DislikedSo, we can assume that price on a demo account: - is less random - is easier to read - has less fake breakouts Conclusion: Should we then base our live entries on demo charts? Why or why not?Ignored

For example, being a quantitative trader my whole existence is pretty well based on rigorous data mining methods....hence backtesting/ walk forward/ demo and live testing is a major part of the game. As a result you need to carefully check all your assumptions.

Given the random method in which MT4 constructs bars outside of control points the first thing you need to be aware of is forget tick data and start to rely on either control points or open only conditions in your strategy design. The best you are going to get is by using M1 control points or open price data in your testing. The rest is simply random construction.

By all means use Dukascopy tick data to construct your long range timeframe bars for use by your preferred testing platform such as MT4....but don't bother about testing on tick data within MT4. For example, if you are testing a D1 strategy then use M1 control points or open only conditions as you means to test it's efficacy. Tick data is both useless for MT4 and an exorbitant waste of time and processing power of your PC. There is not enough material variation from this premise to warrant the time and effort in obtaining the mythical 99.90% accuracy....unless you are trading at the scalping timeframes.

Discretionary traders are never going to be able to make this comparatison....but systematic traders can, based on the application of precise entry and exit rules based on a control point setting that is more reliable. More often than not it is the inexperience of the coder as opposed to the reliability of the broker feed that causes problems in this area.

Attached Image (click to enlarge)

The control points of most regulated ECN broker feeds are going to be similar but there will be variation caused by GMT offset as this impacts on the control points themselves. If they weren't then it is unlikely they will stay regulated for very long. That means if you have sufficient data history on a timeframe, then test your strategies on the brokers platforms that you plan to go live on.

In regards to broker feeds....as mentioned earlier, there is so much variation in live feeds let alone demo versus live feeds. This in part is attributed to the decentralized nature of FX pricing and a host of other material factors which has been discussed in this thread.

The way I get consistency in testing to ensure that variations between live and test results are not material in nature (they will never be exact due to price perturbations in latency etc.) is to use the open condition on all testing.

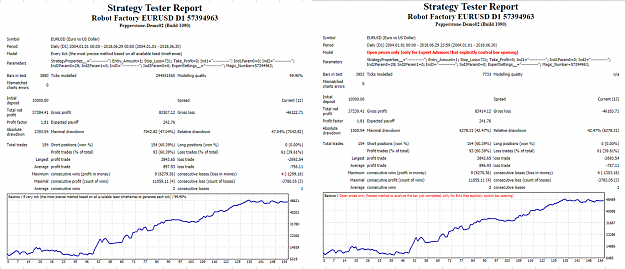

For example here is a D1 strategy result from a live feed and demo feed from FXOPen. I do not regard the variations as material to the outcome...hence I am happy with this degree of variation.....but note the spread difference between these test results. This is when you ask the reason why? with your broker.

Attached Image (click to enlarge)

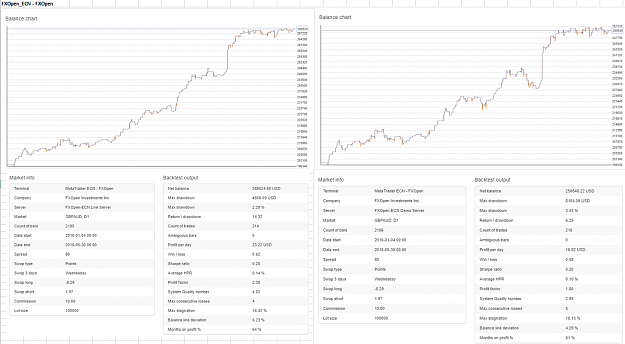

Now have a look at the same strategy applied to Darwinex Live

Attached Image (click to enlarge)

It would be easy to conclude that there was something dodgy going on between these two brokers but the difference relates to GMT offsets, SWAP and spread/commission as opposed to the data feed itself. For example as this strategy works off the open condition in terms of entires and exits....a change in GMT will cause major perturbations in the outcome. This is not a broker issue but a user issue that you need to be aware of.

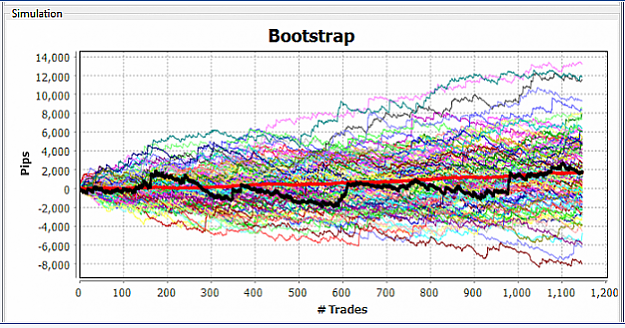

The bottom line is this.....you need a method of comparing feeds and applied current assumptions such as SWAP, slippage, spread/commissions if you are going to use any form of testing as a rigorous basis to test the efficacy of any live strategy. You are kidding yourselves if you don't take testing seriously as minor perturbations in data totally skew your return streams over time and your return stream results will have no decipherable meaning in terms of what is a robust result versus a poor or random result.

Attached Image (click to enlarge)

3