Rolling Over to the Immediate Practical Future

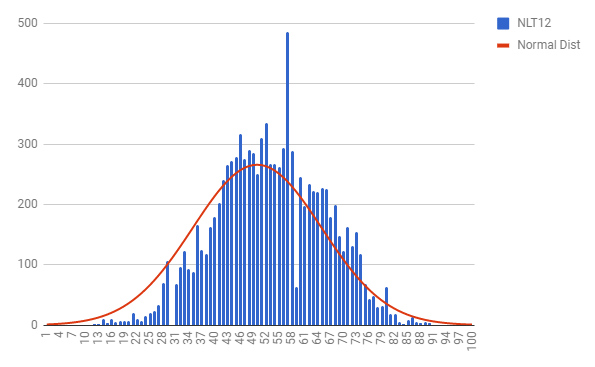

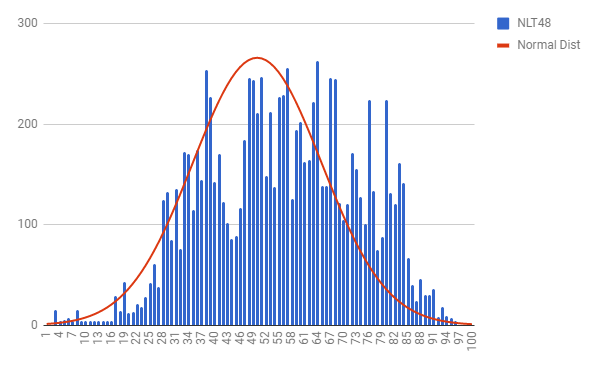

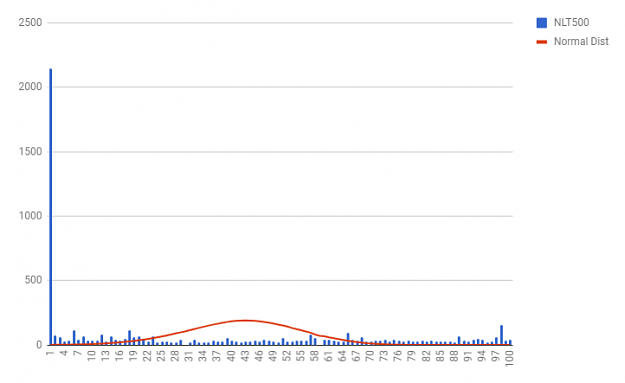

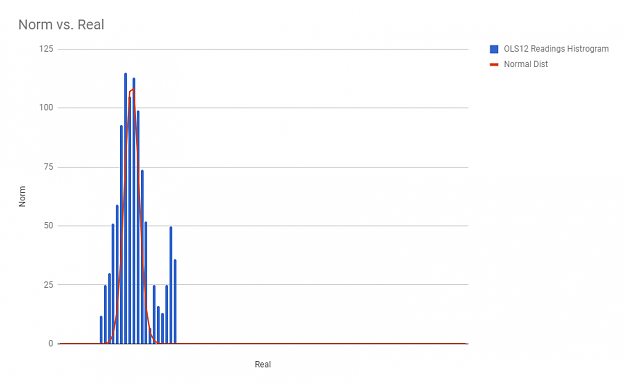

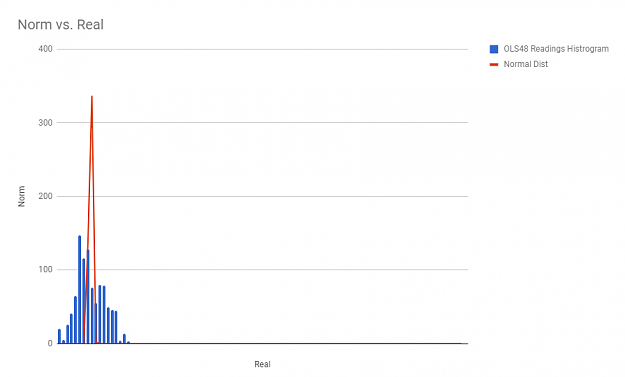

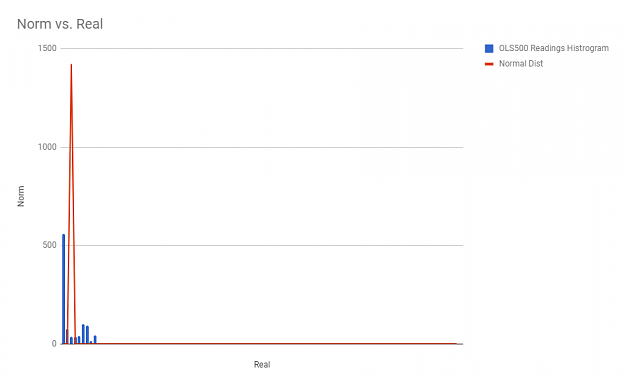

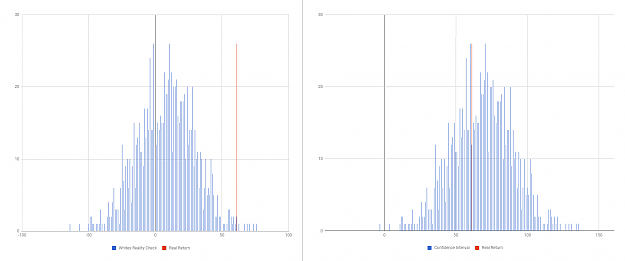

-- This first section is more of a small update. The first image will be referred back to during the main part of this post. --

You know it's going to be a good weekend when it starts like this:

Going to spend a lot of time this weekend studying some data mining bias stuff and working with a few of my systems.

Specifically will be working with Walk Forward Analysis in search of 2 things.

1. To see how well the frequency distribution data gathered in sample, dictates the out of sample behavior of the market.

2. To see how often the frequency distribution data gathered in sample is overstated or understated.

I always like recommending books, and for those looking to learn a lot about really taking a deep dive into technical analysis, I'd check out the book below.

I first heard of the book from Relativity and I can honestly say it's worth getting. I always find myself flipping back through it when I am testing new ideas.

-- Main Idea of Post Below --

I also have a new book coming this weekend that is about finite and infinite games... Sounds awesome I know, and even though it has nothing to do with markets, randomness, etc, I have a feeling it will give me a lot of new ideas that are applicable to the market.

One idea in particular I have been really milling over in my head is looking at rolling over trades to new X Axis Stops in order to extend a "finite" round a little longer. The reasons I am looking to do this is so I can find the optimal time to add into positions and push existing positions as far as they will go.

There are really two ways of going about rolling a trade into a newer A Axis stop that is further away:

1. Roll into a higher time frame move by using multi timeframes - This is what is usually talked about. I will look into this second.

2. Roll into a new "window" on the same time frame. - This is what I am really interested in.

The reason I am very interested in #2 is this. When rolling into higher time frames to extend duration, you are extending your volatility risk (when I say this, I mean the range of expected moves. Example: 1hour ADR vs 1D ADR, if you stop was 1ADR and you rolled into a 1D ADR trade, you would need to widen your stop to fit this higher time frame along with your target if you are looking to get the expected results of the Daily Data. I hope this makes sense.). Yes you are rolling into a higher time frame chart so your target will really widen up, however your stop will also widen quite a bit (often more than double, at least with my system), even when you are still riding the main direction of the market.

If you roll into a new "window" on the same time frame, you are still rolling with main direction, your duration gets extended, your volatility risk stays the same (take the above example, your ADR doesn't change even though the trade has "rolled over" so to speak), your targets expand because your lower bound ADR would be lower due to the drift, and your stops would shrink because the upper bound ADR would be lower due to the drift.

I am thinking these rolling periods will be great ways to milk existing trades, and add into new trades.

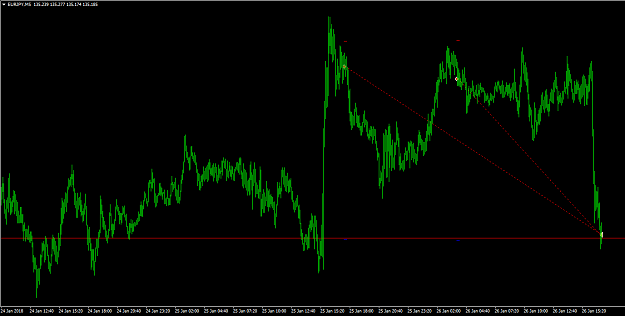

This is kind of what I did with the EURJPY trade I posted.

For example, when I first entered I was risking 30 Pips to make 80. To make things simple, lets assume for each position 1 pip = $1.00

Around the second entry, I rolled over the first trade into a new "window". Adjusting my existing stop and target changed my risk so I was now risking, 11 pips to make 80. I then add after the roll over, and on this added leg I am risking 20 pips to make about 70.

So because I rolled the trade to a new "window" on the same time frame, instead of to a higher time frame. I was able still trade with the same probabilities I was using when I put on the first position, except now I am risking 30 pips or $30.00 ($11.00 on the first position, $20.00 on the second) to make roughly 150 pips or $150.00($80 on the first position, $70 on the second).

By "rolling" we can double reward while keeping our risk the same.

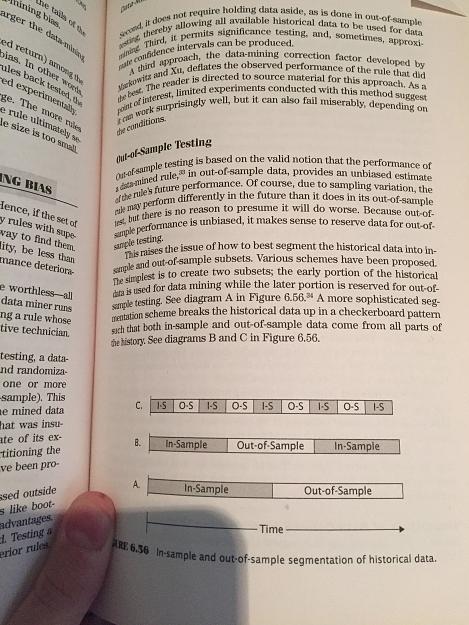

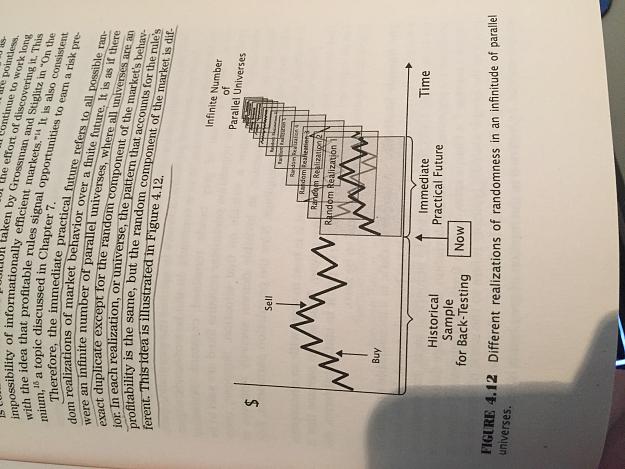

To best describe this kind of "window" I am talking about, I will refer to another image in the book I posted above.

It's essentially continuing to roll into the immediate practical future in order to maximize profit potential and reduce risk. Trading like this can often feel counter-diminutive because humans are programmed to optimize the chance of gain, over the potential of the gain.

Example: Say the initial probabilities we are trading with are 60%, so when we enter the first trade, we have a 60% of winning 80 pips and a 40% chance of losing 30.

Before we roll into the second trade, the probabilities of the first trade being a winner are higher than 60% because price is closer to our first target.

After we roll our trade into the immediate practical future, the probabilities for our net position go back to 60/40 only now we are risking 30 pips for 150. So we actually deoptimized the chance of gain (which is what humans, by default, do not like to do) in order to optimize our potential gain (which is also what humans, by default, do not like to do).

NOTE: It is important to verify your "windows" are independent from one another, and if they are not, you can use the calculation from the "A Correlation Problem" post to figure out what your new odds would be after rolling.

-- This first section is more of a small update. The first image will be referred back to during the main part of this post. --

You know it's going to be a good weekend when it starts like this:

Attached Image (click to enlarge)

Going to spend a lot of time this weekend studying some data mining bias stuff and working with a few of my systems.

Specifically will be working with Walk Forward Analysis in search of 2 things.

1. To see how well the frequency distribution data gathered in sample, dictates the out of sample behavior of the market.

2. To see how often the frequency distribution data gathered in sample is overstated or understated.

Attached Image (click to enlarge)

I always like recommending books, and for those looking to learn a lot about really taking a deep dive into technical analysis, I'd check out the book below.

Attached Image (click to enlarge)

I first heard of the book from Relativity and I can honestly say it's worth getting. I always find myself flipping back through it when I am testing new ideas.

-- Main Idea of Post Below --

I also have a new book coming this weekend that is about finite and infinite games... Sounds awesome I know, and even though it has nothing to do with markets, randomness, etc, I have a feeling it will give me a lot of new ideas that are applicable to the market.

One idea in particular I have been really milling over in my head is looking at rolling over trades to new X Axis Stops in order to extend a "finite" round a little longer. The reasons I am looking to do this is so I can find the optimal time to add into positions and push existing positions as far as they will go.

There are really two ways of going about rolling a trade into a newer A Axis stop that is further away:

1. Roll into a higher time frame move by using multi timeframes - This is what is usually talked about. I will look into this second.

2. Roll into a new "window" on the same time frame. - This is what I am really interested in.

The reason I am very interested in #2 is this. When rolling into higher time frames to extend duration, you are extending your volatility risk (when I say this, I mean the range of expected moves. Example: 1hour ADR vs 1D ADR, if you stop was 1ADR and you rolled into a 1D ADR trade, you would need to widen your stop to fit this higher time frame along with your target if you are looking to get the expected results of the Daily Data. I hope this makes sense.). Yes you are rolling into a higher time frame chart so your target will really widen up, however your stop will also widen quite a bit (often more than double, at least with my system), even when you are still riding the main direction of the market.

If you roll into a new "window" on the same time frame, you are still rolling with main direction, your duration gets extended, your volatility risk stays the same (take the above example, your ADR doesn't change even though the trade has "rolled over" so to speak), your targets expand because your lower bound ADR would be lower due to the drift, and your stops would shrink because the upper bound ADR would be lower due to the drift.

I am thinking these rolling periods will be great ways to milk existing trades, and add into new trades.

This is kind of what I did with the EURJPY trade I posted.

For example, when I first entered I was risking 30 Pips to make 80. To make things simple, lets assume for each position 1 pip = $1.00

Around the second entry, I rolled over the first trade into a new "window". Adjusting my existing stop and target changed my risk so I was now risking, 11 pips to make 80. I then add after the roll over, and on this added leg I am risking 20 pips to make about 70.

So because I rolled the trade to a new "window" on the same time frame, instead of to a higher time frame. I was able still trade with the same probabilities I was using when I put on the first position, except now I am risking 30 pips or $30.00 ($11.00 on the first position, $20.00 on the second) to make roughly 150 pips or $150.00($80 on the first position, $70 on the second).

By "rolling" we can double reward while keeping our risk the same.

To best describe this kind of "window" I am talking about, I will refer to another image in the book I posted above.

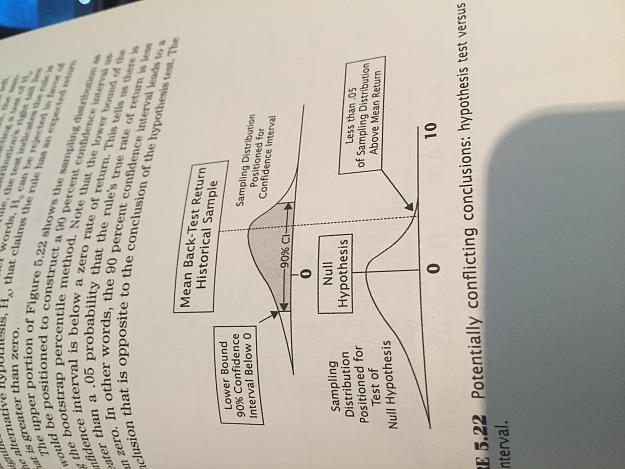

Attached Image (click to enlarge)

It's essentially continuing to roll into the immediate practical future in order to maximize profit potential and reduce risk. Trading like this can often feel counter-diminutive because humans are programmed to optimize the chance of gain, over the potential of the gain.

Example: Say the initial probabilities we are trading with are 60%, so when we enter the first trade, we have a 60% of winning 80 pips and a 40% chance of losing 30.

Before we roll into the second trade, the probabilities of the first trade being a winner are higher than 60% because price is closer to our first target.

After we roll our trade into the immediate practical future, the probabilities for our net position go back to 60/40 only now we are risking 30 pips for 150. So we actually deoptimized the chance of gain (which is what humans, by default, do not like to do) in order to optimize our potential gain (which is also what humans, by default, do not like to do).

NOTE: It is important to verify your "windows" are independent from one another, and if they are not, you can use the calculation from the "A Correlation Problem" post to figure out what your new odds would be after rolling.

5