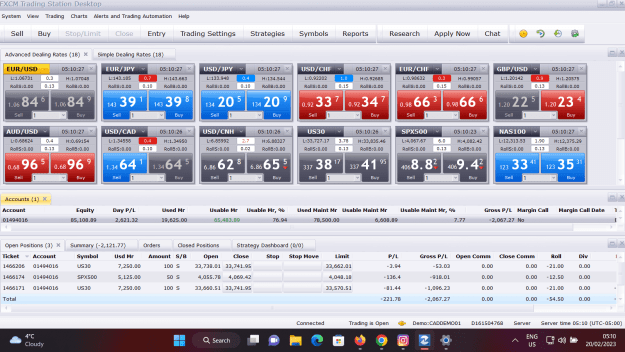

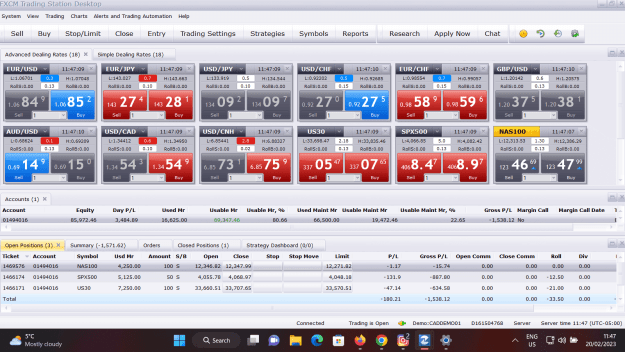

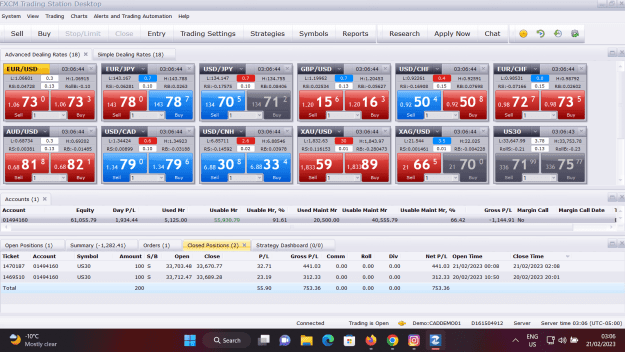

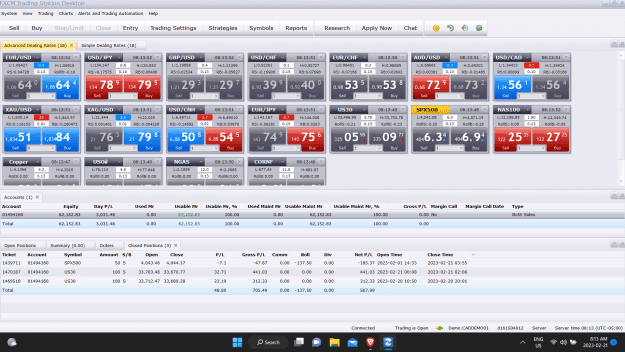

5 Minute Chart from FINVIZ of Dow 30 showing my prediction of last night is taking place as can be seen by my Forex trading results and the attached chart.

Central Banks, Recession landing risks, and why China is the issue to watch

The market is talking about a no-landing scenario – but should be watching what Central Banks are saying, and China’s position re Ukraine. The market remains vulnerable to recession and rising geopolitical tensions. They are very closely linked.

Blain’s Morning Porridge Feb 20th: Central Banks, Recession landing risks, and why China is the issue to watch

“A great landing in one when you can fly the plane the following day..”

This morning: The market is talking about a no-landing scenario – but should be watching what Central Banks are saying, and China’s position re Ukraine. The market remains vulnerable to recession and rising geopolitical tensions. They are very closely linked.

Last week the market was weighing up a soft-landing vs hard landing – to what degree a global recession might be skirted. Last Monday I was writing about Fairy Tales, specifically The Three Bears, and how the market is hoping we’ll be getting Baby Bear’s porridge: not too hot, not too cold – but just right. Bloomberg might have been reading me – my good chum Anthony Peters heard a TV anchor say: “They just murdered Goldilocks” when Fed Hawk Loretta Mester firmly laid down the line: “the fight against inflation is not done, and Fed Funds are heading higher.”

Pretty clear signal the Fed is not about to “pivot”… to use the most misused word of the decade! But, as usual, if all we are worried about are the trees of inflation, rates, yield curves and bond yields, then we are missing the real issues: the forest that is the global economy!

What external forces could trigger global slowdown and a deeper recession? For that you need to read the runes on yesterday’s spat between US secretary of State Anthony Blinken, and Chinese Diplomatic Chief Wang Yi in Munich. There is a lot of posturing underway. How geopolitics plays out is probably as important for global growth as what the Fed, ECB and Bank of England do on rates.

In recent days the market’s narrative has shifted. The commentariat is now talking about the “No Landing” scenario. This apparently means the global economy bounces around with high employment, annoyingly persistent (but not deadly) inflation, and no recessionary outcomes… Such a rosy outcome will occur on the back of China’s reopening, the resilience of western economies, easier energy costs, plus rising post-Covid consumption patterns all combining to power the global economy through this uncertain patch.

Really? What if that much anticipated China boost doesn’t happen because of a deepening Cold War?

This morning I participated in an economic expectations survey on Bloomberg giving the choice of a soft, hard, no-landing or the global economy flying into a mountainside.

None of these are necessarily where we end up… but sure its engaging stuff.. Apparently the no-landing outcome is the most likely…

To be honest.. No Landing sounds like a market convincing itself of upside when the picture remains one of economic grief. There are a couple of key economic determinants missing from the rosy “no landing” picture. We may well miss a global recession, but not because the market hopes for it. We need to understand why the market looks increasingly convinced a no-landing may happen.

In uncertain will-they/won’t-they markets – like today, and immediately following 2022, a dismal year for markets… there are lots of market participants desperately trying to get rich again and show just how clever their investment strategies are. In fervid miasmic markets it only takes a few days for the malarial pestilence of irrational exuberance to embed itself, triggering an outbreak of FOMO: fear of missing out.

Bear Rallies can be stubbornly persistent. Out there… somewhere east of common sense, there are still folk who think ButtCoin is going to $1 million, Cathie Wood is an investment genius, Elon Musk slashing the price of cheapest Tesla makes it the most valuable company on the planet, that Central Banks exist to save markets, and the Tooth Fairy runs a hedge fund. Dream on.

The reality? Work out what others are deliberately not seeing. Start with what central banks are actually doing:

Central banks have no incentive to cut rates early.

Inflation is not licked. Last week Fed members Lorretta Mester and James Bullard both made clear rates are going higher.

The only reason they are not more hawkish is to avoid a destabilising market panic.

Central banks are not just fighting inflation.

What they want is normalised rates to kick start the normal effective functioning of free market economies where investment goes into real job-creating, productivity enhancing, assets, rather than too-low rates creating a debt-fuelled tsunami of stock-buy backs and zombie firms.

Despite 2022 being the year of the fastest, steepest monetary tightening – interest rates are still negative in real terms vs inflation!

That is fundamentally unsustainable, but a host of market analysts are saying this is bond boom time…

What’s likey to set the market tone for the rest of 2023 is two factors:

What Central Banks do

How geopolitics play out

Big news over the weekend was the American’s saying the Chinese are going to start supplying Russia with ammunition. While Blinken and diplomat Yi were hurling insults at each other over balloons, the key issue is how to avoid a global slowdown a new cold war between China and the West would create.

It’s all about Ukraine. When the war broke out, almost one-year ago, the West expected widespread global condemnation of Russia for invading another nation to impose its will upon a people who had the temerity to democratically elect a government Putin disliked. Instead, much of the non-aligned world, and previously US leaning powers, particularly in the Gulf, chose not to support the West. They expected a tired and discredited US (embarrassed by the Afghan pull-out), the potential of a weaker dollar, and the Energy insecurity of Europe, would see the Russians quickly triumph, confirming a shift in global geo-political power away from the US towards China.

As we know, that’s not how it’s played out. Ukraine has proved the more resilient nation. Russia looks increasingly weak. One year after the war began Ukraine survives, and the West is gradually getting its act together to defend Ukraine. It looks likely to remain a long, drawn-out, bloody affair – dare I write stalemate?

The ball in now in China’s court.

If China declines to meaningfully supply Russia, that’s further humiliation for Putin but an opportunity for China to re-engage with the west – suiting President Xi’s kitchen-sink approach to reopening and growing the post-Covid Chinese economy. Not supplying Russia would also potentially suit the Chinese who will have seen how quickly Ukraine and Russia have burnt through war stocks, and how the Russians have underperformed on the field. China will have absorbed these lessons about command and control, and logistics, and factored these into its planning re Taiwan – and knows it will take years to effect changes in the People’s Liberation Army.

It’s a simple choice for Xi:

Supplying Russia would eat into China’s war-stocks, keep the West military focused on Ukraine, but cause economic damage to China’s growth via Western Sanctions.

Stepping back from supporting Russia gives China the prospect of stronger growth, reengagement with the West, and time to further refine its own forces and stocks ahead of “negotiations” on Taiwan.

The Russian planners (assuming there was much planning) assumed the West was hostage to Russian energy. The exceptionally mild winter has put paid to that. Over the weekend we were out for a walk wearing t-shirts, the daffodils are out a fortnight early, birds are nesting, and trees are budding. General Winter never showed up for Russia.

Although Europe will still struggle with energy insecurity – it’s not the only issue. There was a fantastic article on global chip supplies, and how a war in Taiwan will make Covid and Ukraine look like pleasant picnics. Now, that might get Xi thinking…

Uncertain times.. I am keeping my gold positions in place..

NEW YORK/BEIJING -- China's U.S. government bond holdings hit the lowest in over 12 years at the end of December, while its gold trove grew against a backdrop of American interest rate hikes and bilateral tensions.

Chinese holdings of Treasury securities fell for the fifth straight month in December to $867 billion, data published Wednesday by the U.S. Treasury Department shows.

The figure fell $173.2 billion, or 17%, in 2022 -- the biggest drop since 2016. China was not the only nation to sell down its Treasury holdings -- all foreign holdings of Treasury securities fell 6% in 2022 -- but its move was large.

The decline came as the U.S. Federal Reserve raised interest rates at a rapid pace to curb inflation. The benchmark 10-year yield had risen to nearly 4% at the end of December from around 1.5% a year earlier, and Chinese investors likely trimmed their holdings to avoid losses from a decrease in bond prices.

Geopolitical factors also played a role, market watchers said.

"Since the Russian invasion [of Ukraine], a move away from Treasurys ... would be an understandable reaction to the political developments," said a strategist at a U.S. asset manager, who sees the Chinese motivation as "wanting to maintain their independence and not be at risk."

After the February 2022 invasion, the U.S. moved to restrict Moscow's access to dollars, with such steps as freezing Russian foreign reserves. Reducing holdings of Treasurys, a key component of Chinese foreign reserves, as part of an effort to diversify could help guard against the risk of similar sanctions being slapped on Beijing.

China's Treasury holdings peaked at over $1.3 trillion in fall 2013, with the country as the largest creditor to the U.S.

China is believed to be shifting some of its reserves into gold as an alternative to Treasurys. Chinese gold imports rose by around 60% to $76.6 billion in 2022, according to customs data -- the highest figure since tracking began in 2017.

The People's Bank of China has expanded its gold reserves for three straight months starting in November 2022. It had last reported an increase in the period from December 2018 to September 2019, during Beijing's trade war with the Trump administration.

While China may seek to cut its dependence on the dollar, it has made limited progress in globalizing the yuan -- a necessary step in that direction. The yuan was used in 1.91% of global transactions in January, down 1.29 points from a year earlier, data from the SWIFT, the global payments messaging system, shows.

Russia became a bigger yuan user in response to sanctions by the U.S., Europe and Japan, yet the impact of this shift has been limited. The country accounted for 4.27% of global yuan-denominated settlements in August 2022, rising to third in the world mostly on the back of its energy trade, according to SWIFT. But Russia's share fell to 2.57% in this past January as a commodities rally faded.

Few other assets have a similar market depth to U.S. government bonds. Some analysts say Chinese investors are merely moving Treasurys to tax havens like the Cayman Islands, which logged a $20.9 billion increase in holdings in 2022, to avoid scrutiny from American authorities.

Politico managed to achieve the most click-worthy title this weekend - ‘It’s the end of the world as we know it - and Munich feels nervous.’ I will return to the Munich Security Conference in a moment, but first, let’s look at a snapshot of recent economic trends:

US core PCE inflation on Friday is expected at 0.4% m-o-m and 4.3% y-o-y, more than double the rate of the Fed’s 2% CPI mandate.

Between Q4 2019 and Q1 2021, as services spending collapsed and pandemic assistance programs flowed, total US credit card debt fell from $930bn to $770bn. In Q3 2021, it started to rise, and in Q4 2022 leaped $61bn, the largest increase since 1999, to hit a record $986bn. Whether people are borrowing and spending because of the economy, or because they have no choice because of the economy, it is happening.

@GuyDealership says: “Used car prices are *skyrocketing* at a concerning pace. Prices have increased 4.1% so far this month: The LARGEST February increase since 2009. Buckle up.” However, delinquencies on car loans are also soaring.

Labor hoarding continues in construction due to the backlog of work that wasn’t done during Covid and as state spending picks up.

Recent liquidity expansion by the BOJ and PBOC, as well as the use of the US Treasury General Account balance, is arguably countering the effects of Fed QT. (And on QE, the late Shinzo Abe’s memoir notes: “Issuing JGBs for COVID stimulus checks does not mean that debt is being passed onto our grandchildren. The Bank of Japan purchases all government bonds. The Bank of Japan is like a subsidiary of the government so there is no problem.”)

The key question is this: does the Fed keep going until they break things; or do they stop and admit 3-4% CPI is good enough? Both of those outcomes imply the end of the world as we have long known it in markets. The first is an argument for bear flattening in bonds, a collapse in everything except bonds, and of everything against the dollar. The second implies bear steepening in bonds, a rally in everything else as an inflation hedge, and a collapse of the dollar against everything else.

So, back to Munich. This key security conference was covered by Bloomberg, but desperation to believe the world they represent is not ending saw its headline writers spin that the US and China were “talking". Yes - except the US accused Beijing of unacceptable behavior over spy balloons and claimed China is considering providing "lethal support" to aid the Russian invasion of Ukraine. China effectively called the US a warmonger while trying to woo Europe, and on Sunday warned the US it would "bear all the consequences" if it escalated the balloon further.

Moreover, US talk about Russia was equally confrontational. Vice-President Harris accused Moscow of crimes against humanity, climbing a ladder that will be very hard to come down from. UK Prime Minister Sunak is lobbying to send Ukraine the most advanced NATO weapons. China will release its peace plan on the first anniversary of the war on Friday: the West is skeptical.

This matters as the geopolitical are now geoeconomic. NATO chief Stoltenberg directly stated Europe’s dependency on Russian gas was dismissed as being economic, not security-related before February 2022 and that the EU should not make the same mistake with China, or others, by depending on their raw materials or exporting key technologies to them. Of course, such talk is cheap. Indeed, geopolitical thinker Michta noted in a somber analysis: “Was this what 1938 felt like before the German Nazi rape of Czechoslovakia? Satiated countries in the West issuing solemn assurances to Prague and others, but knowing deep in their bones that those checks would not be cashed? Because it was somebody else’s business, not ours?...

Rhetoric is not policy. I’ve sat through too many discussions where everything has been said but not by everyone, so we droned on… It’s not rocket science. It’s about spending the money to produce weapons and munitions so we can send them to Ukraine. It’s about agreeing what the end state should look like not for Ukraine, but for all of us. It’s about imagination, leadership, and courage.”

It is also about supply chains, on/friend-shoring, massive defense spending, capital controls – and then inflation and interest rates. One can no longer look at the latter in isolation.

Relatedly, Senator Hawley just gave a speech ‘China and Ukraine: A Time for Truth’ hammering home that the US cannot do what is it doing in Ukraine and step up in the Pacific, and arguing Europe must defend itself --and Ukraine-- now. Neither Europe nor markets grasp the tail risk of what this shift in US stance would entail, just as they ignored Trump in early 2016, and didn’t read Marx ahead of China’s Common Prosperity. Even for the US, Hawley claims: “Suppose China invades and seizes Taiwan. We try to stop it, but our forces are defeated and the island is lost. What would that mean?... Americans will confront a new, terrifying reality. Every American will feel it. The price hikes and disruptions we’ve seen in recent years will pale in comparison. Product shortages will be commonplace - shortages of everything from basic medicine to consumer electronics. According to some estimates, a war over Taiwan would send us into a deep recession with no clear way out, since huge swaths of our economy run on Taiwanese semiconductors. But the economic consequences are just the start.

If China takes Taiwan, it will be able to station its own military forces there. It can then use its position as a springboard for further conquest and intimidation - against Japan, the Philippines, and other Pacific islands, like Guam and the Northern Marianas… As Asia’s new reigning power, China could restrict US trade in the region - perhaps block it altogether. Maybe we’ll be allowed in, but only on terms favorable to China. China exploited the trading system once before. They can do it again… Imagine a world where Chinese warships patrol Hawaiian waters, and Chinese submarines stalk the California coastline. A world where the PLA has military bases in Central and South America. A world where Chinese forces operate freely in the Gulf of Mexico and the Atlantic Ocean.” Hawley’s proposed solution to prevent this “dark future” is “a nationalist foreign policy. A foreign policy in the spirit of Alexander Hamilton and Theodore Roosevelt. A nationalist foreign policy places America’s interests first. And deterring China from seizing Taiwan should be America’s top priority.”

Meanwhile, today’s headlines are also that inspectors say Iran’s uranium processing has almost reached nuclear weapons-grade purity (as they stand next to Russia and China); and North Korea just tested both short-range missiles and an ICBM that might soon be capable of holding a nuke. Both developments make urgent US, and European, action more likely. I don’t mean rate cuts.

One does not have to worry about the end of the world per se, but the world we knew is ending: in geopolitics; geoeconomics; monetary policy; and, with a lag, markets

Everywhere you look, there are major signs of froth.

1) Investors poured $1.5 billion into stocks per day in January.

2) Meme stocks and insolvent garbage tech plays are exploding higher by 20%, 30% even 100%+ in days.

3) Financial conditions are now LOOSER than they were before the Fed started raising rates in March of 2022.

4) The c-r-y-p-t-o pumpers are back… promoting their scams as the “answers” to everyone’s problems.

Put simply, it’s as if the Fed never even attempted to deflate the bubble of 2021-2022. If it weren’t for the fact Treasuries now yield 5%, you’d be hard pressed to find any signs that the Fed has accomplished anything of note.

Speaking of Treasury yields, the yield on the 2-Year U.S. Treasury has broken out of its downtrend. It is now probing its former highs. If it breaks here… GOOD NIGHT. https://gainspainscapital.com/wp-con...C22123real.png

The Fed is going to have to get a LOT more aggressive to reduce this level of froth and asset price inflation from the financial system. Put simply, the Fed will need to tighten things until something MAJOR breaks.

This opens the door to a SEVERE recession later this year. And that will mean stocks crashing to lows that no one anticipates.

If you’ve yet to take steps to prepare for what’s coming, we just published a new exclusive special report How to Invest During This Bear Market.

It details the #1 investment to own during the bear market as well as how to invest to potentially generate life changing wealth when it ends.

To pick up your FREE copy, swing by: https://phoenixcapitalmarketing.com/BM2.html

Throughout this week, I’ve pounded the table on the fact that the economic data the U.S. government has put out recently is a huge pile of BS.

We’ve covered everything from the jobs data, to inflation, and the recent retail sales results. By quick way of review, the highlights from my research are:

1) The reason the U.S. economy supposedly “added” 500,000+ jobs in January was due to an accounting gimmick, NOT because those jobs were actually created.

2) The Bureau of Labor Statistics (BLS) openly admits this, citing that without its “population control effect” the economy added… 84,000 jobs.

3) The only part of the inflation data that has dropped has been in Energy prices.

4) The reason Energy prices dropped was because the Biden administration dumped over 250 MILLION barrels of oil in the last two years.

5) Retail sales are booming because of INFLATION (things cost more), not because of consumer spending. The jump on credit card debt and massive decline in consumer savings confirms that Americans are maxing out their credit just to get by.

Perhaps the single most disturbing element of the above items is that they reveal the complete failure of the Federal Reserve to tame inflation. Indeed, according to the Taylor Rule which is widely considered one of the best indicators of where rates should be the Fed should have ALREADY raised rates to over 9% to stop inflation.

Instead the Fed has raised rates to 4.75% and is now talking about possibly one or two more rate hikes of just 0.25%. https://gainspainscapital.com/wp-con...K-1024x535.png

Everywhere you look, the Fed is failing miserably at curtailing inflation.

1) Financial conditions are now as loose it not looser then they were before the Fed began tightening monetary policy.

2) Meme stock mania is back with garbage companies rallying 30%, 50% even 100% or more in the last few weeks… again just like before the Fed began tightening monetary policy.

3) The inflationary data is being revised upwards: December’s -0.1% CPI report has been revised upwards to 0.1%, November and October’s CPI numbers were also revised higher.

4) The Producer Price Index results for January 2023 were reported yesterday. They showed inflation rising 0.7% month over month. On an annualized basis this puts inflation over 9%.

The Fed now has a choice: get serious about ending inflation and trigger a market meltdown… or face a debt crisis in the near future as bond yields roar to new highs, forcing the government to spend more and more money on debt payments.

Either way, the U.S. is heading for a crisis in the near future. And most investors are being lead like sheep to the slaughter!

On that note, we published a Special Investment Report concerning FIVE secret investments you can use to make inflation pay you as it rips through the financial system in the months ahead.

HIVE Announces Quarterly Revenue of $14.3 Million, Gross Mining Margin of $3.6 Million and Achieves Adjusted EBITDA of $1.5 Million for the Quarter while HPC Revenue Strategy is Gaining Momentum With Annual Run Rate of $1.3 Million

Vancouver, Canada – HIVE Blockchain Technologies Ltd. (TSX.V:HIVE) (Nasdaq:HIVE) (FSE:HBFA) (the “Company” or “HIVE”) a leading digital asset miners and green focused data center builder and operator, is pleased to announce the earnings report for the third quarter ended December 31, 2022 (all amounts in US dollars, unless otherwise indicated).

HIVE achieved revenue of $14.3 million this quarter, by mining 787 Bitcoin, with a 25% Gross Mining Margin representing $3.62 million of income from mining operations. This is notable, as the first full fiscal quarter for HIVE that does not include any Ethereum mining revenues, as the Ethereum Merge took place on September 15th, 2022. Furthermore, average Bitcoin prices in this current quarter decreased from the prior quarter by approximately 15%, continuing this crypto winter that affects the entire Bitcoin mining sector. However, through hedging our energy contracts, selling power back to the grid, and optimizing our operating capacity to focus on maximum profit per KWHR, HIVE has realized profit from mining operations this quarter.

The Company notes that HIVE’s production of 787 Bitcoin this quarter represents an increase of 13% year over year, with the same period last year, having mined 697 Bitcoin reflecting a continued growth in our operating hashrate. This is in large part a result of the completion of our New Brunswick data center campus, which we have seen reach over 1 Exahash of Bitcoin mining capacity this year, operating in a four-building data center campus, which HIVE owns, and includes our own substation, transformers and electrical infrastructure. This large increase in quantity of Bitcoin production stands even as network difficulty has increased by 60% in this one-year period, while Bitcoin prices and prices have fallen approximately 50%.

Frank Holmes, HIVE’s Executive Chairman, stated “We wish to again thank our loyal shareholders for believing in our vision to mine both Ethereum and Bitcoin. We are sad to see the higher margin from mining Ethereum gone however our HPC strategy which has taken longer to roll out is now growing rapidly on a month over month basis. We are happy to share that our robust growth is scalable and could potentially increase 10x fold over the next year as the demand for our high quality chips due to the huge global demand for Ai projects like GPT CHAT, medical research, machine learning and rendering. Further, HIVE was the first to use our software to help balance the electrical grid and resell back energy whenever there is spike in demand. This strategy has been good for the community and HIVE. Even with a challenging quarter for the global digital asset ecosystem, where we saw the capitulation of crypto prices due to the implosion of FTX and the related contagion with other exchanges, lenders and hedge funds. Strategically, we have not borrowed expensive debt against our mining equipment or pledged our Bitcoins for costly loans, thus our balance sheet remains healthy to weather this storm. We believe our low coupon fixed debt; attractive green renewable energy prices and high performing energy efficient ASIC and GPU chips will help us navigate through this crypto winter. The most recent unexpected challenge has been in Sweden which we cover in greater detail in our interim filings.”

Aydin Kilic, President & CEO of HIVE, added, “HIVE has skillfully navigated the digital asset mining industry in a post-Ethereum merge, when many questioned how we could continue to generate profit from operations. This has been answered by our gross mining margins of $3.6 million this quarter, during a time when many other crypto miners are struggling for solvency. In fact, our Bitcoin holdings have increased by 30% year over year for the period ending December 31, 2022 with 2,372 Bitcoin. In addition to this, we saw Bitcoin mining difficulties increase 60% during this period, reaching an all-time high of almost 40T. HIVE navigated this quarter by selling energy back to the grid, repurposing our GPUs to mine Bitcoin, and upgraded our fleet of ASICs to improve our overall efficiency. As previously reported, our GPUs are currently doing $80 per megawatt hour in revenue, which is similar to Bitcoin mining economics with ASICs. I am incredibly proud of the team, as we have among the leanest G&A as a percentage of revenue among our peers in the industry. HIVE is dedicated to delivering its shareholders value and strives to excel in optimization and efficiency; this quarter the numbers illustrate the merit of our approach and our success. We strive to set the gold standard of operational efficiency at HIVE while constantly adapting to changing market conditions with an agility mindset.”

HIVE achieved a gross mining margin of $3.6 million for the quarter, a 77% decrease over the prior quarter of $15.9 million due to the loss of Ethereum revenues from the Merge and lower Bitcoin prices. This decline in gross mining margin was predominantly driven by significant lower average cryptocurrency prices during this period which negatively affected us as well as the entire Bitcoin mining industry.

On a relative basis HIVE has been able to mine with healthy profit margins during periods of market volatility because of being globally diversified and enjoying attractive power costs in Sweden, Iceland, and Quebec.

Furthermore, HIVE’s average cost of production per Bitcoin was $13,599 (including cost of goods sold, not including SG&A) for the quarter ending December 31, 2022, a 37% increase in cost from the previous quarter ending September 30, 2022. The company notes that from October 2022 onwards, with Bitcoin mining hash rates and Difficulty at all-time highs, it is expected that the cost of production for Bitcoin will increase for the industry at large, as less Bitcoin per Terahash is being rewarded at these difficulty levels.

According to Anthony Power’s monthly industry research we are proud to have achieved and maintained among the best operational uptime amongst all its peers, with HIVE repeatedly emerging as one of the most efficient crypto miners based on digital assets mined per Exahash (commonly measured as quantity of mined Bitcoin per Exahash of reported hashrate).

Further to the Company’s news release dated February 15, 2023, as a result of the filing on the date hereof of the Company’s interim financial statements and accompanying management’s discussion and analysis for the three and nine months ended December 31, 2022 (the “Interim Filings”), a management cease trade order has not been necessary. Consequently, there will be no restriction of the Company’s chief executive officer and chief financial officer from trading the Company’s shares resulting from such management cease trade order. Details of the tax notice received in relation to one of the Company’s European subsidiaries is disclosed in the Interim Filings.

Mark-to-Market of Assets and Non-Cash Writedowns

There was continued pressure in the accounting world to take non-cash charges against mining equipment that is required to create digital assets. With the Ethereum move to proof-of-stake taking place in September 2022, the value of the GPU chips used in proof-of-work mining has fallen globally. Additionally, the price of primary ASIC chips moves in tandem with the price of Bitcoin. On big quarterly down swings like the last couple of quarters we reduce the value of the Bitcoin held in our treasury and the resale cost of the mining equipment, however when Bitcoin prices rise, they are written back up through inventory holdings and flow through the income statement using mark-to-market accounting, while equipment often is not written back up as the threshold to do so is higher. This is a conservative accounting treatment which public crypto mining companies usually follow.

Our adjusted EBITDA for the quarter was $1.5 million with the decline in digital asset prices during the quarter, in addition to a significant impairment of $61.5 million on mining equipment and deposits. Digital assets continue to be much more volatile than the stock market, thus our digital assets can significantly move income both up and down each quarter.

Q3 Quarterly Summary- December 31, 2022

Generated revenue of $14.3 million, with a gross mining margin[1] of $3.6 million

Mined 787 Bitcoin during the three-month period ended December 31, 2022

Adjusted EBITDA1of $1.5 million for the three-month period

Working capital decreased by $21.6 million during the three-month period ended December 31, 2022

Digital currency assets of $39.0 million, as at December 31, 2022

Average cost of production per Bitcoin was $13,599, where the average Bitcoin price was $18,072, during the three-month period ended December 31, 2022. This also represents a 37% increase in production costs of Bitcoin from the previous quarter of $9,894 for the three months ended September 30, 2022 (average price of Bitcoin was $21,252 during this period).

Impairment on miner equipment of $38.8 million and of $22.7 million on equipment deposits during the three-month period ended December 31, 2022

Net loss before tax of $90.4 million for the three-month period attributable to impairment from the value of ASIC and GPU chips declining with the drop in Bitcoin and Ethereum prices and the mark-to-market Bitcoin HODL position

Q3 F2023 Financial Review

For the three months ended December 31, 2022, revenue from digital currency mining was $14.1 million, a decrease of approximately 51.6% from the prior year primarily due to the Merge, significant global hashrate growth combined with much lower average cryptocurrency prices.

Gross mining margin1 during the period was $3.6 million, or 25% of income from digital currency mining, compared to $15.9 million, or 54% of income from digital currency mining, in the same period in the prior year. The Company’s gross mining margin1 from digital currency mining is partially dependent on external network factors including mining difficulty, the amount of digital currency rewards and fees it receives for mining, as well as the market price of digital currencies. The decrease in gross mining margin1 is greatly affected by the price of digital currencies which is approximately 67% of what it was in the prior year quarter.

The Company notes that, while adjusted EBITDA1 this quarter was $1.5 million, because of mark to market accounting practice, net loss during the quarter ended December 31, 2022, was $90.0 million, or a loss of $1.09 per share, compared to net income of $51.2 million, or $0.66 per share, the same period last year. The decline from the prior year was driven primarily by the Merge, higher non-cash charges such as depreciation, unrealized valuation losses on digital currencies and investments, and impairment charges on equipment and equipment deposits, which in turn were all affected by lower Bitcoin and Ethereum prices seen in the current quarter. Adjusted EBITDA is a non-IFRS financial measurement and should be read in conjunction with and should not be viewed as an alternative to or replacement of measures of operating results and liquidity presented in accordance with IFRS.

Mr. Holmes noted, “At HIVE we strive to maintain a high-performance culture, which means that we always adapt to unexpected headwinds, and do our best to maintain operational excellence in the process.”

The Company uses EBITDA and Adjusted EBITDA as a metric that is useful for assessing its operating performance on a cash basis before the impact of non-cash items and acquisition related activities.

EBITDA is net income or loss from operations, as reported in profit and loss, before finance income and expense, tax and depreciation and amortization.

Adjusted EBITDA is EBITDA adjusted for removing other non-cash items, including share-based compensation, non-cash effect of the revaluation of digital currencies and one-time transactions.

The Company emphasizes that “adjusted EBITDA” is not a GAAP or IFRS measurement and is included only for comparative purposes.

Non-Cash Charges

A non-cash charge is a write-down or accounting expense that does not involve a cash payment. Depreciation, amortization, depletion, stock-based compensation, and asset impairments are common non-cash charges that reduce earnings but not cash flows.

Financial Statements and MD&A

The Company’s Consolidated Financial Statements and Management’s Discussion and Analysis (MD&A) thereon for the three and nine months ended December 31, 2022 will be accessible on SEDAR at www.sedar.com under HIVE’s profile and on the Company’s website at www.HIVEblockchain.com.

HIVE Performance Cloud

HIVE is also pleased to announce its anticipated plans to launch HIVE Performance Cloud in calendar Q2 2023.

Prior to the full-scale launch of HIVE Cloud, we are also pleased to share that our proof-of-concept to utilize our fleet of GPUs is currently produced annual revenue on a run-rate basis over $1 million, doing high performance computing workloads (not involving digital asset mining).

5 Minute Chart of Dow 30 - As usual the same pattern repeats leading to millions and millions of dollars of Forex trading profits using our UNIQUE method of Money Flow Forex Trading.

Of course, the millions and millions of dollars of profits are what our corporation Aviel Forex Learning Edge will be earning this calendar year 2023...

Biden made a surprise visit to Ukraine one day ahead of Putin’s National Address scheduled for February 21st. Biden had the audacity to put out the West’s constant propaganda:

“One year later, Kyiv stands. And Ukraine stands. Democracy stands,” he declared. “The Americans stand with you and the world stands with you.”

Putin is elected the head of Russia by its Parliament the same system that takes place in Britain, the EU, Canada, and every country with a Parliamentary system. Only the United States is where the head of state stands for election by the people. This nonsense that Ukraine stands for democracy again Russia is just total outright lies. This only demonstrates that we cannot trust a single word from governments in such times. As they say, truth is the first casualty in war. https://www.armstrongeconomics.com/w...e-for-wart.png

Had the West simply been honest and honored what they negotiated that the Donbas under the Minsk Agreement was to be allowed to vote on their own separatist movement. All the deaths in Ukraine and their blood are in the hands of the West. This war would have NEVER taken place if the Minsk Agreement was honored. https://www.armstrongeconomics.com/w...en-Anthony.png

Blinken has made it clear that the US will NEVER accept the Minsk Agreement and it was indeed only to buy time for a war they wanted from the start. The Biden Administration changed the arrangement with Ukraine in 2021 altering all previous agreements since 2008. This is a Neocon’s dream come true – a direct confrontation with Russia. He outright said that there shall be no peace by returning any land to allow the Russians of the Donbas to live in peace free of Ukrainian domination.

“If we do that, we will open Pandora’s box around the world, and every would-be aggressor will conclude that, ‘If Russia got away with it, we can get away with it,'” Blinken said. “And that’s not in anyone’s interest, because it’s a recipe for a world of conflict.”

This illustrates the duplicity of the West and the desire for World War III. These are the people who are cheering the destruction of our future all for a strip of land that has been occupied by Russians for centuries.

In all my years of dealing with governments, NEVER have I ever even once witnessed such stupidity and arrogance on the part of any government. This Biden Administration seems to be going out of its way to piss off just about everyone in the world to create World War III.

This is just unimaginable. They seem to want to “shrink” the world’s population by 50% with war to get their pat on the back from Gates, Rockefeller Foundation, and Schwab. When you say it is your way or no way, that is not how you negotiate anything.

History will remember the Biden Administration with contempt as the Hitler of the 21st Century.

Hello Benny,

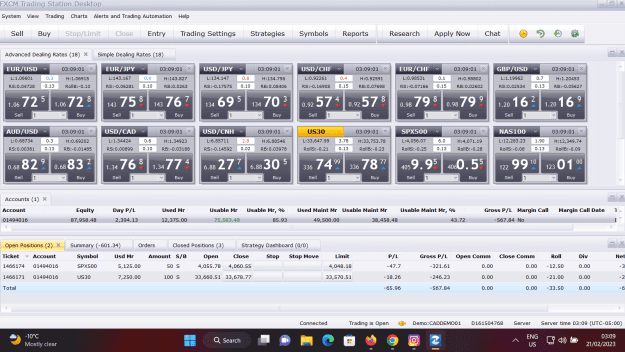

Here is a copy of all my accounts, the first one was open Jan 23,2023 when I first started your course. Then as you see I made some bad trades Feb 1,2023 and final got out today for total 62 152.

In the mean while I was not able to trade so I open an account for my wife and daughter and son

So on Feb 7, 2023 I started trading my wife's account and up to date the total is 59058 with no losses... I think I fear her so I made sure to make it look good for her.

The third account is my daughters, on this one I learned not to trade silver and gold when the markets are down and have been stuck in my trades since Feb 2,2023 but managed to trade with little margin left with a total 48750. I hope to close those trades soon.

Last is my son's account which I struggled to make a little profit since I made bad trades, and today I was final out with a total 52928.

I've been taking my trading seriously even though its a demo account and having lots of fun along the way.

Why take a trip if your not going to enjoy the journey. Thank you for everything you've taken the time to teach me.

Authored by Ven Ram, Bloomberg cross-asset strategist,

Investors now expect the major central banks to raise rates much more than they were just at the start of this month. They are still underpricing the risk of how much more tightening is to come.

The Federal Reserve may raise interest rates as high as 6%, the European Central Bank to 4% and the Bank of England to possibly 5% should the global economy continue to be resilient and inflation run rife. https://assets.zerohedge.com/s3fs-pu...?itok=xYSXvJG0

Here’s why...

The tell-tale three-month/10-year Treasury curve has been in a consistent inversion since November, and typically, recessions have followed between 11 and 14 months. https://assets.zerohedge.com/s3fs-pu...?itok=zs-IjNs3

That would suggest that the US economy is unlikely to roll over before October at the earliest - meaning central banks may be raising rates all through the summer as they try to get inflation to converge to their targets.

While traders have re-priced central bank trajectories considerably this month, they are still blasé: the markets currently see a terminal rate just shy of 5.50% in the US, about 3.75% in the eurozone, and 4.50% in the UK.

The scenarios projected above are consistent with the analysis that showed the Fed has, on average, been able to stop tightening only when its inflation-adjusted policy rate has reached a full 200 basis points.

The Fed’s current real policy rate is 95 basis points — meaning it still has a considerable distance to go.

Recent data in the US have upended expectations of quick disinflation, with consumer prices actually accelerating from a month earlier in January — spurred by the jobless rate sliding to the lowest since 1969 and retail sales rising the most in almost two years.

While the Fed has raised rates by a phenomenal 450 basis points in the current cycle, headline inflation is still running at 6.4%, more than three times its target.

Recent comments by euro-region policymakers suggest that the ECB may act forcefully.

The central bank currently projects inflation to average 6.3% this year, meaning its real policy rate is deeply negative, underscoring why many of its officials reckon the benchmark isn’t restrictive yet.

In the UK, recent comments suggest that policymakers are wary of taking interest rates too high, though BOE Governor Andrew Bailey’s remarks suggest that the central bank may make peace with a peak rate of 4.50%

.

Even so, with both headline and retail-price inflation in the UK still running above 10%, a quick decline to 2% is unlikely. Also, in an environment where the Fed and the ECB keep raising rates, the BOE would find it hard to stop where it would like to in the absence of compelling evidence that inflation is crumbling.

At the start of the year, traders were working on the assumption that inflation is a problem of yesteryear. Now we know that it is still alive and kicking, while the economies are also more resilient than thought. That means only one thing: a re-calibration of central banks’ rate trajectories.