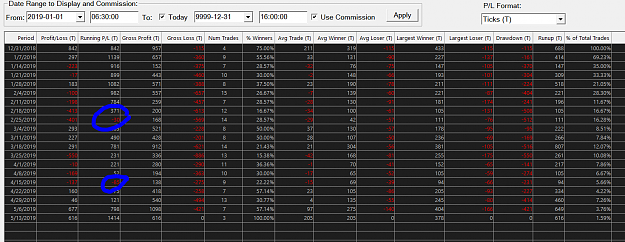

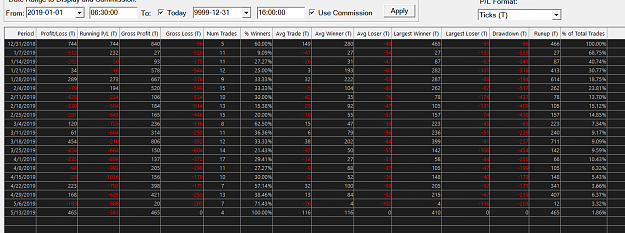

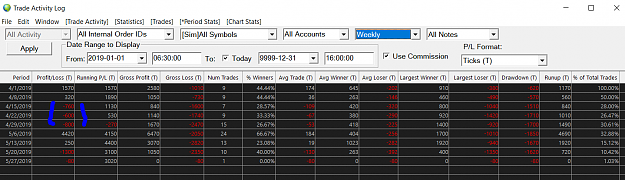

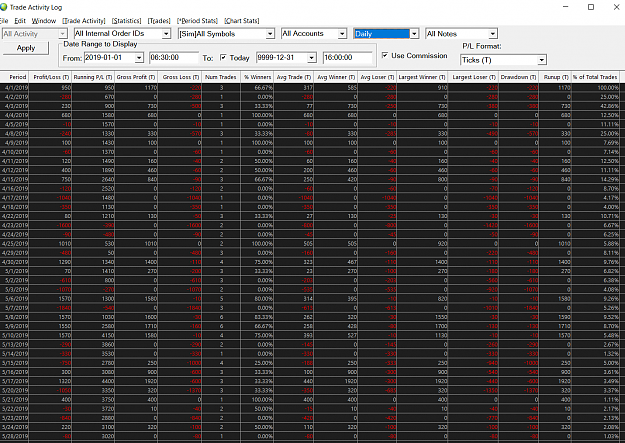

Disliked{quote} Here... one more time. 15 Min ORB with SL @ 0.5xRange and TP @ 2xRange. This equates Reward to be 4 times the Risk and it is still a loser! Anyone who trades NQ would learn how easy it is for a Trend Following strategy to decay during ranging period. Just run any algo in Jan to feel good, then comes feb/mar for slow decay to appear and come april, losses accumulate into a new losing strategy. Better if you list all the filters. I am sure I have not tried every possible permutation and combination :-) {image}Ignored

why? because of fundamental reasons.

NQ represents a stock index. Usually stock indices tends to mean revert; rather than trend.

It may work in the medium to longer term on stock indices. for example; breakout in daily timeframe; such as a breakout from a 5 day range. This is because stock market tends to trend up in the long term.

Perhaps consider "Long Only" for NQ; since there is a bullish bias in stock market over the long term

2