We are starting to get a logical narrative by testing the options.

Here is where I am at currently. The better options need to be crunched across the portfolio and across a long time series when the EA is fully complete.

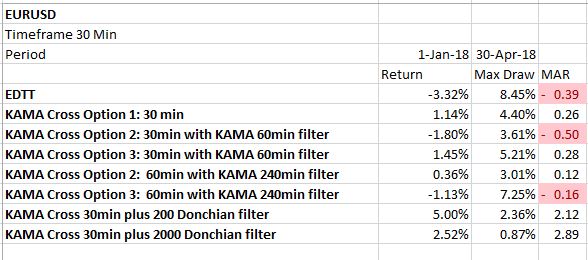

The MAR is what we are after. Interesting that the KAMA cross on 30 min plus 2000 Donchian is our closest proxy for EDTT and it appears to do very well in comparison. This may offer some hope in our direction we take with Instant Karma. Same as EDTT.....stay out of the shit and only strike when excursions take a long move away from the mean.....eg...in the mid range of a trend as opposed to catching all of it. :-)

Karma Variations on EURUSD We are starting to get a logical narrative by testing the options. Here is where I am at currently. The better options need to be crunched across the portfolio and across a long time series when the EA is fully complete. The MAR is what we are after. Interesting that the KAMA cross on 30 min plus 2000 Donchian is our closest proxy for EDTT and it appears to do very well in comparison. This may offer some hope in our direction we take with Instant Karma. Same as EDTT.....stay out of the shit and only strike when excursions...

Ignored

I arrived at the same conclusion comparing my manual testing from yesterday on 2 years of data on copper and today's EA testing. Significant lows/highs as a filter make complete difference. As between night and day.

Also we can add hard SL option, as sometimes price moves so fast, that it makes loss larger than expected max risk.

In the event similar to Swiss Franc depeg in 2015, we will lose much less, than waiting for cross back.

Cut short your losses. Let your profits run on. David Ricardo (1772-1823)

{quote} I arrived at the same conclusion comparing my manual testing from yesterday on copper and today's EA testing. Significant lows/highs as a filter make complete difference. As between night and day.

{quote}Also we can add hard SL option, as sometimes price moves so fast, that it makes loss larger than expected max risk. In the event similar to Swiss Franc depeg in 2015, we will lose much less, than waiting for cross back.

Ignored

Yep it may be necessary......

I am now back to manual testing and having a bit of joy with the following on EURUSD. I noticed the similarity between EDTT and Karma on the 30 minute timeframe as posted before...which made me think what if we approach momentum the same way with Karma.

The test I am running is as follows. I have a split screen with a M30 chart above and a M5 chart below. I apply a Donchian 2000 channel to the M30 chart and only enter trades when a new high or low of the Donchian is achieved. When the Donchian break occurs I release two trades. 1 trade configured to the KAMA cross on the M30 and 1 trade configured to the KAMA cross on the M5 timeframe. This is attempting to replicate what we do on EDTT.

Both trades are set for position sizing based (at this stage on ATR) for their respective timeframes....however this is going to change as ATR has its issues...anyway the M5 timeframe is always going to exit earlier than the M30 timeframe....however if a new high or low is reached on the M30 timeframe with the Donchian....then go again on the M5 at that point. This therefore allows M5 to have multiple bites on the same M30 cherry.

So far over a difficult period 1 Jan 2016 to 30 April 2016 I am producing far better MAR than I was with EDTT.

I will keep testing to 30 April 2018 and let you know the result.

We have been fishing for the past few days with some nibbles and lot's of false hooks.....but we may be on a game changer with the approach described in the last post R. It is blowing EDTT away. Still need to test across a broad universe once the EA is finalised.....but the results of the adapted technique are just too materially different to be random chance.

The best thing is that this appears really powerful and we can still keep EDTT as this is clearly going to offer correlation benefits.:-)

I never got this with EURUSD on EDTT over the same range despite the activity occurring in the same region of market condition.

We have been fishing for the past few days with some nibbles and lot's of false hooks.....but we may be on a game changer with the approach described in the last post R. It is blowing EDTT away. Still need to test across a broad universe once the EA is finalised.....but the results of the adapted technique are just too materially different to be random chance. The best thing is that this appears really powerful and we can still keep EDTT as this is clearly going to offer correlation benefits.:-) I never got this with EURUSD on EDTT over the same...

Ignored

Great stuff! If this is the way to filter the noise, it can be used in any time frame, because main disadvantage is the capacity in these small time frames.

What value of ATR you use for 5m and 30m? I don't think it is daily ATR?

Cut short your losses. Let your profits run on. David Ricardo (1772-1823)

{quote} Great stuff! If this is the way to filter the noise, it can be used in any time frame, because main disadvantage is the capacity in these small time frames. What value of ATR you use for 5m and 30m? I don't think it is daily ATR?

Ignored

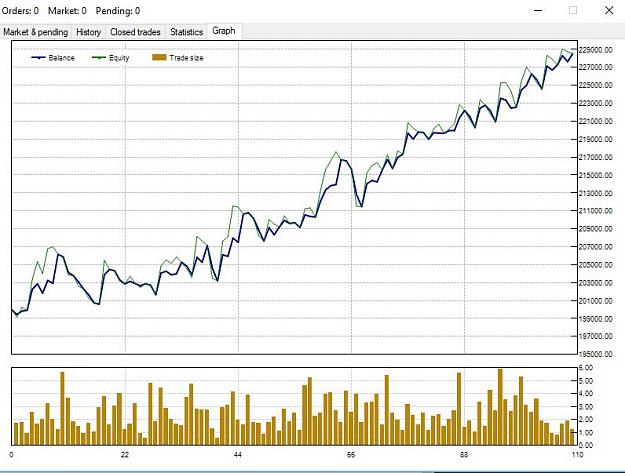

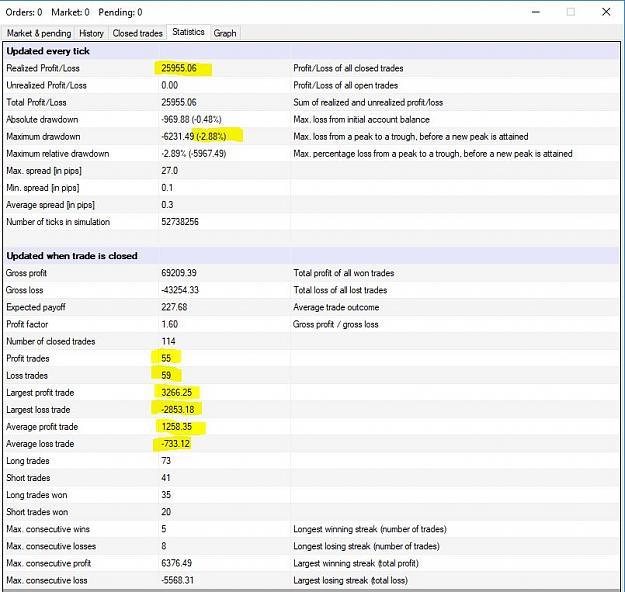

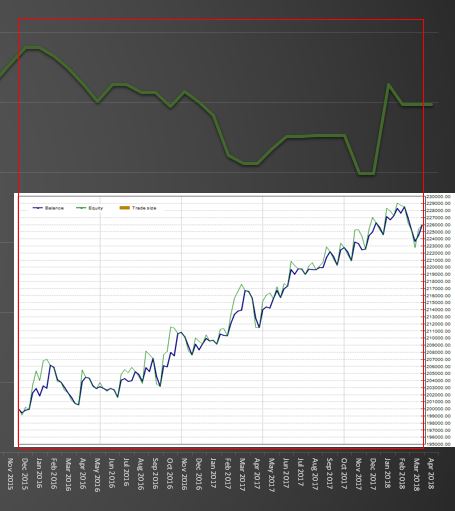

Mate I am using a 14 ATR for each timeframe to get good position sizing on entry. I think the stops solution is not going to work.....but I really don't think we need it. Here is a sneak preview of EURUSD since 1 Jan 2016 to 16 Feb 2018. Clearly non-random in nature and what we are after. Almost finished and will have the stats up shortly.

EURUSD 1 Jan 2016 to 30 April 2018

Position sizing based on fixed risk of $500 but no stops - Performance exit only

CAGR 5.37%

Max Draw 2.88% MAR 1.86

How do you like them apples R :-) Notice the equity curve and no reliance on a single major outlier. This is a different game to EDTT and I am liking it.

Tomorrow if I have time I will put my best and worst in EDTT to the test and see how this copes. I am knackered mate. Cheers till tomorrow.

Inserted Video

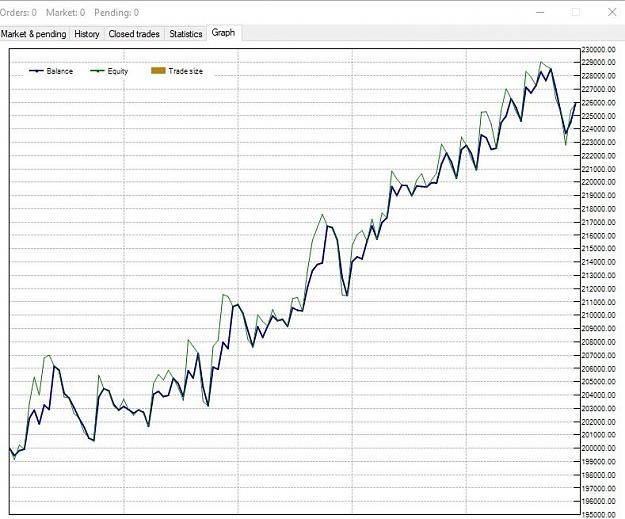

PS Forgot to add equity curve comparison against EDTT on EURUSD. Note the significant correlated nature when it counts and the uncorrelated nature when it doesn't. This is going to be a fine complement to the portfolio methinks :-)

Results {image} {image} EURUSD 1 Jan 2016 to 30 April 2018 Position sizing based on fixed risk of $500 but no stops - Performance exit only CAGR 5.37% Max Draw 2.88% MAR 1.86 How do you like them apples R :-) Notice the equity curve and no reliance on a single major outlier. This is a different game to EDTT and I am liking it. Tomorrow if I have time I will put my best and worst in EDTT to the test and see how this copes. I am knackered mate. Cheers till tomorrow.

Ignored

Impressive! Am I getting this right: You are using KAMA cross only for exiting the trade (on M30 resp. M5), but the entry will alway be a new high or low on the M30 with the Donchian 2000?

{quote} Impressive! Am I getting this right: You are using KAMA cross only for exiting the trade (on M30 resp. M5), but the entry will alway be a new high or low on the M30 with the Donchian 2000?

Ignored

That's it S in a nutshell :-) A slight nuance however is that all trade activity is actually conducted on M5 based on the close of the M5 bar..... as we synchronise entry on M5 for both M30 trades and M5 trades but my filter is the M30.....if that makes sense.

Below is a visual way to hopefully get across what I mean. Let me know if this is sufficiently clear. I better hit the sack mate. Cheers C

{quote} That's it S in a nutshell :-) A slight nuance however is that all trade activity is actually conducted on M5 based on the close of the M5 bar..... as we synchronise entry on M5 for both M30 trades and M5 trades but my filter is the M30.....if that makes sense. Below is a visual way to hopefully get across what I mean. Let me know if this is sufficiently clear. I better hit the sack mate. Cheers C {image}

Hello I have a noob question , how do you calculate the position size using only ATR ? for example : 10000$ account , 1% risk , current ATR(14) = 0.0014.

Ignored

Hi MP.

I am just hitting bed....and if you don't get a response from anyone...then I will respond tomorrow mate. Must sleep get....words can't muddled :-)

Results {image} {image} EURUSD 1 Jan 2016 to 30 April 2018 Position sizing based on fixed risk of $500 but no stops - Performance exit only CAGR 5.37% Max Draw 2.88% MAR 1.86 How do you like them apples R :-) Notice the equity curve and no reliance on a single major outlier. This is a different game to EDTT and I am liking it. Tomorrow if I have time I will put my best and worst in EDTT to the test and see how this copes. I am knackered mate. Cheers till tomorrow. https://www.youtube.com/watch?v=HFfh...xS99D_nWZI2EwT...

Ignored

This is beautiful!

Attached Image

Cut short your losses. Let your profits run on. David Ricardo (1772-1823)

Hello I have a noob question , how do you calculate the position size using only ATR ? for example : 10000$ account , 1% risk , current ATR(14) = 0.0014.

Ignored

So let's say this is 14 pips ATR. Your theoretical SL from entry should be 14 pips and with this SL, you risk 1% of your capital i.e 100 USD. You can use hard SL or not, but this is how you calculate your position size.

{quote} Hi MP. I am just hitting bed....and if you don't get a response from anyone...then I will respond tomorrow mate. Must sleep get....words can't muddled :-) Cheers mate :-) C

Ignored

How can you fall asleep with discovery of this magnitude?

Attached Image

Cut short your losses. Let your profits run on. David Ricardo (1772-1823)

{quote} So let's say this is 14 pips ATR. Your theoretical SL from entry should be 14 pips and with this SL, you risk 1% of your capital i.e 100 USD. You can use hard SL or not, but this is how you calculate your position size. You can use some calculator online to make it easy. Like here: https://www.babypips.com/tools/position-size-calculator Also if you are new, please read whole course there - it is free. I am using EA for calculating positions https://www.mql5.com/en/market/product/5398 for many years now and it is super...

Ignored

Thanks Ramadas I appreciate it , that's what I thought too , what confuse me after reading your's and C the last few posts is your indecisiveness of using a hard sl as an alternative to ATR , but doesn't an ATR SL "as you described above" still be considered as hard SL keeping in mind that you're going to exit the position once youhit your max predefined risk level

{quote} Nice M. Totally agree mate and it appears that the heavy duty Fund Managers in the diversified trend following space also agree with this verdict regarding equities such as Nick Radge, and Andreas Clenow. They simply refuse to adopt short strategies in equities and most tend to adopt rotational absolute momentum strategies in this space. Clenow's book "Stocks on the Move" gives some great examples on how to deploy this natural long only bias...

Ignored

sorry for the late replay, very bussy at the moment. thanks for the book, i will read it maybe next week

Joined Oct 2009

|

Status: Exploiting psychology of the crowds

|1,426 Posts

Ernest Chan in his book Algorithmic Trading: Winning Strategies and Their Rationale (Wiley Trading)

postulates that some markets are more mean reverting and some are more divergent.

For example if you would create spread between Brent and WTI, this would be convergent or mean reverting market. We know that stuff happens that such market goes haywire and deletes money on your account. As it was with LTCM. That's why we stick with divergent and positive skewed strategies.

But if some markets show more convergent nature like EUR GBP, AUD NZD, AUD CAD, NOK SEK, and I think we should mainly test such markets in effort to try to break our strategy.

Attached Image (click to enlarge)

Attached Image (click to enlarge)

He is using Hurst component to gauge trendiness of the given time series:

Attached Image (click to enlarge)

USD CAD is weakly mean reverting.

Attached Image (click to enlarge)

Attached Image (click to enlarge)

AUD CAD are fundamentally mean reverting until something big happens.

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Cut short your losses. Let your profits run on. David Ricardo (1772-1823)

{quote} Thanks Ramadas I appreciate it , that's what I thought too , what confuse me after reading your's and C the last few posts is your indecisiveness of using a hard sl as an alternative to ATR , but doesn't an ATR SL "as you described above" still be considered as hard SL keeping in mind that you're going to exit the position once youhit your max predefined risk level

Ignored

Morning MP. Just popping in for a quick response as I need to do other stuff today.

What Ramadas said....but we really do not use ATR as a stop at all. ATR is used as though we actually were placing a stop at a defined location to determine position sizing only and then we remove the hard stop and simply wait until the KAMA crossover to exit. This is what we refer to as a performance exit as opposed to a hard stop or trailing stop technique.

This means that the theoretical stop of the ATR can and will be breached price with adverse price movements and if trading a single strategy in isolation.....would not be advised....however we can relax our assumptions about this adverse risk management measure on a single instrument provided our trade risk percentage is a fraction of our risk exposure. In this theoretical instance our risk exposure per trade is $500 on a $200K account or 0.25% trade risk. The lagging nature of the performance exit does mean that this risk threshold is frequently exceeded....but as with many mean reverting *convergent* strategies....this is a risk we absorb by the portfolio approach.....not to be advised for a trader using a single system.

There will occasionally be extreme adverse moves such as the Swissy depeg....but the slippage on that event was 2% on my testing with a 0.25% trade risk applied....which in the scheme of things is not world shattering for the portfolio....and not a margin call event or anywhere near that. Just a nasty reminder of the how fast the market can adversely move your position.

You need to balance this risk exposure against the impact of a fixed stop to your system which by it's nature *introduces* drawdown into your system performance. A stop loss is always placed at an adverse position so if it is frequently hit... by it's very definition you will start receiving drawdowns. A performance exit however is based on an adverse characteristic of the market itself as opposed to the simple arbitrary risk management placement of a stop. Under a portfolio you can therefore consider it.....and you will be amazed at how your performance metrics will be improved.

Here are two excellent podcasts on the subject which you should sink your teeth into. Cesar Alvarez and Alan Clement