|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

May Interim Performance Summary - Discretionary Systems - Breakout Techniques (DTT, EDTT, EDTT1)

A very slow start for May. In relation to the portfolio of instruments and the breakout techniques used in the discretionary methods described in this thread it has been "All Quiet on the Western Front".

Despite the lackluster month, it is times like these that in my opinion sorts out the risk managers from the risk takers and ultimately defines the overall sustainability of your approach. During these periods it pays to keep the powder dry and focus on capital preservation. This is where a discretionary trader can outperform a fully automated system, not in terms of achieving refined entries or exits as some may think....but rather in having the flexibility to reduce trade frequency and avoid over-trading. It is all about reducing the propensity to over-trade and protecting capital during directionless market periods.

Anyway, before I blarb on too much.....the interim reporting for the month.

Inserted Video

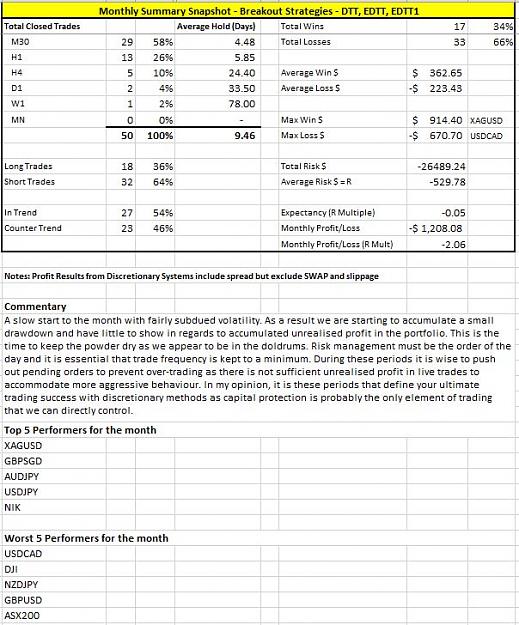

Statistical Summary of Closed Positions for the period 1 May 2016 to 14 May 2016

Attached Image (click to enlarge)

Top Closed Trade so far for the Month

Attached Image (click to enlarge)

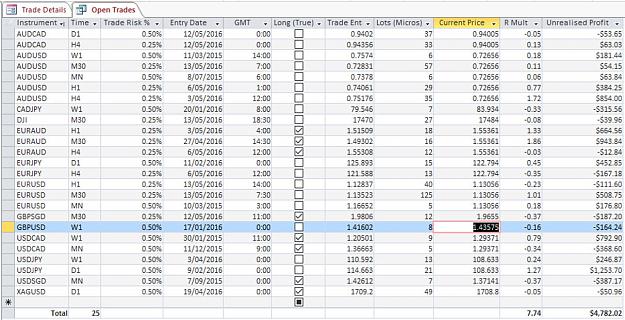

Current Open Positions

Attached Image (click to enlarge)

What's Trending at the Moment According to this Technique?

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)

That's it for the breakout discretionary systems. Full details are contained in the attached spreadsheet.

My next post will feature the interim results of the Discretionary Retracement Entry approach (DTTR)

|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

May Interim Performance Summary - Discretionary Systems - Retracement Entry Techniques (DTTR)

Below are the interim results for the recent entry into the discretionary systems currently being trialled. If results prove to be sufficient over a sufficient data sample, then both the breakout and retracement approaches will be consolidated under a single portfolio umbrella.

Inserted Video

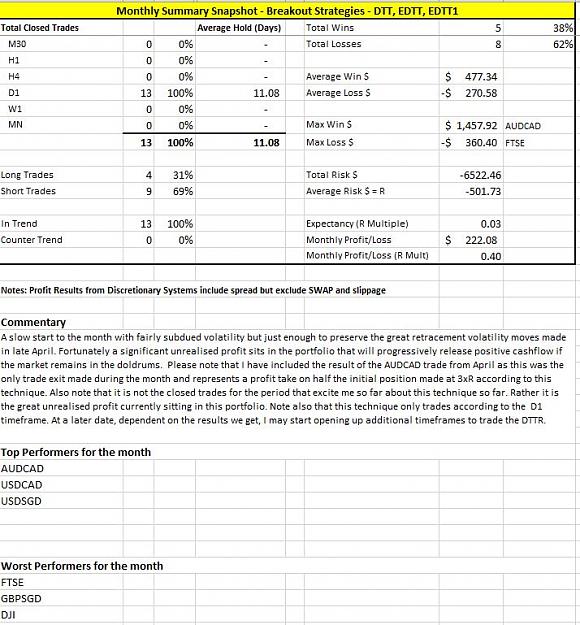

Statistical Summary of Closed Positions for the period 1 May 2016 to 14 May 2016

Attached Image (click to enlarge)

Top Trade so far for the Month

Attached Image (click to enlarge)

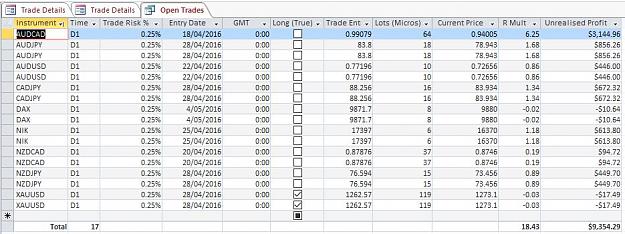

Current Open Positions

Attached Image (click to enlarge)

What's Trending at the Moment According to this Technique?

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)

Attached Image (click to enlarge)

A lackluster week. Let's hope directional volatility is just around the corner :-)

|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

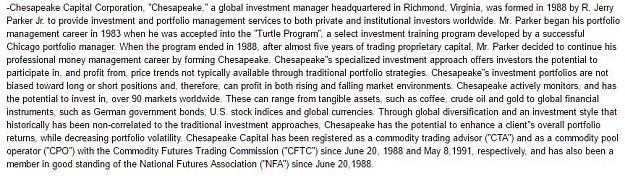

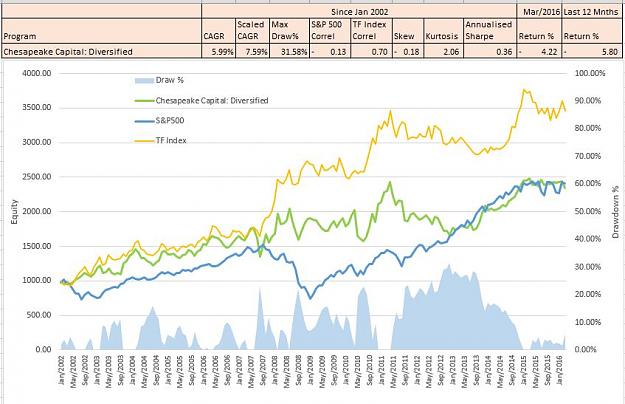

Weekend Ruminations - What is Trend Following and why is it a Divergent Risk Taking Approach?

Below is a summarised transcript from Kathryn Kaminski (Chesapeake Capital) speaking with Neils Kaastrup-Larsen from Top Traders Unplugged Episode 041

Chesapeake Summary

Attached Image (click to enlarge)

Chesapeake Capital Performance since 2002

Attached Image (click to enlarge)

Summarised Extracts from Transcript

Trend following strategies, and the concept of trend following is about creating a simple set of rules - a simple heuristic for how do you actually profit from moves - up or down? If they exist, how do you handle them?

Katy: ...... the beginning of our book starts with an 800 years analysis. That data... you have to think of it as an abstraction. Imagine that 200 years ago that you're sitting there, looking at prices for rice, or lean hogs, there's clearly maybe dealers that are selling these particular prices, so you have to abstract that the historical record that we have of those prices represents an aggregate view of how those markets behaved over history. If you see it that way, then you take this abstraction with the idea that, "what if I was the type of person that just said, if I see things that are going up in the last 12 months, I buy. If I see things are going down, I sell if I can." Do that simple thought analysis, not complicated rules, but basically just looking at history - 12 months buy, or sell. You do that over history, equal weighted, and then we examine how that performs, and the performance is relatively stable. Intuitive to me was what you see with modern day trend following, but modern day trend following is obviously much more sophisticated, but the concept is exactly the same.

Niels: Yeah. .. am I right in saying that you found, actually, some quotes from some, I don't know what it was, was it a politician or something like that who actually used words that I think we use now-a-days in describing trend following?

Katy: Yes. This quote is from David Ricardo, who was a legendary political economist, and this is sourced from a book called The Great Metropolis, in 1838. He said, "cut short your losses, and let your profits run on."

Niels: Sounds very familiar doesn't it?

Katy: It's almost 200 years old, but it's the same concept.

Neils: So tell us why you coined the 'The Search for Crisis Alpha' and where it came from?

Katy: .....where this original paper came from to give some contextual reference for that....... I was in a meeting with Hans Fahlin, who's the CIO of AP2, and Hans turned to me and said, "I don't understand. Tell me why does this (trend following) work during this period of time?" I stepped back... everybody knew that trend following tends to do well during a crisis period and I just was so irritated that I couldn't answer that question that I actually thought about it for some period of time and I went back and did some analysis and did some research and I said, "my goodness, this is pretty incredible, on certain days, when things are really bad for equity (and I'll get back to the other markets in a second) things are... something is happening." It's not just happening in equities. Most of it is happening outside of equities, and it's not just happening in commodities, it can happen in rates, or FX, or here, or there. I started looking at these days where there's these big moves in equities and I found that (and this is going to be a geeky point) .....the cumulative distribution of these particular days is actually before the distribution of the days outside......I will use an example to try and explain what this means.

.. imagine I'm trying to explain this to one of my MBA students. So if I take the days where equity markets go down, and I look at a simulated trend following system, and I take something which is called the cumulative distribution function. So how that works is you think of it as building. When you build a cumulative distribution function, it's as if you take the values and put them into a bag, and so you start collecting them. So if something has a big fat tail, you're going to see a lot of mass on the left side, and then it's going to grow up less slowly. So what you can do, actually... one particular statistical test you can do is you can look at if one dominates the other. What that means is that the cumulative distribution is farther to the left... the one that dominates to the right, and then you have another to the left. So if you have two distributions: one that is to the right of the other, completely. Then it's considered first order domination.

If you take stocks and bonds, this relationship doesn't hold, because they cross and why is this the case? It's because stocks have fat tails, which means that they end up collecting more of these worse scenarios first before bonds, but then they have much better performance latter, so their distributions actually cross. So it makes sort of a loop. But when I looked at trend following returns in a certain... some of the daily analysis that I looked at, based on a sort of a filtering rule that I use, I could find periods where there was first order stochastic dominance and I have basically never seen or very rarely seen that in financial data.

I said, "there's something here that's just different." So I thought, OK, these particular moments... something is happening where these strategies are adapting to the scenario of sort of a crisis scenario in a way that is not expected. Then if you go back and you think about the Efficient Markets Hypothesis, futures markets should be so competitive that you can't make money, right, because they're obviously the most liquid, sort of the most efficient. Then I thought, wait a minute, maybe it's actually the case that they're a little bit like Buffet, that they're liquid when others are not, so the fact that they are so liquid and adaptable and in futures is what gives them an advantage over the others in these scenarios. That's where I said, OK, so what are they getting at this period of time when things are sort of a mess? Well, they're getting alpha, because they're finding opportunities that are up and beyond the sort of normal risk measures.

So, I said, ah ha! Now I have a buzz word, it's "crisis alpha". The content of crisis alpha came out of that entire story. It originated from a question that someone asked me that I couldn't answer, and then I went back and did a research report on it, which I actually have never published but then I wrote a short article for the CME group to compliment this research paper, which was meant to sort of be for the entire industry, and that was the original paper which was meant to be for the entire industry, and that was the original paper which is called A Short Guide to Investing in Managed Futures: in Search of Crisis Alpha a Short Guide to Investing in Managed Futures, that was in 2011.

So now going back to your point about bonds and commodities. That's something that really bothered me as well, because I kept getting that question all the time. So in the book we talked about crisis alpha for commodity indices. We talked about bond crisis alpha. We talk about commodity crisis alpha, but over the course of writing this book I actually had moved more towards a new idea, and this is the idea of divergence.

Katy: What we do in the book is we explain that trend following strategies are long divergence. What that means is that the most divergent moment in history is always crisis, wherever it comes from. Yeah, so crisis alpha is part of that. That's extreme divergence. The story is a little bit more clear to me now that it's really about being long divergence in markets, and divergence can be driven by many things.

.....so if you step back for a second and you think about risk as a concept, risk is really sort of what we face every day in every aspect of our life. It's sort of a dynamic process. How we handle risk depends on both what our frame of reference is as an individual, our experiences over the past, and also our beliefs. So if we think about that, those three things come together to give us an idea about which type of strategy we're going to use, in any risk situation, whether it's personal or financial.

Convergent risk taking strategies are used when we believe that the world is somewhat stable, knowable, and understandable, and quantifiable. Many, many risks in life actually are somewhat convergent, or quantifiable. When we believe that the world is like that, then we tend to apply one set of strategies, convergent risk-taking strategies.

.....So if you're a convergent risk taker, you have a particular view. Let's say that you view that equity markets are going to go up, as an example. If equity markets go up, you tend to take profit on that. When they go down, you'll tend to do the opposite. You'll say, wait a minute, I know that equity markets go up over the long run, this looks like a buy opportunity. I should actually double my bet, or at least hold my bet and not sell it. So in that sense, over time, when you're convergent, when you win it reaffirms to you what you believed. When you lose, it actually goes against your fundamental belief structure which is sort of a threat in some sense, causing you, in some sense, to often reaffirm your beliefs.

Now divergent is the opposite. If you imagine a scenario where you have no idea if A, B, or C is going to do better than the others, what you'll do is you'll invest, or put a small amount of investment in each of them, and if one of them starts to do well, you'll say, hmm, this could be it, I don't know, but A could be the one. So you'll double your bet on the thing that's going well. Every time you lose you don't have any prior expectations about a particular position or particular view, so you'll cut your losses.

So those two philosophical views (convergent and divergent) are very different. For those of you who know... you yourself being a trend following manager, you know that trend following managers, in general are divergent. When they're asked what their view is about the dollar, they may give a view, but they don't... they would change their view as soon as their indicators said something else. Global macro investors are not the same. Same with value investors, they believe in the value of a particular company. It really depends whether they work - if the world is actually governed by risk or uncertainty.

Neils: So can you explain the relationship between these different philosophies and the Adaptive Market Hypothesis

Katy: Starting in around 2004, professor Andrew Lo, from MIT, put forth the idea of the Adaptive Markets Hypothesis. This hypothesis is an alternative and a complement to both the world of behavioral finance, which is really a world of psychology, and the world of efficient markets, which is more sort of a physics view of the world, where you see F=MA. If you look on a spectrum, psychology and physics are very, very far apart. What Andrew brought forth, which is a really fascinating way to think about it is that markets are much more like evolutionary biology - somewhere inbetween, where the psychologist have some things to say, and the physics matters too. So if I want to give you a definition of the Adaptive Markets Hypothesis, it's an approach to understanding how markets evolve, how opportunities occur and how market players succeed or fail based on the principles of evolutionary biology. So the concept in that, based on Andrew's work, is to see the market as an ecology and to understand who succeeds and fails based on those principles. So competition will drive who succeeds; resources which are available will drive profits; and the evolution of our industry is a function of the players that are involved in the industry and the resources that are currently available. So you asked me to connect convergent and divergent. Well, what that means is that, depending on the environment, at some periods of time convergent makes sense. At some periods of time divergent, but if you want to be adaptable over a long horizon and survive, you need to be both following the herd and convergent, but you also need to be divergent so that you can innovate, adapt and sort of be more robust in times when markets are changing drastically.

Niels: Of course divergence and volatility is somewhat related, but it's not the same thing.

Katy: Yes, divergence and volatility are correlated. They're positively correlated maybe at 20%. The reason is that... I was just giving a talk about this recently for the CME, and what I said was that if you have low volatility, you tend to have low divergence, but if you have high non-directional volatility, so that means where things are going up and down, and up and down, but they're not really going anywhere. This is actually a nightmare for a divergent trend following strategy, so there's no divergence in that. It's actually low divergent. But if you have high directional volatility, then you have high divergence. So divergence is more if you take... it's basically the amount of discernable trend in price. So if you take this, sort of over an horizon and you divide the amount of movements, you're actually taking the volatility out. So if you have lots of volatility, the divergence is really the signal to noise ratio in prices. So when there's lots of volatility there's lots of noise, and therefore divergence is not very high.

|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

What's closing into the Kill Zone

A couple of potential mean reverting opportunities back into trend on D1. I wait for confirmation entry once mean reversion has commenced into the orange zone and touches/crosses the 75% SDC channel.

|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

What has Evolutionary Biology got to do with Trend Following?

As you peruse the popular posts of this forum, you inevitably have the banter between those who treat this game as a lucrative venture offering the chance to live the life of dreams versus those that adopt the spectral opposite and suggest that this is a negative sum game for the gamblers out there.

Is there a middle ground between these diametrically opposed viewpoints?

What this post seeks to explore is a middle ground between the notion of 'efficient markets' or what others may view as 'predictive markets' by exploring a concept referred to as 'Adaptive Markets'.

For evolutionary biologists out there, the ideas surrounding a stable ecology occasionally punctuated by 'shocks' or disequilibrium events is an accepted viewpoint that recognise that complex systems (ecologies) can exhibit prolonged periods of equilbrium where systems appear very stable but occasionally due to the intricate set of relationships that exist within complex systems, a seemingly insignificant and unpredictable failure in a critical element of that network of relationships can result in a cascading failure that ultimately translates into an avalanche of disequilibrium for a period of time, until a new equilibrium is achieved when a new set of relationships is established that restores the system into a 'quasi steady state'.

Let's then apply this concept to the markets.

Let's assume that the market (and for the sake of this discussion let's assume this relates to any liquid market as no single asset class stands alone as all are interconnected) is efficient 'most' of the time and let's assume that this representation of the market is when orderly markets reign that appear predictable in nature.

What are some of the symptoms that a retail trader would face under these conditions where markets are stable and efficient?

During orderly market conditions when volatility is within 'normal' limits, the markets are incredibly efficient, but also due to the relatively stable regime, quite 'predictive' in that repeatable patterns of price behaviour exist by virtue of the market's stable nature. The multiplicity of participants and their various strategies make it exceedingly difficult to extract a sustained edge in the market while these conditions exist. Competition for alpha is extreme and during orderly times, price action exhibits repetitive features that a nimble trader/ discretionary trader and pattern recognition algorithm can quickly adapt to. Within these 'orderly markets' noise is a common characteristic. When referring to noise, we refer to the notion of 'unpredictability'.

The noise is a manifestation of the multitude of trading activities undertaken in this efficient market, but it must be noted that noise is a 'relative' concept. What I mean by this is that what is noise to a particular trading style, may be 'alpha' to another trading style. The prevalence of noise however is a feature that the persistence of alpha for a particular trading style is ephemeral in nature and quickly evaporates.

Due to the intense competition for alpha in orderly markets, the potential for exploitation is very quickly removed as discretionary traders and pattern recognition algo's rush to exploit the 'new' opportunity. With the evaporation of a repeatable pattern, the composite mix of participant behaviour then creates a new ephemeral pattern ...and so on and so forth. Also during times of normal market conditions, the opportunity to identify when price exceeds it's normal volatility variation is able to be predicted with a degree of confidence enabling convergent strategies such as mean reversion strategies to shine during these periods.

A speculative retail trader (a very small part of the total participant mix) who identifies an exploitable repetitive pattern has a very small window of opportunity to capitalise on this opportunity while it exists. Markets are dynamic and respond to participant behaviour and within a short space of time the influx of participants who exploit this temporary opportunity find that their cumulative market impact actually removes this opportunity and it reappears elsewhere with another repeatable pattern.

So here are some of the symptoms that a retail trader may face during these 'quasi stable periods' :

They would find that the exploitable opportunity identified through back testing or forward testing over a short time interval (when those specific market conditions prevailed), would quickly evaporate, and after a short hiatus in the sun pf live trading, would no longer work....a familiar outcry on this forum.

They would scratch their head and perhaps declare that the markets were rigged.......another familiar outcry on this forum.

They may find that the short term magnificent returns upon which they projected their vast future wealth in Costa Rica evaporated leaving them a progressively greater drawdown until sanity prevailed and they pulled the pin on the strategy, hopefully before blowing up their accounts.

It is during these specific times (market regimes) that a convergent risk taker dominates the forum. They are the ones that:

State boldly that markets can be predicted;

That long term back-testing or demo testing is worthless as an endeavour and that true trading is about 'live trading';

That trader skills and discretionary trading beats the stuffing out of systematic trading;

That no EA's work as they are incapable of reading price action with the finesse achieved by a trained brain;

That reading price action is everything;

That accuracy of entry and setup are tantamount to trading success;

That trend following is dead and that if you really want to make the bucks you need to scalp predictive price action;

That mean reversion is safe as houses;

That Mingary is a bore and is just a failed trader with a gripe.........

.....do I need to go on.

And the reason that the numbers of convergent risk takers swell is that during this regime, their beliefs are reinforced until they become 'Lords of the Domain' with a legion of loyal supporters.

It is during these times that a divergent risk taker (also called the trend follower) keeps his powder dry and avoids overly committing their diversified portfolio to trades when alpha is scarce and highly competitive. Frequently those trend followers that find they over-commit during stable market conditions, endure progressively larger and larger drawdowns and if not careful run the risk of such significant drawdowns that they are unable to recover. Now this is 'why' the diversified trend follower back-tests over as many different market regimes as they can muster as it is imperative to scale your trades and trade frequency in such a way to 'keep your powder dry' and avoid these excessive drawdowns....as 800 years of history have told us that market regimes frequently change, and during these disruptive times, trend following makes it's return in spades to recover from these protracted drawdown periods during stable efficient markets.....so typically just when you start second guessing yourself and start to think like a convergent risk taker.............an innocuous 'something' happens to disrupt the apple-cart and bring chaos to the convergent risk taker.

The prevalence of these market regime shifts are much more frequent than you might think but are impossible to predict. So while stable market conditions might prevail most of the time, market transitions occur 'some' of the time, but enough of the time to allow diversified trend followers to outperform the competition. This is what gives the fat tails to the distribution of market returns. This frequency of occurrence of market regime shifts is the reason why convergent risk takers rarely can post an audited verified track record of more than a few years and why so many curve fit EA's get sent to the sin bin.

The regime shift itself disturbs the ecology (it's participants and network of relationships that have previously emerged) and the false sense of security that have been lulled into it's participants due to previous market stability. We get panic and system disruption as fight or flight pandemonium set's in. The bulk of convergent risk takers start acting like a herd scurrying for the exits and across asset classes, and on the other side of those trades lies the 'divergent risk taker' who is simply following price action and relying on extended directional price behaviour during these chaotic periods of disruption before the market achieves a new equilibrium where then the convergent risk taker starts to emerge from their bunkers ....to repeat the cycle again and again and again.

This is when the competition for alpha becomes far easier as the bulk of previous competition are heading for the exit gate, and this is when diversified trend followers start pillaging the horde. The availability of alpha during these periods is extreme due to the 'sudden' dramatic reduction in competition and a time when the lion's share of performance for the trend follower emerge which starts paying for their enduring patience and associated drawdown legacy. Think of ecologies that have had a major disruption (such as an asteroid strike) where the bulk of the competition is wiped out and the 'meek' robust species who survives rapidly exploits the uncontested environment.....well us trend followers are the meek that will inherit the earth. :-)

Now this disruptive feature is simply symptomatic of the dynamic nature of markets. Once an equilibrium is reached, a new network of relationships emerge that create inertia and 'stick' the market into it's stable enduring state...for a period of time at least....until that small flap of a butterfly wing occurs at a strategic weak spot that sends the market into short term pandemonium.

Now the thing about complexity is that as systems become more complex, the stability of the system reduces. Think of any large complex system (like the global economy) and think what a small disruption, such as a power outage for example brings with it)........ so the future of trend following is indeed bright particularly given the nature of global markets and their current 'manipulated nature' by government intervention and the onset of a flurry of HFT. The more complex the system becomes, the greater the propensity for cataclysmic disruption. The thing however about HFT, just like mean reversion or indeed any negatively skewed strategy is that when the collapse comes, it will be sublime......so keep on keeping on and don't lose the faith as sooner or later we will be 'bringing in the sheaves'.

What we are discussing here is simply evolution in action of a complex system....... and to be a survivor and have a track record in this market of more than a few years beyond a single market transition, you need to become a divergent risk taker. This however does not preclude the trend follower from dabbling with convergent systems provided it is a supplement as opposed to the main game of his/her strategy that is uncorrelated and assists in reducing drawdown impacts. This is the preferred way to deal with uncertainty and the reason for 'how' life has evolved on this planet. Not by design, but simply by being sufficiently robust to survive in a dynamic environment. To all those diversified trend followers out there......take a bow from Charles Darwin.

|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

While on the subject of rants.

Here is a rolled gold example from Covel that needs to be posted on some of this forum's threads about the need for a reality check and the inability to expect consistent returns.

{quote} Ive just had to evacuate anyone who was in my office due to unexceptable noise levels... What a great tune, I love this sort of vibe..I need bigger speakers ...lol.. And that's coming from someone who is in their late forties ...who said your only young once

Ignored

There definitely is a bit of modern jazz in you Ja. I thought it might tickle your fancy

Pffft....old age???....who's counting. We are simply ageing gracefully like any good wine should.

Weekend Ruminations - What is Trend Following and why is it a Divergent Risk Taking Approach? Below is a summarised transcript from Kathryn Kaminski (Chesapeake Capital) speaking with Neils Kaastrup-Larsen from Top Traders Unplugged Episode 041

Ignored

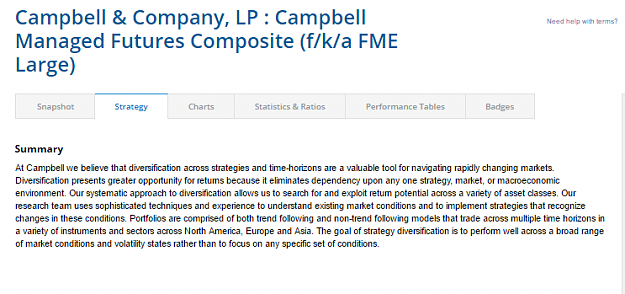

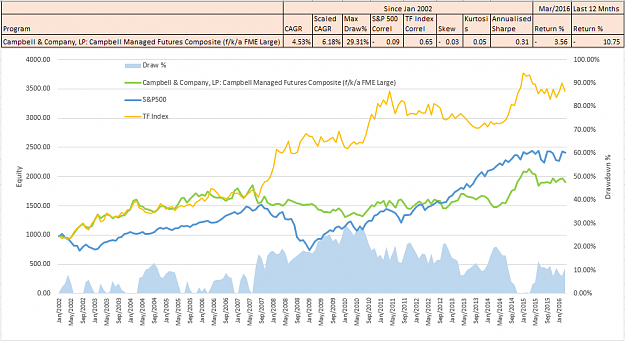

Apologies guys. A big stuff up in Post 964. Kathryn Kaminski is a Director at Campbell & Co and NOT Chesapeake Capital. Not sure how this oversight happened, but better correct it for the record. Obviously it's easy to confuse the names of Jerry Parker and Kathryn Kaminski. They sound so familiar.....NOT!!!!

Details of Campbell & Co are below to replace that given for Chesapeake.

|

Commercial Member

|

Joined Apr 2013

|4,366 Posts

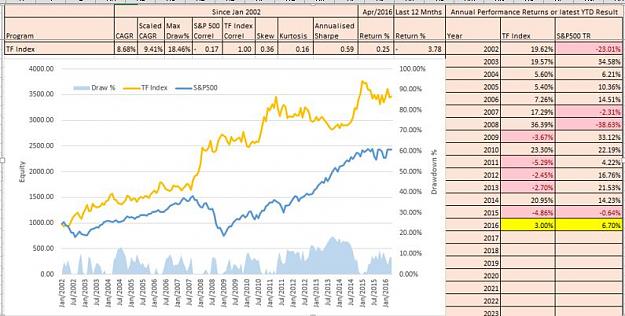

Trend Following Performance Report - April 2016

Following a harrowing March result that gave the trend following camp a solid kick in the guts, April fortunately stemmed the blood letting and produced a marginally positive month for the Trend Following Index (TF Index)....Nothing to get excited about but enough to reduce the pile of investor complaints sitting on the FM's desks.

The calendar year results for the period Jan 2016 to April 2016 is up 3.00% for the Index as a whole and is languishing behind the S&P500 TR Index.....that's right, you heard correctly.....despite the shellacking that the 'buy and hold' mutual camp get's from the trend followers, they are making us eat humble pie at the moment. But the year is still early and it's not over till the fat lady sings.

Inserted Video

Below are the results for the TF Index.

Attached Image (click to enlarge)

Despite the recent under-performance, nothing materially significant is popping up in the analysis to give cause for any concern. As trend followers, living under the shadow of a drawdown is just something we need to get used to if we are seeking those attractive long term returns. Since 2002, the TF Index has achieved a nice CAGR of 8.68% and a maximum drawdown of 18.5% (or approximately 2x the performance return). Overall the sector has delivered a positive skew which is part and parcel of a divergent strategy and the reason why the drawdowns for trend following are almost a permanent feature.

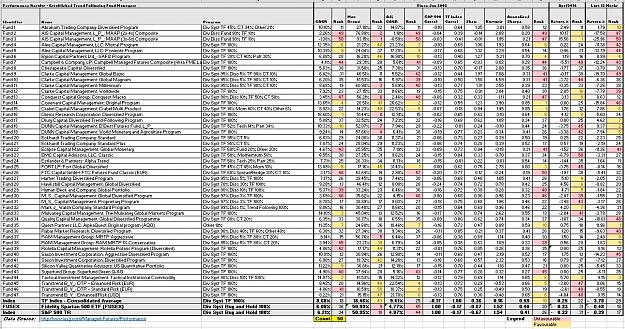

Anyway, below are the detailed results of the funds that comprise the TF Index.

Attached Image (click to enlarge)

April was a pretty mixed month for performance with some funds (that offered diversified strategies that included mean reversion and discretionary options) pulling in thee good returns. The traditional systematic trend following funds in general found it quite a difficult month however.

Note that Covenant Capital, Drury Capital, Rotella Capital, Silicon Valley and the Superfund Group have not posted results yet for the month of April......they are probably still responding to their investors from March's horrific results. Anyway, for these reporting laggards I have given them a big fat zero return for the month which might actually be doing them a favour.

So onto the awards for the Month of April for the FM's.

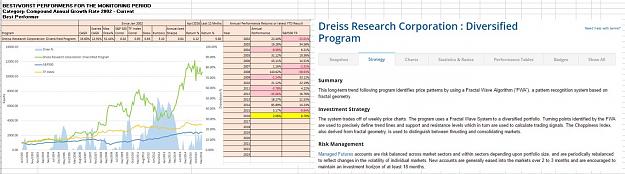

Adrenalin Junkie Award for the best CAGR between Jan 2002 to April 2016

Attached Image (click to enlarge)

You guessed it. Dreiss Research once again is maintaining it's lead over Tactical Investment Management, but the juggernaut is slowing down given most recent results and only boasts a 2% return for the calendar Year to date.

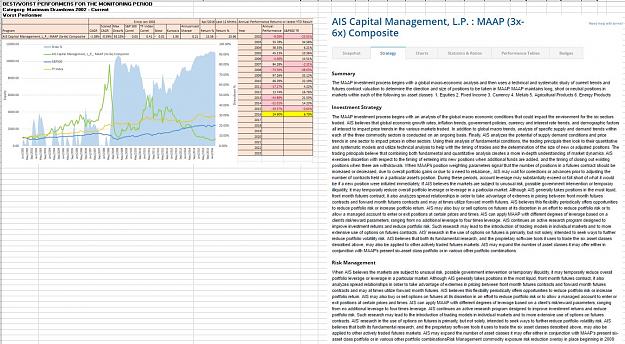

Wooden Spoon Award for the Worst Drawdown between Jan 2002 to April 2016

Attached Image (click to enlarge)

Yes folks, it's still alive. If you are really quiet you can still hear the heart beating........in fact, this nightmare on CTA street actually pulled a strong performance for April. There are no brakes with this fund. Investors with concerns are asked to contact AIS's Marketing Manager seen here (below).

Attached Image

White Undie Award for the Lowest Drawdown between Jan 2002 to April 2016

Attached Image (click to enlarge)

This is more my style.....but I am a risk management nazi. What this demonstrates is that if you seek returns of above 5% per annum you are going to have to live with drawdowns in excess of 10% over the long term.

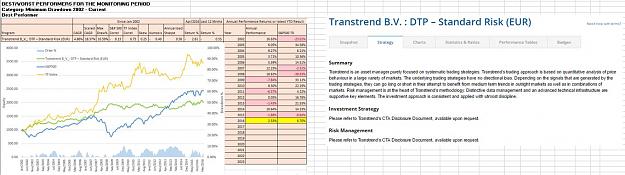

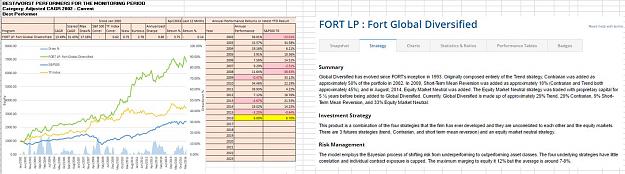

Bestest of the Best Overall Performer Award for the Highest Adjusted CAGR between Jan 2002 to March 2016

Attached Image (click to enlarge)

If you are after the best overall performer with respect to best performance return scaled to drawdown....then this is it...... The current investment god of the universe in the CTA space. Well done again FORT. Interestingly note how to accelerate performance returns FM's who have traditionally occupied the trend following space are now being forced to diversify into non-traditional trend following strategies such as mean reversion.

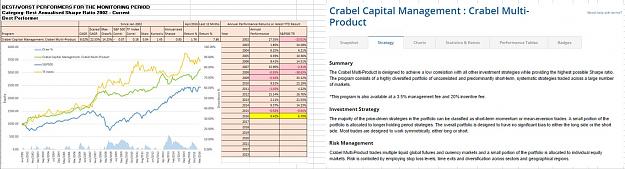

Encouragement Award for the Best Annualised Sharpe Ratio between Jan 2002 to April 2016

Attached Image (click to enlarge)

Not my preferred performance category (as I prefer adjusted CAGR), but the Sharpe ratio is still a fairly robust metric that displays overall volatility of returns. Note how the investment strategy specifically seeks to provide the highest possible Sharpe ratio....well, they have delivered on their promise so far.

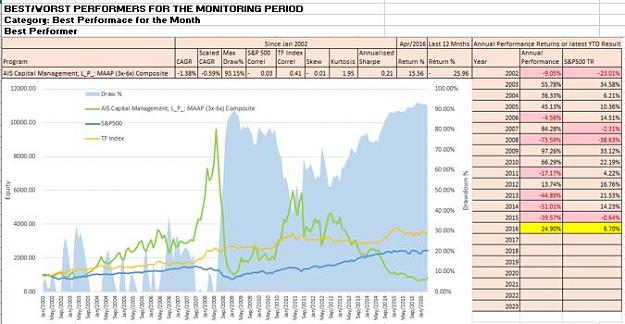

Brief Moment of Glory Award for the Best Performance for the Month

Attached Image (click to enlarge)

OMG......Who would have thunk it.....the black sheep of the group delivered the best result for the month. It's time to party.

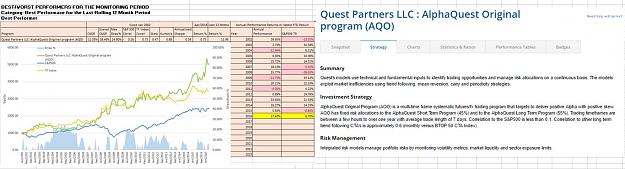

The Last But Not Least Award for the Best Performance over the last 12 rolling Months

Attached Image (click to enlarge)

It looks like Quest is on a Quest. Warp factor 6 Scotty.