{quote} I couldn't find a reliable MT4 VWAP indicator. I coded one some time ago but it wasn't that good. I appreciate if you can share yours. All the best, Khalil

{quote} I couldn't find a reliable MT4 VWAP indicator. I coded one some time ago but it wasn't that good. I appreciate if you can share yours. All the best, Khalil

Ignored

vwap is calculated on ticks; however in MT4 I found the nearest almost identical indicator to vwap is to do SMA of pivot on 1m bars since start of day

Remarks: Volume slowing down... chop expected. Chop = regression towards VWAP. Some news later on.

Some issues regarding trading chop:

- give stoploss little more space.. channels become wider..price is a little erratic. It can go a little past supporting trendlines..etc..

- take profits quickly.. even if price looks like going nuts..it probably will return just as easy.

When trading trend (away from VWAP) my entry has to be perfect. one tick after BO... no quick gain = out.. Totally different way of trading.

So will we get continuation down from yesterday? I don't know...but if I wanted to sell a lot I'd wait until after the news.

Ivo

Attached Image

Trouble lies in what we believe to know for sure that just ain't so.

{quote} vwap is calculated on ticks; however in MT4 I found the nearest almost identical indicator to vwap is to do SMA of pivot on 1m bars since start of day

Ignored

Hello alphadude,

would you mind to post an example?

It sounds very interesting

many thanks

regards

v

When long, the "action" at this moment is hold. The action after BO is always hold.

We broke 2 trendlines, stayed outside the channel for one complete bar (which makes the BO valid). So we wait for another point3 up.

Besides this we broke the VWAP.

As a general rule of thumb: it went up 4 bars, so I give it 8 bars to make the point 3 up.

Ivo

Attached Image

Trouble lies in what we believe to know for sure that just ain't so.

{quote} vwap is calculated on ticks; however in MT4 I found the nearest almost identical indicator to vwap is to do SMA of pivot on 1m bars since start of day

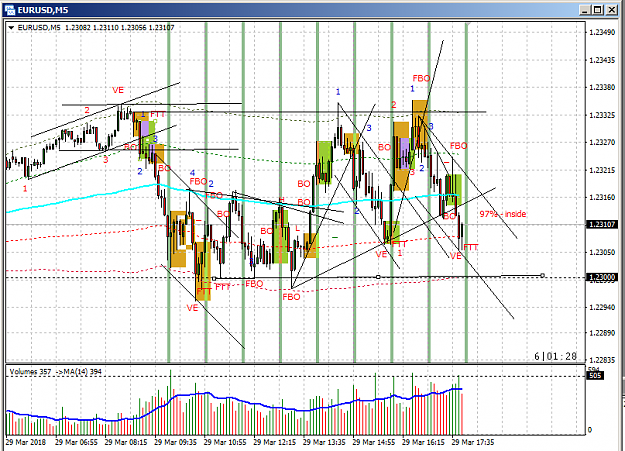

Choppy day today, not easy. Collected couple of pips but nothing big. Once a trend is on the way it's over.

GLOSSERY

VE: volatility extension: left trendline is pushed away. Good moment to take profits. Often precedes FTT and "change" especially during choppy day. BO: breakout. After this we expect a point 3. If we have a position we hold. FBO: failed breakout. Often makes a point 1 in new direction or point 3 or 4 in the original channel direction. FTT: failure to traverse: Price trying to touch Left trendline but cannot make it. Often makes a point 1 or point 3 of bigger channel. Point 1-2-3: 1-2 = move, 2-3 = retracement 3 = continuation Point 3: Expected after 1-2: This is the moment of entry. So we patiently wait for point 1, breakout (or a move of 3+ bars), point 2, retracement, point 3: continuation. Point 4: second point 3 formed by an FBO. VWAP: Volume Weighted Average price.

Ivo

Attached Image (click to enlarge)

Trouble lies in what we believe to know for sure that just ain't so.

{quote} Hello alphadude, would you mind to post an example? It sounds very interesting many thanks regards v

Ignored

attached is an example from recent 3 days on EURUSD

1. Pivot of 1m bar: (High+Low+close)/3

2. calculate how many bars since start of day (you can use any timezone you like for start of day)

3. Calculate the sum of the pivots of all these bars

4. Divide the sum by the number of bars (from step 3)

I have tried calculating VWAP including the volume (ticks in MT4); and the result were the same as using the above method

BTW: Vwap can be calculated on any timeframe; for example; daily VWAP (start from trading day), hourly VWAP (start from each hour bar), 5m VWAP (start from each 5m bar), etc. however institutional traders; usually use VWAP of the trading session they are in

{quote} attached is an example from recent 3 days on EURUSD 1. Pivot of 1m bar: (High+Low+close)/3 2. calculate how many bars since start of day (you can use any timezone you like for start of day) 3. Calculate the sum of the pivots of all these bars 4. Divide the sum by the number of bars (from step 3) I have tried calculating VWAP including the volume (ticks in MT4); and the result were the same as using the above method BTW: Vwap can be calculated on any timeframe; for example; daily VWAP (start from trading day), hourly VWAP (start from each...

Ignored

Nice calculation and it probably looks quite the same but you're missing the volume which is exactly what VWAP uses

Yes, it looks the same across all timeframes. So it's kind of a true display of the average price that was paid. The mother of all moving averages so to speak.

>however institutional traders; usually use VWAP of the trading session they are in best

Yes. If a client wants to buy the trading firm gets paid extra/bonus/commission for any price below the VWAP and vice versa. They get it cheap then. There are always many orders around it. It´s considered a fair price and on itself it does act like support/resistance.

Ivo

Trouble lies in what we believe to know for sure that just ain't so.

{quote} Nice calculation and it probably looks quite the same but you're missing the volume which is exactly what VWAP uses TotalPV+=Volume*((Low+High+Close)/3); TotalVolume+=Volume; VWAP=TotalPV/TotalVolume; > Vwap can be calculated on any timeframe; Yes, it looks the same across all timeframes. So it's kind of a true display of the average price that was paid. The mother of all moving averages so to speak. >however institutional traders; usually use VWAP of the trading session they are in best Yes. If a client wants to buy the trading...

Ignored

in FX you dont have the true FX volume.

vwap is not the same on all timeframes; you need to calculate it on tick data. if you dont have it; use 1m data. the higher the timeframe the higher the calculation error

if you dont have tick data and volume data; then vwap on 1m pivot data is as close as you can get to true vwap

{quote} attached is an example from recent 3 days on EURUSD 1. Pivot of 1m bar: (High+Low+close)/3 2. calculate how many bars since start of day (you can use any timezone you like for start of day) 3. Calculate the sum of the pivots of all these bars 4. Divide the sum by the number of bars (from step 3) I have tried calculating VWAP including the volume (ticks in MT4); and the result were the same as using the above method BTW: Vwap can be calculated on any timeframe; for example; daily VWAP (start from trading day), hourly VWAP (start from each...

Ignored

many thanks for the chart and for the explanation

v

{quote} attached is an example from recent 3 days on EURUSD 1. Pivot of 1m bar: (High+Low+close)/3 2. calculate how many bars since start of day (you can use any timezone you like for start of day) 3. Calculate the sum of the pivots of all these bars 4. Divide the sum by the number of bars (from step 3) I have tried calculating VWAP including the volume (ticks in MT4); and the result were the same as using the above method BTW: Vwap can be calculated on any timeframe; for example; daily VWAP (start from trading day), hourly VWAP (start from each...

Ignored

Hi Alpha,

What about real time pivots for the trading day? A brief explanation:

Every minute passes during the current day you calculate (High(Today) + Low(Today) + Close(ThisMinute))/3

High, Low and Close values are the values realized up to that minute.

Just an idea...

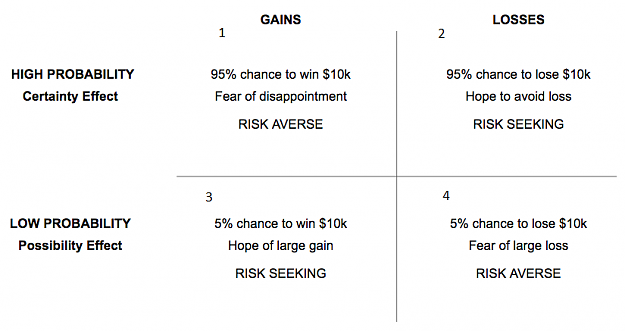

I'm a big student of Kahneman.. here is his quadruple matrix.

It explains our irrational behavior under uncertainty.

Quadrant 2/3: holding on to losers.. hoping it will be okay.

This also explains among other things why we bet everything to make up for a still manageable loss, risking a catastrophic loss.

It explains why we take stupid trades in choppy markets under less than ideal circumstances.. Why we keep on trying and trying when it's just not the day.. (Q 3)

Quadrant 1/4: We have a decent win...and it can become enormous.. but just to be sure we take profits...

The day is perfect.. we see everything right, but we just don't milk it.

It explains why during high volatility and high probability periods we can freeze.. (Q1)... --> to avoid disappointment in case it doesn't work out.

The key: be aware... don't be too much risk seeking....don't be too risk averse.. When you feel it: be aware of the bias..others feel it as well but are unaware.

Ivo

Attached Image (click to enlarge)

Trouble lies in what we believe to know for sure that just ain't so.

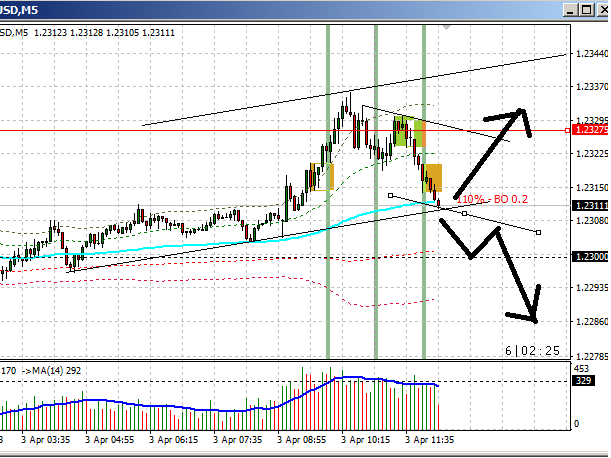

Looked promising but volume dropped of...and we're in a low volume downchannel that could last for hours..

Will it bounce of the VWAP? Maybe.. but I don't expect anything substantial until after the news. As long as we're in this channel the trend is down. Short on the FBO's.

Ivo

Attached Image (click to enlarge)

Trouble lies in what we believe to know for sure that just ain't so.