| Risk Management |

This thread will serve as an all encompassing guide to learning how to approach risk management from scratch. Hopefully by sharing this knowledge with you I can dispel some common myths, clarify hotly debated topics, and bring profitability to your trading by breaking the numbers down in an easy to digest format. There will be quite a lot of information contained within this thread so read carefully, remember that it's your money on the line!

Also if there's anything I should add or clarify more on then be sure to let me know!

- When making a comment about risk management, make sure to understand that there a many different ways to approach risk management but only a few are proper for a beginner and the type of strategy being used (as explained below)

- This thread will only accept proper risk management strategies geared towards beginner traders. Strategies that aren't complex and convoluted and easy for a beginner trader to use as a foundation for how they should approach risk.

- If you're a beginner trader and you start to become confused after reading many different comments and suggestions made by other users on ForexFactory, remember to just come back to this original thread and cross-analysis, use this as a your book of Golden Rules.

At some point I'll also release one of my custom Lot Sizing programs to help you instantly calculate the proper lot size for each trade you make (there are some already online but none really did what I wanted). I'm eventually going to make the program into an EA so one could quickly hit Buy or Sell and the position will be perfectly sized according to defined risk management protocols, that way all of this information can be wrapped up in a single button click.

Steady trading!

----------------------------------------------------------------------------------------------------------------------------------------------

Risk/Reward

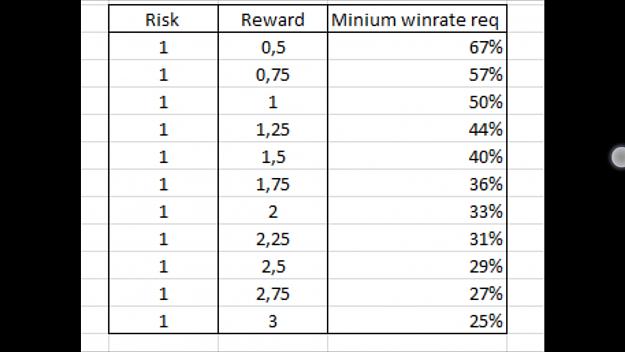

The amount of risk that you take in order to make an expected amount on a trade is known as the Risk/Reward and is expressed as a ratio. The ideal ratio is of hot debate. There are warring parities of traders (mostly retail traders) who say 1:1 is the best ratio,1:3 is better, or 1:2 is ideal. There are others who say that the ratio is completely meaningless and should be discarded altogether. Others say that a R/R is only for those who like to "set and forget" their trades of which consists only of the dumb, rookie trader crowd whom have minimal trading experience. There's a ton of differing opinions on the Risk/Reward ratio and the subsequent debates that follow can make a beginning trader confused and lead them in the wrong direction, which is dangerous for their long-term success. Let me dive in...

Most people have day jobs unlike the 'professional' traders who sit at their computer all day scouring 32 currency pairs on 12 computer screens. Not everyone will have the same time allocation as other traders so as a reuslt everyone will use different trading strategies that bend to their daily routines. The static R/R is best used for traders who don’t have the time to watch their computer screen all day long analyzing price action every 15min.

A static R/R is also good for basic EA management schemes so as to backtest a certain strategy and produce qualifying metrics.

R/R ratio is also applied differently to different types of strategies. For some strategies a static R/R serves as a guideline for their risk management. For these types of strategies there should be a minimum R/R maintained for every trade taken with the potential to increase the ratio to let winners run and ride a trend. Other strategies find the R/R irrelevant to their trade setup process (even though behind the scenes they still maintain a positive expectancy ratio unwittingly).

Here are the most popular strategies you will use in your daily trading and how R/R should be different for each one even when strategies might have the same or varying win rate:

Trending Based Systems

Exit Method: Reversals, Consolidation Zone, when trend has officially ended using custom indicator/cue (most trend strategies use this)Exit Type: Trailing Stops (dynamic), Breakeven (dynamic), Pre-determined SL/TP (static)

Calculating Metric:

Dynamic: Average Win : Average Lose

Static: R/R same for all trades

R/R should be higher (1:3 minimum) to maximize profits.

Must maintain a minimum R/R with each trade

Ideal Trader: Active involvement needed with possibility to set SL/TP to time breakouts and ride trends. 1-2 hours neededRange Based Systems

Exit Method: Based on defined market structureExit Type: Trailing Stops (dynamic), Breakeven (dynamic), Pre-determined SL/TP (static)

Calculating Metric:

Dynamic: Average Win: Average Loss

Static: R/R same for all trades

R/R should be lower (1:2 being the minimum) to boost win rate in a time where choppy markets produce more losers.

Must maintain a minimum R/R with each trade AND must not get too greedy and aim for more, strict R/R

Ideal Trader: Those who prefer ‘set it and forget it’ type of strategies where R/R ratio is static and stable with market conditions. 1 hour neededMarket Maker Systems

Exit Method: Based on defined market structure; price action evaluationExit Type: Trailing Stops (dynamic); Breakeven (dynamic); NO static TP/SL exists

Calculating Metric:

Dynamic: Average Win: Average Loss

Static: N/A

R/R cannot be calculated until after trading history is generated

Depending on what kind of market maker phase you’re trading, R/R should still be maintained at 1:3 for the trending phase and 1:2 for the consolidation/expansion phase to beat the statistical win rate odds

No minimum R/R needed

Ideal Trader: Active involvement in their trading spending 3-4 hours on the computer. Not a laid-back strategy.Dynamic Price Acton Systems (discretionary price action trader)

Exit Method: Based on price action (no clear mechanical entry/exit)Exit Type: Trailing Stops (dynamic); Breakeven (dynamic); Staggered TP/SL (dynamic) NO static TP/SL exists

Calculating Metric:

Dynamic: Average Win: Average Loss

Static: N/A

R/R cannot be calculated until after trading history is generated; it is arbitrary in this strategy

No minimum R/R needed

Ideal Trader: Active involvement in their trading spending 3-4 hours on the computer. Not a laid-back strategy. This strategy's profitability is entirely dependent upon the skill level of that trader and their understanding of price action.There isn't a ‘holy grail’ 1:2 or 1:3 ratio that must be used at all times for all strategies. Risk/Reward isn't a one size fits all number, rather it's dependent upon what underlying strategy including the type of entries, exits, and market dynamic it plays upon. You might have a 30% winning strategy with a 1:10 risk ratio and it be profitable. Or 80% winning strategy with a 2:1 risk ratio and it fail miserably.

Beware, some strategies are dependent (they are designed from the start) to revolve around the R/R. This is a slippery slope and is like trading on a House of Cards. Meaning the only way a strategy is able to win 80% of the time is BY adjusting the R/R to risk more than what it earns. These are dangerous strategies and it saturates the EA world. Adjusting the R/R to start risk more than what it earns will increase win rate and may be profitable for 6 months. But in 9 months, or a year it will fail because it's breaking an important rule to never risk more than what you earn when trading on margin.

One shouldn't start with setting an arbitrary Risk/Reward ratio and then whip the strategy into submission to fit this triangle of a number into a square strategy. Rather one should start with a strategy and then deduce the R/R from that strategy. If the R/R is not sustainable based upon the win percentage, then the underlying strategy is bad and there's no amount of tweaking the risk settings you can do to 'fix' it because then you'll inadvertently change the strategy itself when you start tinkering with the SL and TP levels.

In the end a winning strategy MUST be over 1:1 for it to be profitable regardless of win rate. 1:2 for beginners (in ranging markets), and 1:3 for beginnings (in trending markets). And it's also dependent on the type of strategy and exits that you use. If you're using a a dynamic exit then you'll never know how many pips you'll get so instead of focusing on R/R, you focus on price action and getting it right. Once you manage your trade effectively (and have the time to do so), R/R becomes irrelevant to the discretionary trader. To the automated, minimal time trader, R/R must be maintained at the minimums always in order to come out on top.

Key Points

1. Determine what kind of trader you are by figuring out how many hours a day you can dedicate to trading. Do you need a hands-on strategy or a more laid back approach? If you need hands on, then follow a strategy that capitalizes off of Trends. If you need more laid back then use a Range Based system. Or increase/decrease the timeframe that you trade. If you’re super hands on and ready to spend many hours a day then use Market Maker or Dynamic Price Actions systems where you need to react fast to moves in the market.

2. Now find a strategy that uses ONLY the market dynamic of your choice and stick to it. If you want to test a new strategy or run another strategy at the same time, do it in a separate trading account using separate money management schemes.

3. If your strategy uses dynamic exits, then R/R will not help, only the forward test results will determine the “true” Risk/Reward ratio, and at that point it is after the fact. Backtesting and forward tests are crucial. Remember that most strategies and systems that use dynamic exits fail and it's mainly due to the fact that you need to forward test in order to figure out it's true R/R and Win Rate. Forward tests of course take a lot of time, getting about 1,000 trades just for a accurate measurement (and even making 1 trade a day could take you 4 years to get up to 1,000 trades).

4. If your strategy uses static exits, then a positive R/R is critical for long-term profitability and you must use a strict 1:2 for ranging markets (not increasing or decreasing the ratio) and 1:3 for trending (not decreasing the ratio but you CAN increase the reward). When you decide on what R/R to use, make sure to never change it by risking more on "100% certain trades" or risking less on trades in a "choppy market." Doing so will invalidate your profitability metrics and is a recipe for negative growth. Stick to the same R/R once you decide on it.

5. This also applies to your % of balance at risk. Once you decide on a % to risk on each trade, DO NOT change it. Don't increase your risk on the next trade because you're 99% certain it will blast off into space and don't reduce your risk because "I don't know where the market is going so I'm place small risk". Both actions will harm your strategy by not taking full advantage of your wins and letting greed wipe out your account. If you're risking 1% on each trade (ideal for beginners and experts), stick to it at all times! If you don't have confidence in a trade setup, don't decrease the lot size, instead you skip it. There will be more opportunities.

5. Last thing to remember is that you cannot change a dynamic exit strategy into a static one without ultimately changing the strategy itself. Fitting a triangle into a square does not work without breaking something. And if you now create a new strategy, you therefore must forward test it which takes a large amount of time just to see if it's profitable in the long-run.

More trading concepts to come!