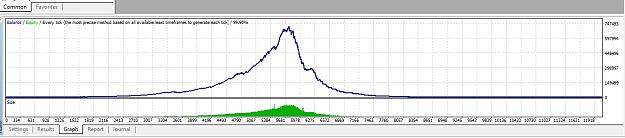

see attached back test using data from mt4 strategy tester and when i used tick data to carry out back test for 99% modeling quality.

the result were opposites.

tested EURUSD.

i also tested usdjpy, Gbpusd, i used defualt settings, and also changed my stop loss to 10. i used signal settings 6, and also 8

none of the results were good for any year between 2010- 2017.

using normal data from mt4, the results were excellent. but when you backtest using 99% modelling quality then result is not good.

used stating capital $500, and risk settings 3% also tried 1%

the result were opposites.

tested EURUSD.

i also tested usdjpy, Gbpusd, i used defualt settings, and also changed my stop loss to 10. i used signal settings 6, and also 8

none of the results were good for any year between 2010- 2017.

using normal data from mt4, the results were excellent. but when you backtest using 99% modelling quality then result is not good.

used stating capital $500, and risk settings 3% also tried 1%

Attached Image(s) (click to enlarge)