{quote} Is there no software that does it? Playing with numbers can't be that hard. Yes, it's for ALL major FX pairs and one derivative designed especially for the EURAUD and EURNZD

Ignored

There should be something available and frankly I have not searched for it. I like to build stuff on my own to understand the inner workings myself instead of forming a bias from what I read elsewhere. finviz might have something already available.

Anyone here trades stat arb models instead of indicator based systems? I have developed one (out of curiosity that involves basically the DOLLAR (Index)) and it works extremely well.

Ignored

can you shed some light here. are you referring to basket formation with weights etc?

{quote} can you shed some light here. are you referring to basket formation with weights etc? is it momentum or mean reversion?

Ignored

It's supposed for mean reversion (but also can be used for blatant momentum setups).

Normally it would be a basket (weighted) to trade against some pairs (equal weight), but i managed to bring everything down to only two pairs: EURAUD and EURNZD

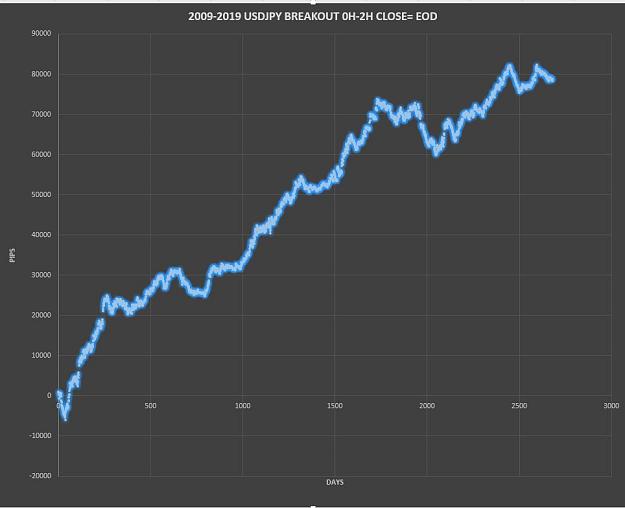

USDJPY 0H-2H BREAKOUT RESULTS: Profit factor = 1.22 avgPips = 2.92 #trades = 2681 2009-2019 transactionCosts = NO Timeframe = 1min Probably it needs some filter to overcome the transaction costs and make it profitable, but there is some edge as Alpha pointed out {image}

Ignored

nice work. pretty much similar results to mine

Vee: this is your opportunity to make some bucks. the edge still exists. it works on both usdjpy and dax.

{quote} I am also hoping anyone can prove me (or CP) wrong when I say "Any strategy that trades every buy and sell signal on a price/time series will fail in producing consistent returns". I tried to prove this wrong and I could not. I think CP is right. There is something about directional bias that makes a strategy win or lose in the long run.

Ignored

Ok, time for some theoretical nonsense:

Although alpha doesn't like it, there needs to be an edge in trading. What does it mean to have an edge? It means that the strategy needs to make you winning (P) more than you lose (L). If your win rate is r, any successful strategy should fulfill the inequality L < r × P.

There are only a few scenario I could think of how to make this work:

Add to winners to increase the potential profit.

Enter with one indicator and exit with the signals of another indicator.

1: The problem with this attempt is that (from my experience) you'll always deteriorate the parameter r with increasing R:R. Thus, in the long run you'll alwys lose with a strategy like the one shown in the link.

2: I've only partly surveyed that strategy (there's still a lot of work to do). No, I haven't found an edge yet. Assume that your statement above is true: The use of 1 indicator for entries and exits will always yield losses in the long term. Now let's assume that you use 2 indicators, one for entries (e.g. determining momentum and enter if you see strong momentum) and another for exits (e.g. another momentum indicator that tells you that momentum flattens). If the signals of both indicators are still highly correlated, you would still lose. But what would happen if the correlation of the indicators is almost 0? How could it be established? Maybe using a lagging and a less lagging indicator.

{quote} I have already tried this strategy what you posted earlier. It's a loser on NQ as after 2 hours of NYSE, most likely price reverses (unless on very strong trending days like we had in january) ....

Ignored

Vee, I am not sure what you are trying to get at.

this strategy that I presented; has an edge on USDJPY.

I re-run the backtest; and have similar results to DavidRP; with extremely simple rules:

- backtest date range: 2011 to present day; using tick data (raw bid/ask)

- buy when the price breakout from the first 2 hours range (GMT 00:00 - GMT 02:00) (opposite for sell)

- Exit on opposite signal

- Exit at end of day (NY 16:45)

I haven't used any stop loss, neither profit target, neither trailing stop.

since the curve is positive; there is an edge in this strategy.

You can enhance the strategy by various filters, and exit techniques.

If you can't see an edge in this equity curve; then I can't help you.

Although alpha doesn't like it, there needs to be an edge in trading. What does it mean to have an edge? It means that the strategy needs to make you winning (P) more than you lose (L). If your win rate is r, any successful strategy should fulfill the inequality L < r × P.

There are only a few scenario I could think of how to make this work:

Add to winners to increase the potential profit.

Enter with one indicator and exit with the signals of another indicator.

...

Ignored

I beleive either way is correct to define an edge:

- use same indicator for entry and exit

- use different indicators for entry and exit

it doesn't matter. As long as you find a statistically significant result of positive result; is all it matters.

When I am presented with a trading idea; I always try to test the entry and exit using the same rule (aka indicator); and I assume transaction cost are zero (spread = 0, and commission = 0). If I get a positive equity curve; then there is an edge.

The next step is to overcome transaction cost by introducing entry and exit filters; or even other indicators for that matter.

I try not to mix strategies onto one (like Vee is doing in NQ). It is far easier to treat every type separately. You can then study correlation to help allocate capital.

{quote} Dude - I am only focused on NQ and nothing else and only during NYSE session and only with 2019 data. NQ has a completely different footprint. It can work but it will also cause DD using rangy days (similar to any breakout style) Is there any way you can load tick data of NQ in your backtester? I could use some help as Sierra limits to 90 days max. I can no longer test with January tick data now :-(

Ignored

I don't trade NQ; and I don't have have the data.

Ony forex dude

As I mentioned earlier; the open range breakout strategy; only works on USDJPY. I published the strategy here for you to consider in your trading; since you asked me for it earlier.

{quote} Vee, I am not sure what you are trying to get at. this strategy that I presented; has an edge on USDJPY. I re-run the backtest; and have similar results to DavidRP; with extremely simple rules: - backtest date range: 2011 to present day; using tick data (raw bid/ask) - buy when the price breakout from the first 2 hours range (GMT 00:00 - GMT 02:00) (opposite for sell) - Exit on opposite signal - Exit at end of day (NY 16:45) I haven't used any stop loss, neither profit target, neither trailing stop. since the curve is positive; there is...

Ignored

highlighting areas where human intervention will take place..

good luck if you started the equity curve where the blue line is...that's torture right there. You seriously think there's an edge here..that's almost 3 years of stagnant performance!

{quote} I hate to even mention this as it just sounds retarded but I will say it anyway (this is specific only to NQ and only during NYSE)....of all my testing rigor, the only 'approach' I have found till date feasible and close to my overall success criteria is to do the following Entry via brute force across multiple strategies specific to trending or ranging market. (I remain unsuccessful to devise a strategy that will work in both market conditions but I am getting there with the HHLLHLLH market structure!) enter with no SL and small TP like...

Ignored

V, by all means, as long as you get a statistically significant number.

you have to decide though, to go autonated or manual. doing both is a recipe for disaster

{quote} highlighting areas where human intervention will take place.. good luck if you started the equity curve where the blue line is...that's torture right there. You seriously think there's an edge here..that's almost 3 years of stagnant performance! {image}

Ignored

Hilmy, that curve is the raw edge curve. you have to add some filters or exit techniques to improve it.

{quote} Hilmy, that curve is the raw edge curve. you have to add some filters or exit techniques to improve it. in my real strat, i use multiple TP levels. that is where traders can add value. the edge exists

Ignored

Then technically breakout and reversion entry both have raw edge to them. You're basically extracting 1 of 2 fundamental market moves as a baseline. I wouldn't classify it as an "edge", it's just how the market moves lol

How does a filtered raw curve looks like for the one you posted?

By the way, I think the word "trading edge" is thrown around without fully understanding of what it means

from investopedia:

A trading edge is a technique, observation or approach that creates a cash advantage over other market players. It doesn’t have to be elaborate to fulfill its purpose; anything that adds a few points to the winning side of an equation builds an edge that lasts a lifetime. Don’t be frustrated if you haven’t found one yet because the majority of traders don’t even know it exists. It’s the primary reason why a few book excellent profits while everyone else struggles with weak or negative returns.

So now this begs the question back to your raw edge post; is breakout setup considered an edge? (or any pattern setup)

Based on the definition, no. There will be many players trading the same patterns at any given time. If traders all trade different patterns, then the performance should narrow to 50% over the long term as vee said. Some days you win and some days you lose because of what Mark Douglas describe as forces of other traders to invalidate your setup.

I would maybe classify order flow reading as an attainable edge because it's not fully mechanical system and does require experience that most retail traders dont' bother to look into.

I agree the edge is a combination of these "filters" and discipline. Even with algo, that discipline still needs to be there (avoiding intervention) ESPECIALLY if it has DD over the span of days or weeks.

By the way, I think the word "trading edge" is thrown around without fully understanding of what it means from investopedia: A trading edge is a technique, observation or approach that creates a cash advantage over other market players. It doesn’t have to be elaborate to fulfill its purpose; anything that adds a few points to the winning side of an equation builds an edge that lasts a lifetime. Don’t be frustrated if you haven’t found one yet because the majority of traders don’t even know it exists. It’s the primary reason why a few book excellent...

Ignored

totally disagree. this is a perfect edge. It is alpha.

you trade an open range breakout. it doesn't matter how many people trade it. it is an edge; because it is statistically significant over a period of time.

why other currency pairs does not exhibits this behavior? only USDJPY? there are hidden reasons why it works that way; and I don't care about the reasons. It's all about statistics.

Another way of definign edge; it is better than random (50/50 coin toss). Use ANOVA to study the statistics of a trading system; compared to a random system.

ANOVA will show that the performance of both curves; are statistically different with a 95% confidence.

In the past; there used to be an edge in USDJPY; once a month; bank of Japan used to do some shitty large transaction; which will impact JPY negatively (basically trying to make JPY cheaper for exports). Many traders took advantage of that; until BOJ made that transaction random.

There are many *interesting* ways how the Japanese economy works; which is quite different to other economies. Understanding those; gives you an edge.

{quote} great discussion... exactly the type we should be having to grow our knowledge and skill in this space. I feel I struggle more than others because of the variety of channeled thought process I find myself in frequently. Not sure if it is a good thing or bad thing yet but I do find it extremely hard to convert a "raw edge" whatever that is... into a provable working edge by the so-called filtration process. In my experience the opposite has happened... the freaking edge (or the illusion of edge if you will) starts to DECAY the moment I introduce...

Ignored

Vee, I am going to stress this again and again; you are trying to combine many systems onto one; which does not work.

keep it simple. develop one single strategy that works; trade it live mechanically; then add other strats on the way.

the way you are proceeding; you are not going to go anywhere am afraid.

I am surprised you are an engineer and you don't know that.

The secret to engineering (especially software engineering); is to break down a complex problem onto smaller problems; that can be solved one by one.

btw; I am perhaps more engineer than any of you in FF; lol am serious.

An edge is the probability of X-tick price movement in one direction over Y-ticks price movement in the opposite direction after an objective signal.

If an edge does indeed exist, then consistent execution is all that is required. Grinding, day in and day out. This definition of an edge coupled with consistent execution puts the law of large number on your side, not against you.

Note, if the objective signal is actually subjective, then the trading becomes completely discretionary and the results are based on the traders "ability/skill" (good luck quantifying that).

Also note, if consistent execution is not possible, for whatever reason, the law of large number is no longer on your side.

Without risk parameters edges cannot exist. In order to measure the probability of EVENT-A over EVENT-B, both Events must be pre-defined, otherwise we are not measuring probability, but rather baking girl scout cookies!