment you come with money-making as the sole and only objective, you are out of the game anyway and part of the larger crowd which is unsuccessful

Do things that can identify you as a professional trader - learn the process, understand and follow risk management and position sizing. Be disciplined and understand that trading is a long haul.

Each day around 8:30 AM to 9:30 AM Eastern Standard Time, I determine whether we have RISK ON or OFF.

No indicator can do this just as no technical indicator can effectively predict what will happen moment to moment as one MAJOR fundamental fact whether GEOPOLITICAL or FINANCIAL or now SUPPLY CHAIN or some New Covid 19 variant can cause the markets to go down or up 500 points as the Dow 30 has been doing recently and will continue to do. This happens sometimes in one day so normal charting cannot work.

That is why my Unique Method of Forex trading developed in 2003 when I started trading Forex and later in 2012 when I added to my business model and started teaching my unique 100% proven method of Money Flow trading.

It is no longer possible to trade without a STOP LOSS.

A STOP LOSS of fewer than 100 PIPS is not a good strategy. That leads me to explain why most of the 95% of all Retail Forex Traders lose. They trade with small amounts of money and SCALP, making it almost impossible to make profits over one year because of the VIOLENT NATURE of the swings in the Asset Classes caused by world-changing events.

Each Forex Trade that you do should not risk more than 2% of your trading Capital and that is based on trading Capital of $50,000 US Dollars, INITIALLY learning on a $50,000 US Funds Demo account just as I did for three years before I made my first Real Funds Trade on March 9, 2006, 18 years ago.

PLEASE GO WITH THE MONEY FLOW

Let us review what we teach and why it works if YOU WORK.

Without your WORK, you are wasting your time and probably your money.

There is no such thing as Political Correctness here because we are here to teach and share our knowledge.

SO.... going back to our winning FORMULA for FOREX SUCCESS.

20% of the SUCCESS is yourself the Forex Trader.

20% of the SUCCESS is your EDGE, which we teach you, Money Flow Trading.

20% of the SUCCESS is control of your RISK (Your hard-earned money) Our UNIQUE RISK MANAGEMENT allows you to trade without worry, fear, and greed. Of course, we want to make sure that you have the right qualities to be a winning Forex Trader so our course is for three months, so we can teach you the right trading methods we can see your results and make adjustments without your FEAR OF LOSS of Real Money.

20% of the SUCCESS is using and understanding the USE of Technical Indicators which include not only the common ones. It consists of understanding supply and demand. Support and Resistance and the use of Pivot Points which you can see daily on our daily charts that cover ALL our Trade Plans which we also help you develop and explain WHY. We review These Winning Trade Plans every three months or earlier if market circumstances require that.

20% of the SUCCESS is the FUNDAMENTALS, which are much more than Data released daily worldwide. It includes reports and articles extremely well researched as you can see from this article that explains why the TREND in the Equity Markets especially in North America is DOWN. By understanding the difference between PERCEPTIONS (MARKETS) and REALITY, you have a good handle on REALITY before the MASSES do and are not surprised when events eventually unfold.

When successful traders aren't trading, they are researching, developing, and innovating. When unsuccessful traders aren't Forex trading, they stare at screens and force trades. There is nothing better for trading psychology than being at the cutting edge of a growing business.

Quoting perfectionis

What are the key principles of risk management in forex trading, especially considering the influence of central banks and market sentiment? How do you determine risk-on or risk-off conditions, and how does it affect currency flows? Considering both fundamental factors and technical indicators, what impact could the Britain election have on forex markets? The election took place on Thursday, July 4, 2024.

The answers to your excellent questions will happen by you registering to post on Forex Factory so you can then post your questions or comments on my thread.

THE RETAIL SALES NUMBER FOR DECEMBER 2024 WILL BE RELEASED at 8:30 AM.

If the number is low the PERCEPTION, not the REALITY which they cannot do practically because it will lead to more inflation. Most commercial and retail Forex traders have no idea what QE (Quantative Easing) and QT (Quantative Tightning) do to CAUSE INFLATION.

If you want to call me and discuss it further I offer direct contact by calling me at 1 819 275 7780. Please sign up for my service by sending a Bank E Transfer in Canadian funds to Tobyruth11@yahoo.com

The fee is 125.00 dollars in Canadian funds from your bank account by E-Transfer.

We believe in a hands-on approach at a more than reasonable cost for a comprehensive service.

We can all see by looking at the link below, the 5 Minute Chart of Dow 30, the patterns keep repeating and you all have a chance if you want to learn to become very wealthy over the next year by signing up. You have zero risk as the information that you will have access to is invaluable.

Here is the link.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

LOOK AT THE PATTERN OF TODAY and Every Forex trading day from Sunday at 2:00 AM Eastern Standard Time in Europe to 10:00 AM Eastern Standard Time when North American Equity Markets start trading at 9:30 AM Eastern Standard Time on Monday.

This X-RAY and PATTERN repeats between Sunday and Friday at 5:00 PM Eastern Standard Time when All Forex Trading stops until 3:00 PM Eastern Standard Time when New Zealand opens for trading followed by Asia at 8:00 PM, Europe at 2:00 AM and North America at 9:30 AM.

ABSOLUTE FORTUNES ARE POSSIBLE ONCE YOU UNDERSTAND !!! And you show that you have the DISCIPLINE by your results to CONTROL your FEAR, GREED and EGO !!! The markets are always right until they are not.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

If you want to call me and discuss it further I offer direct contact by calling me at 1 819 275 7780. I will spend a minimum of 30 minutes with you on the telephone to answer any of your questions at NO COST TO YOU. Please sign up for my service by sending a Bank E Transfer of Canadian funds to Tobyr[email protected]

5-Minute Chart of Dow 30 - Our X-Ray Photo - Please CLICK on the LINK below.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

NOTE: PLEASE REGISTER TO POST ON THIS THREAD. WE CAN THEN HELP YOU BECOME SKILLED WITH 24/7 Guidance. It costs nothing to register and takes less than 5 minutes.

CLICK ON THE LINK ABOVE AND LOOK AT THE REPEATING X-RAY Each Forex Trading Day.

You Need To Act So I Can Help You DISCOVER if you have the SKILLS to become a winning Forex trader using LEVERAGE of 100 to 1.

Our Forex Trade Plan from January 1, 2025, until March 31, 2025, is SHORT 50 UNITS of DOW 30, SHORT 50 UNITS of SP500, Go LONG 100 ounces of Gold and 5000 Ounces of Silver. I usually choose one of the MAJOR Currency Pairs to SHORT or GO LONG ON.

WWW.AVIELFOREXLEARNINGEDGE.COM

CLICK ON THIS LINK - IT IS THE 5-Minute Chart Of Dow 30. See how the KNOWN PATTERNS REPEAT -

https://finviz.com/futures_charts.ashx?p=i5&t=YM

The Dow Jones 30 (DJIA) went UP OVER 700 points YESTERDAY when the actual trading started and 4:00 PM when the markets closed.

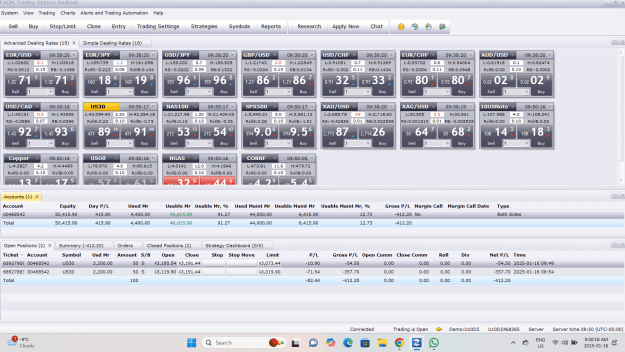

I was travelling between Montreal and my home in Riviere Rouge, Quebec and I did no Forex trades HOWEVER, I opened a NEW DEMO account and have already put on my FIRST FOREX TRADE for today with a PROFIT TARGET of $500.00.

Attached Image (click to enlarge)

https://www.forexfactory.com/attachm...l?d=1722691331

THE WRONG PERCEPTION WORLDWIDE CONTINUED IN THE STOCK MARKETS.

WHY? Most Traders and EXPERTS do not understand ECONOMICS. READ THE JANUARY 2025 JOHN HUSSMAN NEWSLETTER.

HE CALLED IT PERFECTLY. RATE CUTS CANNOT STOP A RECESSION AND OTHER SERIOUS PROBLEMS IN THE MANIPULATED STOCK MARKETS.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

LOOK AT THE PATTERN OF the last 24 hours as it repeats every day which is why my results are so spectacular and PROFITABLE.

CLICK ON THE LINK ABOVE AND SIGN UP OR CALL ME FOR A ONE-ON-ONE 30-minute discussion. Thanks - BWM

DislikedGood day Bruce, What happen to your last demo account since January 12,2025 ? Why did you start a new demo account? It was opened at the end of December and you did not even trade 30 days with it. Keep me posted. ThanksIgnored

Attached Image (click to enlarge)

https://www.forexfactory.com/attachm...l?d=1721753447

WWW.AVIELFOREXLEARNINGEDGE.COM

All SCREEN SHOTS show ALL Forex trades BEFORE and AFTER the FOREX Traes !!!

NOTE from BWM: This $50,000 US dollars FXCM UK Demo account was opened on January 15, 2025.

In the last 20 years, TOP FOREX traders rarely earn over 5% a month or 60% a year and NEVER more than 3 years in a row. There are reasons for this.

My students are expected to earn 5% a month under my guidance for 90 days, the length of my hands-on teaching.

Forex trading presents vast opportunities for profit through its high liquidity and leverage options. However, it also carries inherent risks, demanding a thorough understanding of market mechanics, disciplined trading strategies, and effective risk management. As a dynamic and complex financial market, Forex offers global challenges and rewards to participants.

WWW.AVIELFOREXLEARNINGEDGE.COM

News from around the world. Please CLICK on the link below.

https://finviz.com/news.ashx?v=2

5-Minute Chart of Dow 30 - Our X-Ray Photo - Please CLICK on the LINK below.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

Please sign up for our 90-day Forex Trading and Information course by sending E Transfer of 125.00 Canadian dollars to Tobyruth11@yahoo.com

"Trader", does not mean that the sole objective is to make money. The moment you come with money-making as the sole and only objective, you are out of the game anyway and part of the larger crowd which is unsuccessful

Do things that can identify you as a professional trader - learn the process, understand and follow risk management and position sizing. Be disciplined and understand that trading is a long haul.

Each day around 8:30 AM to 9:30 AM Eastern Standard Time, I determine whether we have RISK ON or OFF.

No indicator can do this just as no technical indicator can effectively predict what will happen moment to moment as one MAJOR fundamental fact whether GEOPOLITICAL or FINANCIAL or now SUPPLY CHAIN or some New Covid 19 variant can cause the markets to go down or up 500 points as the Dow 30 has been doing recently and will continue to do. This happens sometimes in one day so normal charting cannot work.

That is why my Unique Method of Forex trading developed in 2003 when I started trading Forex and later in 2012 when I added to my business model and started teaching my unique 100% proven method of Money Flow trading.

It is no longer possible to trade without a STOP LOSS.

A STOP LOSS of fewer than 100 PIPS is not a good strategy. That leads me to explain why most of the 95% of all Retail Forex Traders lose. They trade with small amounts of money and SCALP, making it almost impossible to make profits over one year because of the VIOLENT NATURE of the swings in the Asset Classes caused by world-changing events.

Each Forex Trade that you do should not risk more than 2% of your trading Capital and that is based on trading Capital of $50,000 US Dollars, INITIALLY learning on a $50,000 US Funds Demo account just as I did for three years before I made my first Real Funds Trade on March 9, 2006, 18 years ago.

PLEASE GO WITH THE MONEY FLOW

Let us review what we teach and why it works if YOU WORK.

Without your WORK, you are wasting your time and probably your money.

There is no such thing as Political Correctness here because we are here to teach and share our knowledge.

SO.... going back to our winning FORMULA for FOREX SUCCESS.

20% of the SUCCESS is yourself the Forex Trader.

20% of the SUCCESS is your EDGE, which we teach you, Money Flow Trading.

20% of the SUCCESS is control of your RISK (Your hard-earned money) Our UNIQUE RISK MANAGEMENT allows you to trade without worry, fear, and greed. Of course, we want to make sure that you have the right qualities to be a winning Forex Trader so our course is for three months, so we can teach you the right trading methods we can see your results and make adjustments without your FEAR OF LOSS of Real Money.

20% of the SUCCESS is using and understanding the USE of Technical Indicators which include not only the common ones. It consists of understanding supply and demand. Support and Resistance and the use of Pivot Points which you can see daily on our daily charts that cover ALL our Trade Plans which we also help you develop and explain WHY. We review These Winning Trade Plans every three months or earlier if market circumstances require that.

20% of the SUCCESS is the FUNDAMENTALS, which are much more than Data released daily worldwide. It includes reports and articles extremely well researched as you can see from this article that explains why the TREND in the Equity Markets especially in North America is DOWN. By understanding the difference between PERCEPTIONS (MARKETS) and REALITY, you have a good handle on REALITY before the MASSES do and are not surprised when events eventually unfold.

When successful traders aren't trading, they are researching, developing, and innovating. When unsuccessful traders aren't Forex trading, they stare at screens and force trades. There is nothing better for trading psychology than being at the cutting edge of a growing business.

Quoting perfectionis

What are the key principles of risk management in forex trading, especially considering the influence of central banks and market sentiment? How do you determine risk-on or risk-off conditions, and how does it affect currency flows? Considering both fundamental factors and technical indicators, what impact could the Britain election have on forex markets? The election took place on Thursday, July 4, 2024.

The answers to your excellent questions will happen by you registering to post on Forex Factory so you can then post your questions or comments on my thread.

THE RETAIL SALES NUMBER FOR DECEMBER 2024 WILL BE RELEASED at 8:30 AM.

If the number is low the PERCEPTION, not the REALITY which they cannot do practically because it will lead to more inflation. Most commercial and retail Forex traders have no idea what QE (Quantative Easing) and QT (Quantative Tightning) do to CAUSE INFLATION.

If you want to call me and discuss it further I offer direct contact by calling me at 1 819 275 7780. Please sign up for my service by sending a Bank E Transfer in Canadian funds to Tobyruth11@yahoo.com

The fee is 125.00 dollars in Canadian funds from your bank account by E-Transfer.

We believe in a hands-on approach at a more than reasonable cost for a comprehensive service.

We can all see by looking at the link below, the 5 Minute Chart of Dow 30, the patterns keep repeating and you all have a chance if you want to learn to become very wealthy over the next year by signing up. You have zero risk as the information that you will have access to is invaluable.

Here is the link.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

LOOK AT THE PATTERN OF TODAY and Every Forex trading day from Sunday at 2:00 AM Eastern Standard Time in Europe to 10:00 AM Eastern Standard Time when North American Equity Markets start trading at 9:30 AM Eastern Standard Time on Monday.

This X-RAY and PATTERN repeats between Sunday and Friday at 5:00 PM Eastern Standard Time when All Forex Trading stops until 3:00 PM Eastern Standard Time when New Zealand opens for trading followed by Asia at 8:00 PM, Europe at 2:00 AM and North America at 9:30 AM.

ABSOLUTE FORTUNES ARE POSSIBLE ONCE YOU UNDERSTAND !!! And you show that you have the DISCIPLINE by your results to CONTROL your FEAR, GREED and EGO !!! The markets are always right until they are not.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

If you want to call me and discuss it further I offer direct contact by calling me at 1 819 275 7780. I will spend a minimum of 30 minutes with you on the telephone to answer any of your questions at NO COST TO YOU. Please sign up for my service by sending a Bank E Transfer of Canadian funds to Tobyr[email protected]

5-Minute Chart of Dow 30 - Our X-Ray Photo - Please CLICK on the LINK below.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

NOTE: PLEASE REGISTER TO POST ON THIS THREAD. WE CAN THEN HELP YOU BECOME SKILLED WITH 24/7 Guidance. It costs nothing to register and takes less than 5 minutes.

CLICK ON THE LINK ABOVE AND LOOK AT THE REPEATING X-RAY Each Forex Trading Day.

You Need To Act So I Can Help You DISCOVER if you have the SKILLS to become a winning Forex trader using LEVERAGE of 100 to 1.

Our Forex Trade Plan from January 1, 2025, until March 31, 2025, is SHORT 50 UNITS of DOW 30, SHORT 50 UNITS of SP500, Go LONG 100 ounces of Gold and 5000 Ounces of Silver. I usually choose one of the MAJOR Currency Pairs to SHORT or GO LONG ON.

WWW.AVIELFOREXLEARNINGEDGE.COM

CLICK ON THIS LINK - IT IS THE 5-Minute Chart Of Dow 30. See how the KNOWN PATTERNS REPEAT -

https://finviz.com/futures_charts.ashx?p=i5&t=YM

The Dow Jones 30 (DJIA) went UP OVER 700 points YESTERDAY when the actual trading started and 4:00 PM when the markets closed.

I was travelling between Montreal and my home in Riviere Rouge, Quebec and I did no Forex trades HOWEVER, I opened a NEW DEMO account and have already put on my FIRST FOREX TRADE for today with a PROFIT TARGET of $500.00.

Attached Image (click to enlarge)

https://www.forexfactory.com/attachm...l?d=1722691331

THE WRONG PERCEPTION WORLDWIDE CONTINUED IN THE STOCK MARKETS.

WHY? Most Traders and EXPERTS do not understand ECONOMICS. READ THE JANUARY 2025 JOHN HUSSMAN NEWSLETTER.

HE CALLED IT PERFECTLY. RATE CUTS CANNOT STOP A RECESSION AND OTHER SERIOUS PROBLEMS IN THE MANIPULATED STOCK MARKETS.

https://finviz.com/futures_charts.ashx?p=i5&t=YM

LOOK AT THE PATTERN OF the last 24 hours as it repeats every day which is why my results are so spectacular and PROFITABLE.

CLICK ON THE LINK ABOVE AND SIGN UP OR CALL ME FOR A ONE-ON-ONE 30-minute discussion. Thanks - BWM

Disliked{quote} Dear Domenico It is still active. Thanks for asking. I will post a SCREENSHOT LATER TODAY OR TOMORROW MORNING. I OPENED THIS ONE BECAUSE AM ABOUT TO FINALIZE A 100,000.00 Canadian dollars deposit to my Friedberg Direct account in Toronto shortly. Thanks for posting and asking. I am now at my new acquisition to be finalized by January 31, 2025 - Auberge Motel Godard. I am in Suite 117 and will send pictures later. Best regards, Bruce Warren Margolese. 514 777 1868 or 514 883 4361 or my landline in Riviere Rouge - 1 819 275 7780 WWW.AVIELFOREXLEARNINGEDGE.COM...Ignored

DislikedGood morning Everyone My only job on this thread is to help you learn and earn money. I cannot help unless I see your SCREEN SHOTS if you are still trading Forex using my UNIQUE method. To Lovelandpeacw, It is not legal to publish what you want to see and I do not know why you would even ask.? Only shareholders in Aviel Forex Learning Edge Corporation have that right. Have a nice weekend everyone !!! Bruce Warren Margolese President/CEO Aviel Forex Learning Edge Corporation 514 777 1868 514 883 4361 1 819 275 7780Ignored

Disliked{quote} SERIOUSLY!!!!! DO NOT you have your personal " LIVE " Account ?? In forex, we MUST NOT beat about the bush, we MUST come straight to the point. DEMO achievement is NOTHING in forex.Ignored