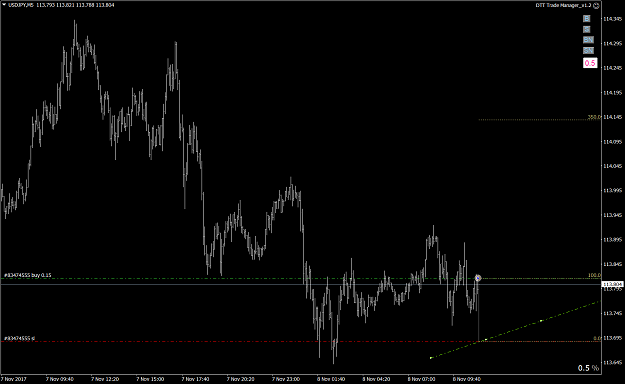

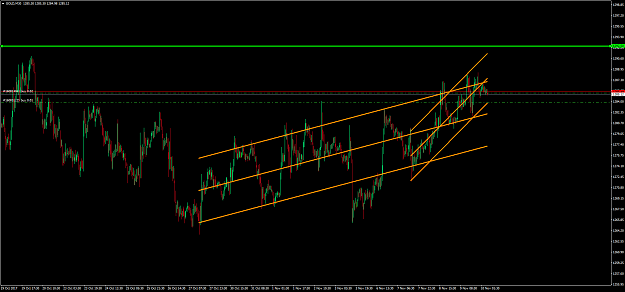

DislikedWhat I noticed on different markets in forward testing and now in GBP USD. Ranging markets are widened by less than half ADR at a time. Limit orders against breakouts (buying cheap, selling expensive) are waiting there, it seems. {image}Ignored

If we start a new system that trades ranging conditions between the boxes or pending orders of EDTT, it is not necessarily going to give us any correlation benefit with our EDTT. The reason for this is that the ranging system trades when the EDTT doesn't. It will generate it's own equity curve which may not necessarily give us any drawdown benefit to our primary system.

What we need to look for is a system that is 'switched on' and 'switched off' at the same time as EDTT yet is a mean reverter (or convergent system) as opposed to a divergent system (aka EDTT). When EDTT fails, the alternate system wins and vice versa. If both systems then can offer a slight positive edge then we have a dual system that suppresses the volatility of the combined equity curve.

If we simply trade within the range when the EDTT is switched off, then even if it has a positive edge, there may be times when the dual systems may compromise the great results of the EDTT in isolation dependent on the profile of the equity curve generated by the latter system compared with the equity curve of the EDTT.

So......let's assume we use the SDC for both systems and have the pending order entry set of divergent trades (like we are doing currently with EDTT) and convergent trades (eg. reverting back to the centre line of the SDC). The latter system will have a high win rate of say 65+ % (given that the EDTT win rate is approx 40%) but the Risk:Reward will be approx 2:1 or 3:1). We need to test it out....but it may produce the offset we need to reduce our drawdowns during the ugly non trending periods of mean reversion.

Sooner or later I will start testing a few options on our backtest model......but I don't have much available time at the moment.

2