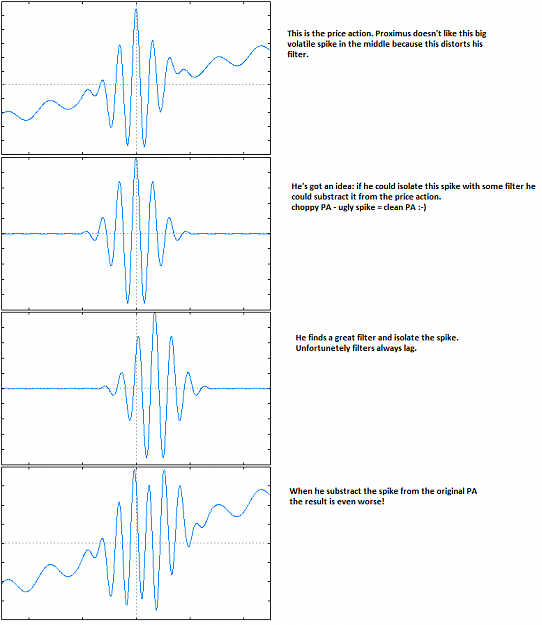

Ok this method stands so far, as i also introduced the filtering of the signal itself, to cutoff the small amplitudes which are only a noise, mostly we are talking about <2 pip noise, but it is still a noise and we dont want that.

I found that a filter like that can also cut off the price spikes and the minor fluctuations without causing unproportional lagg.It is proportionally useful to say like this.

Oh an also i will use the WINRATE as a metric too, so we will have 3 main metrics and 1 optional.

Why the winrate ? Well we got the expectancy so we really dont need the winrate, however the winrate plays the role when we are talking about consecutive losses. You see we only measured the intra-trade drawdown, but what if there are 4 consecutive losses, it is equivalent to 1 big intratrade DD, 4 smaller extra-trade DDs, yet they were not measured yet.

Although i dont measure directly the consecutive losses because that depends on luck, i could measure the maximum one, but it can also be derived from the winrate directly, so its ok to use only the winrate.

For example a winrate of 20%, will have a probability of 5 consecutive losses is about 96.875% under normally distributed trades (which normally are depending on the strategy) but roughly speaking we can assume it.

So obviously we want the highest Winrate possible to be able to use the highest lot size possible without assuming huge risk for the equity.

In case of a 20% winrate like above we need to have a very conservative lot size otherwise it would be a cowboy madness. Risk management is the first priority for any trader.

So my current GEN 2.6 FILTER HAS:

This is my HOLY GRAIL for the moment, I hope that my research will show me better ones later on.

I found that a filter like that can also cut off the price spikes and the minor fluctuations without causing unproportional lagg.It is proportionally useful to say like this.

Oh an also i will use the WINRATE as a metric too, so we will have 3 main metrics and 1 optional.

Why the winrate ? Well we got the expectancy so we really dont need the winrate, however the winrate plays the role when we are talking about consecutive losses. You see we only measured the intra-trade drawdown, but what if there are 4 consecutive losses, it is equivalent to 1 big intratrade DD, 4 smaller extra-trade DDs, yet they were not measured yet.

Although i dont measure directly the consecutive losses because that depends on luck, i could measure the maximum one, but it can also be derived from the winrate directly, so its ok to use only the winrate.

For example a winrate of 20%, will have a probability of 5 consecutive losses is about 96.875% under normally distributed trades (which normally are depending on the strategy) but roughly speaking we can assume it.

So obviously we want the highest Winrate possible to be able to use the highest lot size possible without assuming huge risk for the equity.

In case of a 20% winrate like above we need to have a very conservative lot size otherwise it would be a cowboy madness. Risk management is the first priority for any trader.

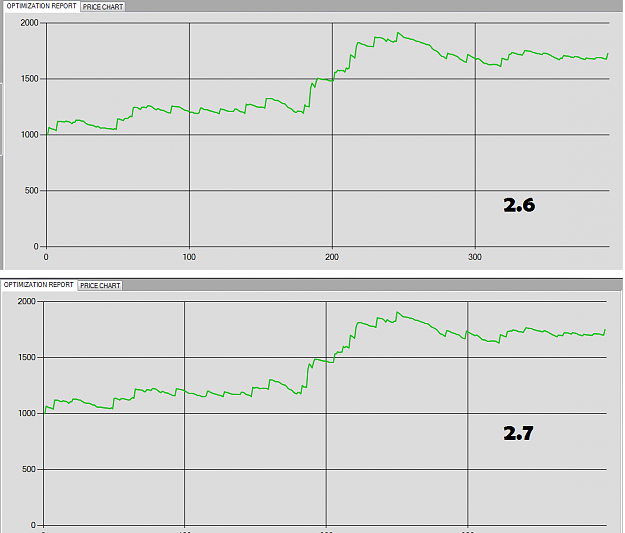

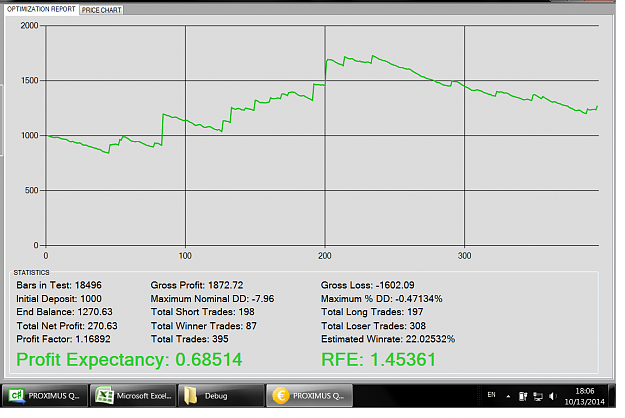

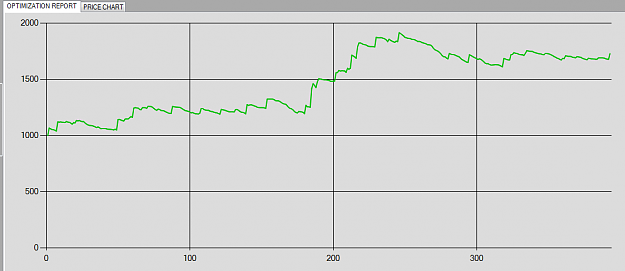

So my current GEN 2.6 FILTER HAS:

- 1.45 RFE

- 393 TRADES

- 22.3% WINRATE

- 1.47 PROFIT FACTOR

The equity curve looks like this:

Attached Image (click to enlarge)

This is my HOLY GRAIL for the moment, I hope that my research will show me better ones later on.

"There's a sucker born every minute" - P.T. Barnum