Sell In May & Play It Safe?

We are not usually pessimists but when we see the writing on the wall getting bold redder each week that passes, we can't help but to take serious note.

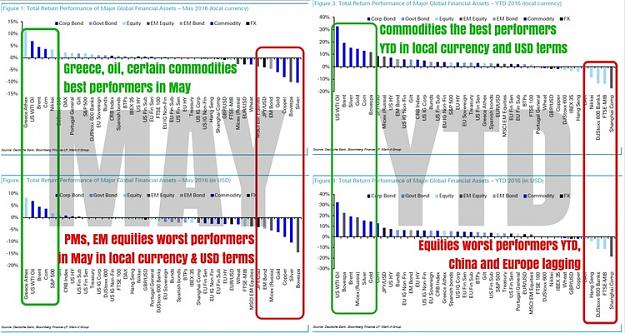

Just last week, we warned readers that markets might be about to get nastily volatile during the summer. So far so bad. May hasn't started well at all. The S&P 500, as of the week ending this past Friday, posted its first 3-week losing streak since January. The VIX has finally gone above 15, and the U.S. dollar index has been breaking the chain of shorts in the past 2 weeks, wiping out many bears in the process.

As portfolio managers, we have been flipping from short to long repeatedly in 2016. The environment remains markedly difficult to navigate and although the markets are aware of the many known unknowns, the sheer diversity and quantity of these unknowns have led to nervousness in the markets, and that has been reflected in abnormally non-directional price action in various asset classes. Volatility is a given.

READ MORE:

http://www.businessoffinance.com/ins...d-play-it-safe

"Is the Fed right to say that markets have misjudged its ability to raise interest rates both higher and quicker than expected? Well, the markets say the Fed is wrong on that. The gap between the market implied FF rate and that implied by the FOMC's "dot plot" is widening. For instance, the dots say FOMC officials see on average 2 more rate hikes this year while the market only expects 1. This discrepancy only widens the farther out we go.

Also, stocks have deviated far away from GDP growth expectations, likely because the transmission that are interest rates and monetary policy have become so broken, the market refuses to trade on fundamentals and are rather technical driven.

Lastly, whatever happened in March threw the balance between yields, stocks, and macro data totally off. All 3 have been divergent since and only one will ultimately be proven correct. So which is it?"

We are not usually pessimists but when we see the writing on the wall getting bold redder each week that passes, we can't help but to take serious note.

Just last week, we warned readers that markets might be about to get nastily volatile during the summer. So far so bad. May hasn't started well at all. The S&P 500, as of the week ending this past Friday, posted its first 3-week losing streak since January. The VIX has finally gone above 15, and the U.S. dollar index has been breaking the chain of shorts in the past 2 weeks, wiping out many bears in the process.

As portfolio managers, we have been flipping from short to long repeatedly in 2016. The environment remains markedly difficult to navigate and although the markets are aware of the many known unknowns, the sheer diversity and quantity of these unknowns have led to nervousness in the markets, and that has been reflected in abnormally non-directional price action in various asset classes. Volatility is a given.

READ MORE:

http://www.businessoffinance.com/ins...d-play-it-safe

"Is the Fed right to say that markets have misjudged its ability to raise interest rates both higher and quicker than expected? Well, the markets say the Fed is wrong on that. The gap between the market implied FF rate and that implied by the FOMC's "dot plot" is widening. For instance, the dots say FOMC officials see on average 2 more rate hikes this year while the market only expects 1. This discrepancy only widens the farther out we go.

Also, stocks have deviated far away from GDP growth expectations, likely because the transmission that are interest rates and monetary policy have become so broken, the market refuses to trade on fundamentals and are rather technical driven.

Lastly, whatever happened in March threw the balance between yields, stocks, and macro data totally off. All 3 have been divergent since and only one will ultimately be proven correct. So which is it?"

Attached Image (click to enlarge)