{quote} I have some questions : Trading time. - Broker/Local time? News On/Off some of them. - We can play also with news timing to check from 120 - 480 min. Entry Signal D1/M15 and H4/M15. - D1 has given more stable signals. Close on profit with fixed lot 0.02 and different Take Profit in equity like 4/5/6 . - with cvp 0.02 , is it good to use TP 6,7,8 ? Negative Correlation Limit to scan between -90 / -95 . - my feedback is stronger is better. Thank you.

Ignored

1.Broker time.

2.Good idea.

3.I agree.

4.Yes.

5.Yes,but you might have less orders opened.

I think to understand almost all thing about corti EA after using it for a few weeks.

The one thing I'm not very sure is about CVP : will it keep the same the value of 1 pip for each pair by adjusting the lot to use ? For example >>> for triangular GBPJPY / GBPUSD - USDJPY the value of 1 pip for each pair will be the same, let's say $ 1. I'm right ?

My belief is that instead of CVP a better approach is to calculate margin needed on-the-fly and therefore risk the exact amount of money on both trading instruments, below is the MQL5 sample code for this purpose (I know, I know, but it can be converted to MQL4 easily):

This way you can risk exactly 100$ for EURAUD and 100$ for AUDJPY for example (those were the latest trades of Corti's EA).

One more thing, so far I cannot understand why the EA gets the correlation coefficients from outside source, instead of using simple Pearson/Spearman/Kendall correlation matrix calculations, or even simpler StdDev over mean, example code:

My belief is that instead of CVP a better approach is to calculate margin needed on-the-fly and therefore risk the exact amount of money on both trading instruments, below is the MQL5 sample code for this purpose (I know, I know, but it can be converted to MQL4 easily): double calcMarginNeeded(string oSymbol, double oLots) { /* SYMBOL_CALC_MODE_FOREX Margin: Lots * Contract_Size / Leverage * Margin_Rate SYMBOL_CALC_MODE_FOREX_NO_LEVERAGE Margin: Lots * Contract_Size * Margin_Rate SYMBOL_CALC_MODE_FUTURES Margin: Lots * InitialMargin * Margin_Rate...

Ignored

Hi man

Welcome to/at FF community and thanks for your inputs

regards

I have prepared MT5 indicator, which displays correlation or cointegration statistics between given instruments.

Correlation is not the same as cointegration - the correlation is used to check for the linear relationship (or linear interdependence) between two variables, while cointegration is used to check for the existence of a long-run relationship between two or more variables (i.e. is the difference in movements between instruments stationary). Thus, cointegration does not reflect whether the pairs would move in the same or opposite direction, but can tell you whether the distance between them remains the same over time.

I find it useful to check if particular instruments are correlated and at the same time cointegrated, this way it is statistically more likely given trade deal (consisting of two symbols) to become a winning trade. I assume that parameters of the indicator are self-explanatory and almost anyone can understand how to use it.

A hint: when indicator line is green in correlation mode (either Pearson, Spearman or Kendall), that means that both instruments are also cointegrated. Also if initially indicator does not show any information - give it some time or right-click "Refresh" from MetaTrader platform, most probably chart history of one (or both) instruments is not loaded fully.

Download Corti v3.33 - https://macrofed.com/ .

Fixed a bug in case of VPS restart that did not load some of the trades when there were multi instances trading. This Bug was found while testing SpiderWeb with 10 instances.

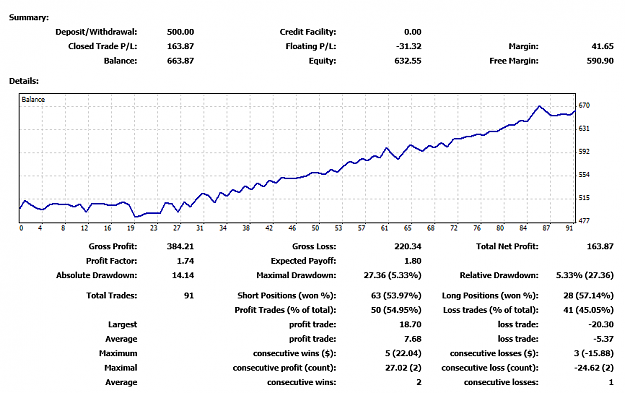

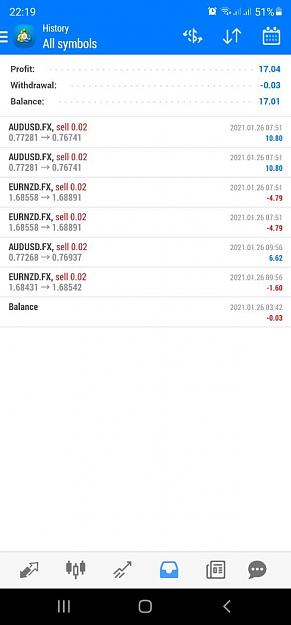

{quote} Brilliant thank you. Just out of interest does it only trade EUR/AUD and AUD/CHF? Thats all it has traded so far, all of which have been profitable.

Ignored

It trades the most negative correlated duo,from time correlation change and you will see other pairs too.