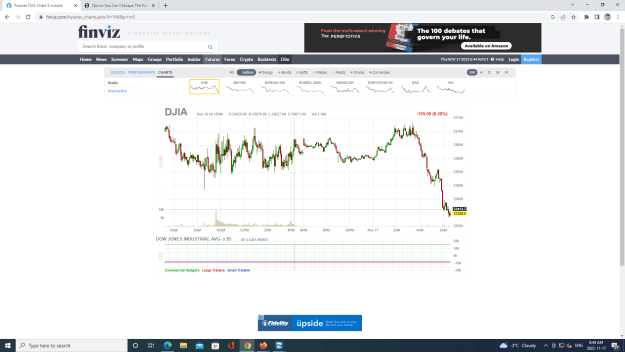

Attached Image (click to enlarge)

Whats your best money management method? 52 replies

How to flow with the order flow? 26 replies

Money Management / Risk Management 24 replies

Money management model for multiple strategy trading method 16 replies

Most popular money management method. 7 replies

In an interview with Reuters in September, OTPP had described its investment in FTX as the one having "lowest" risk profile in this space.

Teacher's Venture Growth invests in early stage start-ups.

"Naturally, not all of the investments in this early-stage asset class perform to expectations," the fund said.

The Ontario government, which is a joint sponsor of the pension fund, said that the Financial Services Regulatory Authority of Ontario, as the regulator of OTPP, engages with plans to ensure appropriate risk management processes are in place. FSRAO did not provide an immediate comment.

Most other Canadian pensions fund, who are prolific global investors, have stayed away from crypto investments. Canada's fifth-largest fund PSP said it wanted to be cautious despite being interested in the crypto space,

"You have to be careful as a pension fund and as a long term investor when you step into innovation and a new technology," said Herman Bril, head of Responsible Investment at Montreal-based Public Sector Pension Investment Board.

Reporting by Divya Rajagopal and Maiya Keidan in Toronto, editing by Deepa Babington

https://www.natlawreview.com/article...saga-continues

The FTX Bankruptcy and the Question of Prudent Retirement Plan Investments: the Saga Continues

Monday, November 14, 2022

Among those impacted by the U.S. bankruptcy filing of leading global cryptocurrency exchange FTX on November 11, 2022 is the Ontario Teachers’ Pension Plan. Last October, the Ontario Teachers' Pension Plan Board, via its Teachers' Innovation Platform, invested $75 million in FTX Trading Ltd.’s (the owner and operator of FTX.com) Series B-1 fundraise.

Early this year, the pension plan invested another $20 million in FTX. FTX was an attractive investment because the focus of the Teachers’ Innovation Platform is growth equity and venture capital investments in companies, such as FTX, that are using technology to shape future markets. Hopefully the pension’s financial losses in this investment will have limited impact since the pension’s board has reported that the fund’s FTX exposure is limited to 0.05% of its total assets as it manages more than $182 billion in net assets for Ontario school teachers. But, news of FTX’s bankruptcy filing has negatively impacted cryptocurrencies, crypto related stocks and blockchain-related firms across the board, and will continue to have a ripple effect.

For U.S. retirement plans, this year has seen much debate regarding the Department of Labor’s Compliance Assistance Release No. 2022-01 on 401(k) Plan Investments in “Cryptocurrencies” issued on March 10, 2022. The DOL has more recently explained that the Release does not make new law, but rather it was issued as an interpretive rule on the duty of prudence with respect to cryptocurrency investment options and reminds fiduciaries of their duties as expressed under ERISA and the Supreme Court’s decision in Hughes v. Northwestern University, which found that fiduciaries must ensure that each plan investment option offered is prudent.

Yet, investments in cryptocurrency are not limited to 401k plans. In fact, in the 2022 CFA Institute Investor Trust Study found that 94% of state/government pension plan sponsors and 62% of corporate defined benefit plan sponsors invest in crypto assets, as institutional investors find that a small allocation to digital assets can be beneficial to a diversified portfolio. And for fiduciaries of retirement plans governed by ERISA, if the Retirement Savings Modernization Act introduced by Senator Pat Toomey, Senator Tim Scott and U.S. Representative Peter Meijer on September 29, 2022 is passed, ERISA would be amended to clarify that ERISA plan fiduciaries do not breach their fiduciary duties solely by selecting or monitoring investment options that include a range of asset classes, including digital assets and infrastructures. Prudent decision-making, therefore remains key.

While the latest fallout from the FTX bankruptcy will surely provide more reasons to scrutinize plan participant access to cryptocurrency and related investments, the story of the future of retirement plan investing is still being written. As the old adage goes, nothing ventured, nothing gained.

"You have to be careful as a pension fund and as a long term investor when you step into innovation and a new technology," said Herman Bril, head of Responsible Investment at Montreal-based Public Sector Pension Investment Board.

https://www.reuters.com/technology/ontario-pension-says-any-loss-ftx-inv...

![]() 1994-2022 Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C. All Rights Reserved.

1994-2022 Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C. All Rights Reserved.

Two large Canadian pension plans have found themselves enticed and then burned by crypto investments this year.

The Ontario Teachers’ Pension Plan Board revealed last week that it had made a US$95-million investment in FTX, while the Caisse de dépôt et placement du Québec said in August it had written off its US$150-million investment in Celsius Network LLC, which had entered court-supervised bankruptcy proceedings in the United States.

Caisse chief executive Charles Emond said at the time that his team had conducted extensive due diligence with outside experts and consultants. They were aware of management and regulatory issues at Celsius and underestimated the time it would take to resolve them, he said, adding the Caisse was keen on “seizing the potential of blockchain technology” and that perhaps the investment in Celsius had been made “too soon” in the company’s development.

• Email: [email protected] | Twitter: BatPost

NOUVELLES & VUES

Prévisions, commentaires et analyses sur l'économie et les métaux précieux

Célébrons notre 49e année dans le secteur de l'or

DÉCEMBRE 2022

"... [D]ollars, yens et euros ne brilleront pas toujours dans une tempête, et ils ne seront jamais confondus avec de l'or."

Sir Peter Tapsel

–––––––––––––––––––––––––––––––––––––––––––––––––– –––––––––––––––––––––––––––––––––––––––––

La Chine est-elle la baleine mystérieuse du marché de l'or ?

"La relique barbare lance maintenant une alerte rouge pour les haussiers du dollar"

https://www.usagold.com/wp-content/u...e-1024x594.png

Ventes et achats d'or de la Banque centrale

2002-2022 (T3) (net ; tonnes métriques)

https://www.usagold.com/wp-content/u...2-1024x490.png

Graphique par USAGOLD [Tous droits réservés] • • • Source des données : World Gold Council

–––––––––––––––––––––––––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––––––––––––––––––––

–––––––––––––––––––––––––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––––––––––––––––––––

Court et doux

"POUR LA PLUPART DES ANALYSTES, LES PROBLÈMES DE LIQUIDITÉ sur le marché du Trésor ne sont pas seulement liés à l'évolution rapide des prix, ils sont également le reflet d'une pénurie d'acheteurs ou d'une incapacité ou d'une réticence des acheteurs sur le marché à éponger toute l'offre", rapporte Financial Times.Cette absence d'acheteurs est le résultat, pour l'essentiel, du retrait de la Fed et de la Banque du Japon du marché des bons du Trésor en tant qu'acheteurs. En bref, ces fissures pourraient rapidement devenir des fractures majeures à moins que des acheteurs ne soient trouvés ailleurs. Comme le souligne FT, en cas de nouvelle crise, la Fed arrêterait probablement le resserrement quantitatif ou même reviendrait à l'assouplissement quantitatif, comme l'a fait la Banque d'Angleterre dans des circonstances similaires il y a quelques mois. Un tel retrait de la politique déclarée, cependant, ne communiquerait pas "le type de stabilité et de sécurité dont dépendent les investisseurs du monde entier", déclare FT.https://www.usagold.com/wp-content/uploads/ramirezFTXscandal2-1024x697.jpeg Dessin animé avec l'aimable autorisation de MichaelPRamirez.com

Citation notable

"L'investissement physique en 2022 est en passe de bondir de 18% à 329 millions d'onces, ce qui serait également un nouveau record. Le soutien est venu des craintes des investisseurs face à une inflation élevée, de la guerre russo-ukrainienne, des craintes de récession, de la méfiance à l'égard du gouvernement et des achats en cas de baisse des prix. La hausse a été encore stimulée par un (quasi-doublement) de la demande indienne, une reprise après le marasme de l'année dernière, les investisseurs profitant souvent de la baisse des prix de la roupie. – The Silver Institute, Revue intermédiaire du marché de l'argentExcédent ou déficit d'argent

(Millions d'onces troy)

https://www.usagold.com/wp-content/u...V-1024x718.png

Graphique par USAGOLD [Tous droits réservés] • • • Source des données : The Silver Institute

«Après 14 ans, [crypto] est toujours une solution à la recherche d'un problème. Il ne s'agit pas de construire un nouveau système financier. Il ne s'agit pas de construire un nouvel Internet. Ce n'est pas un actif décorrélé du marché. Ce n'est pas une couverture contre l'inflation. C'est un véhicule de spéculation pure et nue, détachée de tout ce qui touche à l'économie. C'est un casino enveloppé dans tous ces mensonges. Lorsque vous déchirez ces mensonges, ce qui reste ressemble à un net négatif pour le monde. – Philip Diehl, Financial TimesPensée finale

La politique de la Fed est-elle vraiment aussi hawkish qu'elle voudrait le faire croire aux marchés ?

Certains applaudissent le président actuel de la Fed comme s'inspirant de l'inflation qui a vaincu Paul Volcker. D'autres voient en lui une politique plus proche de celle d'Arthur Burns dans les années 1970. L'un des observateurs les plus célèbres de la Fed à Wall Street, Henry Kaufman, a déclaré : « J'attends toujours qu'il agisse avec audace. Aujourd'hui, le taux d'inflation est supérieur aux taux d'intérêt. À l'époque, les taux d'intérêt étaient supérieurs aux taux d'inflation. C'est toute une juxtaposition. Nous avons un long chemin à parcourir. L'inflation doit baisser ou les taux d'intérêt augmenteront.Taux d'inflation et taux d'intérêt en Argentine

(%, 2008-2022)

https://www.usagold.com/wp-content/u...V-1024x615.png![]()

Graphique avec l'aimable autorisation de TradingView.com • • • Taux d'inflation rouge, taux d'intérêt noir • • • Cliquez pour agrandir

__________________________________________________________________________________

https://www.usagold.com/wp-content/u...insV4trans.pngInquiet de la suite de la Grande Crise Financière ?

DÉCOUVREZ LA DIFFÉRENCE USAGOLD

BUREAU DE COMMANDE :

1-800-869-5115 x100 • • •[email protected]• • •COMMANDEZ DE L'OR ET DE L'ARGENT EN LIGNE 24-7

https://www.usagold.com/wp-content/u...ogo2021NV3.png

–––––––––––––––––––––––––––––––––––––––––––––––––– –––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––––––––––––––

https://www.usagold.com/wp-content/u...marginNV-2.png Michael J. Kosares est le fondateur d'USAGOLD, auteur de The ABCs of Gold Investing - How To Protect and Build Your Wealth With Gold [Three Editions], et l'éditeur des publications du cabinet.NEWS &VIEWS

Forecasts, Commentary & Analysis on the Economy and Precious Metals

Celebrating our 49th year in the gold business

DECEMBER 2022

“… [D]ollars, yen, and euros will not always glitter in a storm, and they will never be mistaken for gold.”

Sir Peter Tapsell

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Is China the mystery whale in the gold market?

‘The barbarous relic now flashing a red alert for dollar bulls’

https://www.usagold.com/wp-content/u...e-1024x594.png

Central Bank Gold Sales and Purchases

2002-2022 (Q3) (net; metric tonnes)

https://www.usagold.com/wp-content/u...2-1024x490.png

Chart by USAGOLD [All rights reserved] • • • Data Source: World Gold Council

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

The six keys to successful gold ownership––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Short & Sweet

“FOR MOST ANALYSTS, THE LIQUIDITY PROBLEMS in the Treasury market are not just about rapidly changing prices, they are also a reflection of a dearth of buyers or an inability or unwillingness of the buyers in the market to mop up all the supply,” reports Financial Times. That absence of buyers is the result, for the most part, of both the Fed and the Bank of Japan withdrawing from the Treasuries market as buyers. Those cracks, in short, could quickly become major fractures unless buyers are found elsewhere. As FT points out, in the event of another crisis, the Fed would likely halt quantitative tightening or even return to quantitative easing, as did the Bank of England under similar circumstances a few months ago. Such a retreat from stated policy, though, would not communicate “the kind of stability and security that investors around the world depend on,” says FT.https://www.usagold.com/wp-content/u...-1024x697.jpegCartoon courtesy of MichaelPRamirez.com

Notable Quotable

“Physical investment in 2022 is on track to jump by 18% to 329 million ounces, which would also be a new record. Support has come from investor fears of high inflation, the Russia-Ukraine war, recessionary concerns, mistrust in government, and buying on price dips. The rise was boosted further by a (near-doubling) of Indian demand, a recovery from a slump last year, with investors often taking advantage of lower rupee prices.” – The Silver Institute, Interim Silver Market ReviewSilver surplus or deficit

(Millions of troy ounces)

https://www.usagold.com/wp-content/u...V-1024x718.png

Chart by USAGOLD [All rights reserved] • • • Data source: The Silver Institute

“After 14 years, [crypto] is still a solution in search of a problem. It’s not building a new financial system. It’s not building a new internet. It’s not an asset uncorrelated with the market. It’s not a hedge against inflation. It is a vehicle for pure, naked speculation detached from anything in the economy. It’s a casino that’s wrapped in all of these lies. When you tear back those lies, what’s left looks like a net negative for the world.” – Phillip Diehl, Financial TimesFinal Thought

Is Fed policy really as hawkish as it would like markets to believe?

Some applaud the current Fed chairman as drawing inspiration from the inflation vanquishing Paul Volcker. Others see him as charting a policy closer to that of Arthur Burns during the 1970s. One of Wall Street’s most famous Fed watchers, Henry Kaufman, says, “I am still waiting for him to act boldly. Today, the inflation rate is higher than interest rates. Back then, interest rates were higher than inflation rates. It’s quite a juxtaposition. We have a long way to go. Inflation has to come down or interest rates will go higher.”Argentina inflation rate and interest rate

(%, 2008-2022)

https://www.usagold.com/wp-content/u...V-1024x615.png

Chart courtesy of TradingView.com • • • Inflation rate red, interest rate black • • • Click to enlarge

__________________________________________________________________________________

https://www.usagold.com/wp-content/u...insV4trans.pngWorried about the sequel to the Great Financial Crisis?

DISCOVER THE USAGOLD DIFFERENCE

ORDER DESK:

1-800-869-5115 x100 • • • [email protected] • • • ORDER GOLD & SILVER ONLINE 24-7

https://www.usagold.com/wp-content/u...ogo2021NV3.png

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––––––––––––––

https://www.usagold.com/wp-content/u...marginNV-2.pngDislikedHi BenjaminIS, Kindly could you please explain your Money Flow Trading Method with Risk Management in detail? Every day where do you go first to see and decide whether RISK OFF OR not ?? and at what time ?? ThanksIgnored