First results as a liquidity trader

Hello dear subscribers,

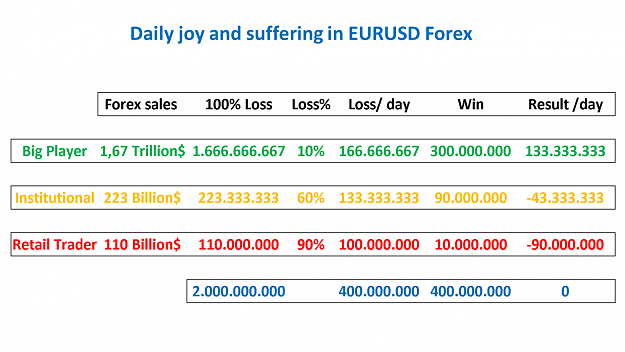

For almost a year now I have been dealing very extensively with the stock market data that I use exclusively for my trading in Forex. At first, like most future traders, I concentrated on the volume, but found that the big players primarily absorb the volume with their limit orders in order to collect the required number of bid and ask. The big players used the volume, in the form of market orders, only to keep the price within a range or to push the price in their direction in order to fill their limit orders with compressed volumes (stops of retail traders). In addition, they began to make massive amounts of liquidity and volume available to themselves when there was relatively little volume on the market. You can also find some posts about this in this blog.

Experiment own liquidity continues!

Overall, the decisive factor is in the area of limit orders, since most traders ignore them. For this reason, in the past few weeks I have concentrated exclusively on the decisive liquidity (limit orders) that come into the market unnoticed in the form of iceberg orders. I initially invested many hours on the side to put together an individual strategy.

I recommend you first look at the following articles.

A completely new market view

Volume versus liquidity

Why volume trading doesn't work

The Truth of successful Liquidity Traders

The truth about the volume profile

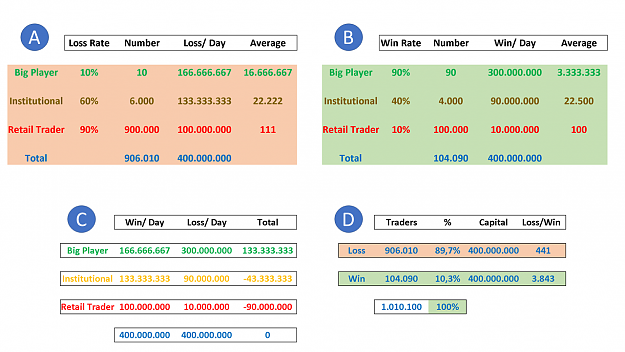

As I mentioned in many articles, it is crucial to find out why a bullish or bearish candle is created. A green, bullish candle arises because the euro is bought or the dollar is sold. A red, bearish candle arises because the euro is sold or the dollar is bought. When a big player pushes the price down and the stops of retail traders trigger a chain reaction by triggering further stops, this bearish candle has arisen because the euro was primarily sold. If this retail sale of euro by retail traders is now intercepted by the buy limit orders of the big players, this is a clear indication of an upward trend in the medium term. In addition to concentrating on limit orders, identifying cumulative market orders, open interest, the cumulative delta of limit orders, and reading out the algorithms of the big players with different tones, I tried to create a setup that made sense for me.

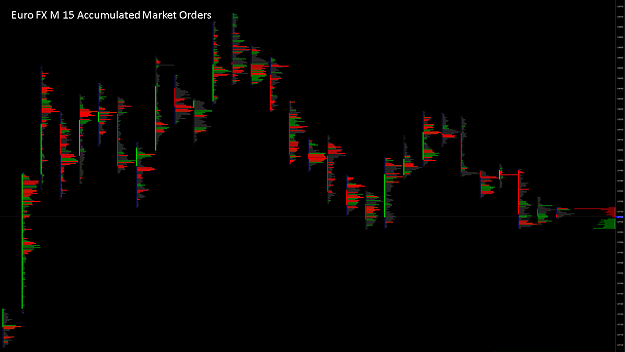

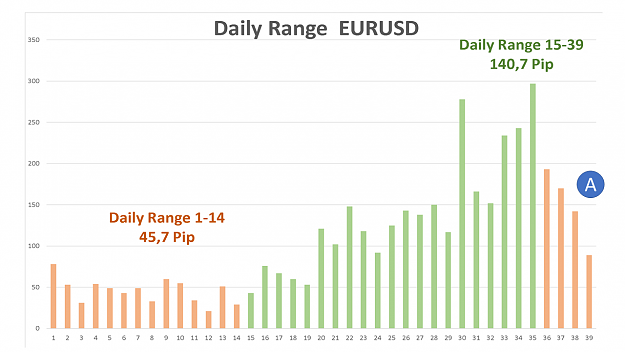

The daily range has tripled in the past 20 days and volatility has increased five-fold. This initially prevented me from starting my test run. After the open gap in the forex closed on Thursday, I expected a small drop in the daily range and volatility for Friday. So I started my first experiment on Friday to find out if my setup had a profitable chance.

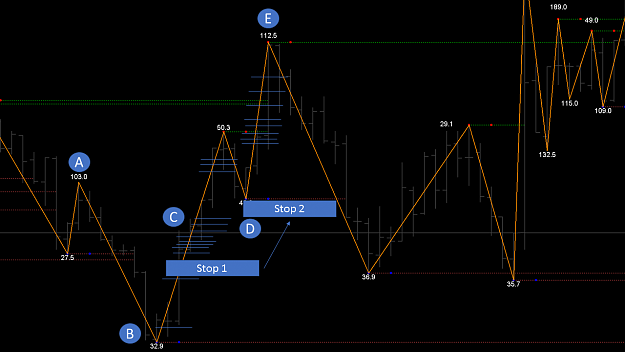

In the past I traded up and down the range in the Equilibrium. With the future data I have now concentrated on the smaller outbreaks that usually take place before a stophunting. At first it was difficult as a scalper to find the right entries, my plan was to use the best 20 trades of the day to generate a profitable trade. I only traded 18 trades because I still lacked some information, which I then corrected immediately. The experiment got off to a good start and I created an evaluation.

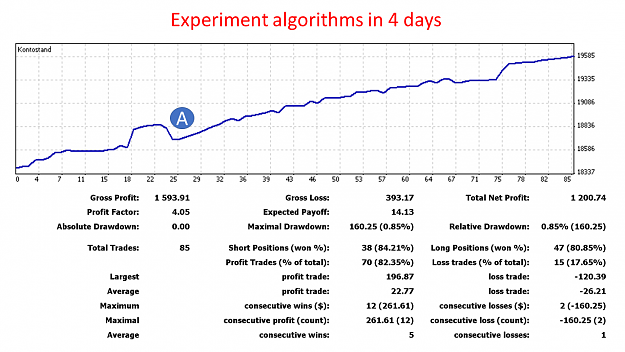

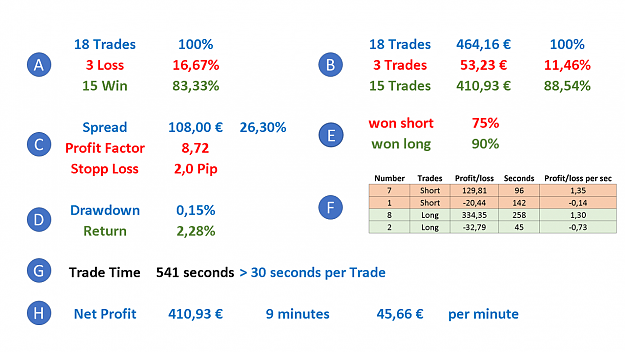

Point A

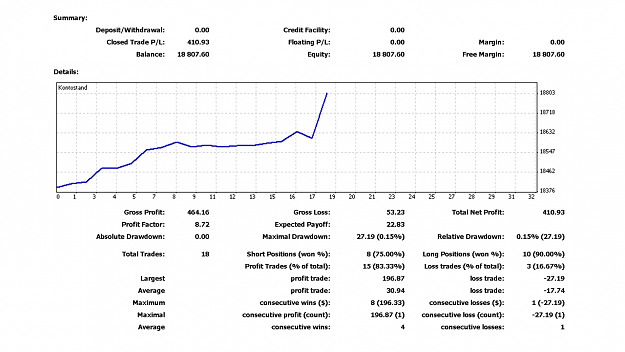

Overall, I made 18 trades in 9 hours from 09:00 CET to 18:00 CET. I lost 3 trades and won 15 trades. This is initially a win ratio of over 83%.

Point B

Overall, I won € 464 and lost € 53, leaving a net € 411. In this case the win ratio was over 88%.

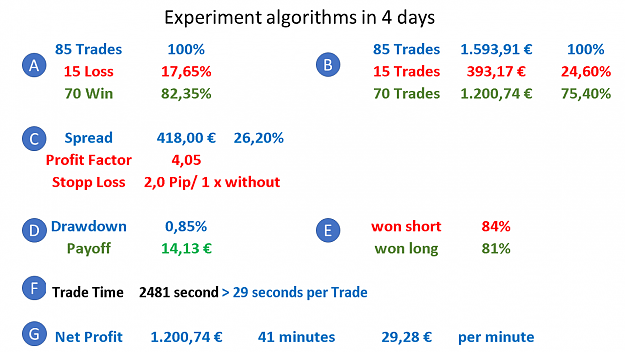

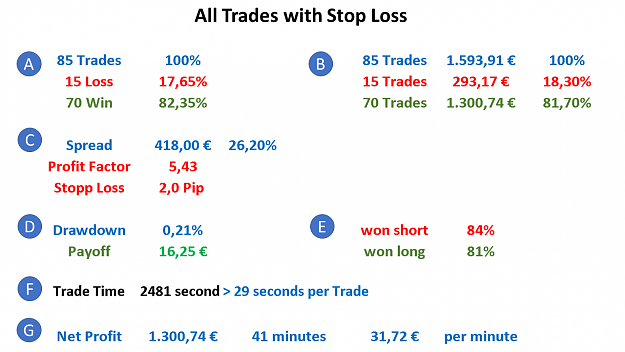

Point C

I paid my broker a spread of € 108 for these 18 trades, which I also had to earn, because I don't have to pay a commission. The spread was a bit higher than usual, normaly I pay € 72. That would have increased my profit again.

The profit factor was 8.72 since I won € 464.16 and lost 53.23 at the same time. I can be very satisfied with this value.

My first stop loss was 2.7 pip, which I reduced to 2 pip after my first loss. Since I traded the small breakouts, the price should move in my direction immediately after I started, so I am considering reducing the stop loss to 1.5 - 1 pip in the future.

Point D

The drawdown was initially very small because I traded with relatively little Lot. This drawdown will increase significantly in the future. With an account size of € 18,000 and a risk of 1.5 pip with 10 lots, the drawdown would increase to 2.5%, with the same profit ratio. The future risk per trade would then be 0.83% and could be increased to 1.7% in exceptional situations. The return of 2.28% is based on the fact that I was very cautious at first. This could increase drastically if the number of lots is increased.

Point E

What I was particularly pleased about is the fact that I won more long trades than short trades, since I was much more successful with short trades in the past. Maybe also because the short trades run about 30-40% faster than the long trades. But let's take a closer look at the analysis.

Point F

With 7 short trades, I was able to win € 129.81 in a total of 96 seconds, which is a profit of € 1.35 per second. With 8 long trades, I was able to win € 334.35 in a total of 258 seconds, which is a profit of € 1.30 per second. Although I won more on the long side than on the short side, the short side is still more efficient. I will keep an eye on that. In the long range I lose 0.73 € per second while on the short side I only lose 0.17 €. This is also an argument for the short area. The longest trade I made was the short loss of 142 seconds. This is once again proof of the principle of hope. I just waited too long and hoped that the trade would develop in my favor. Typical human behavior.

Point G

Overall, I spent 541 seconds in the market with the 18 trades, which is an average of 30 seconds per trade. Of a total of 9 hours (32,400 seconds) I only used 1.67% of the time to trade in the market. That means there is still enough potential for interesting trade entries.

Point H

The net profit was 410.93 that achieved in 9 minutes, that is a profit of € 45.66 per minute and a very good hourly wage. By increasing the number of lots, this profit can be increased significantly in 9 minutes, with a maximum risk of 0.83% per trade. In this experiment I tried to filter out the best signals for me. One would first have to check whether further signals reduce the profit rate. If that were the case, the risk would have to be increased to 1.7%. This would make a profit 20 times as high as in this experiment.

However, one would have to expect significantly lower volatility and range in the future, which would realistically enable a profit 6 times as high as in this experiment. However, it is questionable whether this high probability of winning can be maintained in the future. The best times in EURUSD are from 07:00 CET to 11:30 CET and from 14:00 CET to 19:30 CET. That is 10 hours to identify optimal trading signals. Part of my future experiments will be to find out if I can trade profitably with less qualitative trading signals. This will result in the future strategy. Either I use further trade signals to keep the risk low or I increase the risk to 1.7% per trade to optimize profits.

Conclusion:

The result is initially positive, but should not be overestimated as it could also be a coincidence. At the same time, this result is also confirmation that the experiment will be followed up. The more data is collected, the more precise a statement will be about my approach.

What did I do differently in this experiment than before?

In principle, nothing, since much of my trading is still based on intuition and experience. I don't sit in front of my screen and watch for a signal that tells me to go long or short. It is a series of different information that I intuitively combine from my 8 screens into one story and make an immediate trading decision. In the past 10 years I have done this a few thousand times in the Equilibrium and today I am able to use this experience. A Setup is an individual thing, even if I described my approach exactly, the result for other traders would still be different. You have to compare that with a setup of a racing car. If a racing driver were to drive with his colleague's setup, this could possibly lead to a bad accident. In this blog you will find different ideas to create your own setup. No one else can do this work for you. Successful trading does not work by waiting for intersecting Moving Averages who tell you: Entry or Exit. Successful trading is a hell of a challenge. I work with complicated algorithms and extremely well-resolved and filtered stock market data, but I still lose regularly.

A subscriber on our blog put it so nicely, I would like to quote his words.

In the DAX, I trade in the M1 with very short-term trades to cut out a few points. Why do I achieve a hit rate of 75% in good phases? (By "good phase" I mean: if I can suppress the gambling instinct, that is to say I am maximally disciplined). The fact is that I somehow now see what - probably - is about to happen. Of course not just intuition and gut feeling, but also based on rational considerations (and a lot of screen time in recent years). But I like to compare it to driving on the motorway: Why do I know that the car in the right lane will probably change to the left lane (although it is not flashing)?

I think he put it in a nutshell.

It is precisely this intuition, the gut feeling and a rational approach that will bring the long-term success you want. For that you have to be ready to work hard (screentime, screentime and again screentime). I am very proud that this blog brings together so many traders who take their work very seriously. That will take us all one step further.

Many thanks to all subscribers who make this blog so successful.

I wish you a relaxing weekend

Lovely wishes

Michael

Hello dear subscribers,

For almost a year now I have been dealing very extensively with the stock market data that I use exclusively for my trading in Forex. At first, like most future traders, I concentrated on the volume, but found that the big players primarily absorb the volume with their limit orders in order to collect the required number of bid and ask. The big players used the volume, in the form of market orders, only to keep the price within a range or to push the price in their direction in order to fill their limit orders with compressed volumes (stops of retail traders). In addition, they began to make massive amounts of liquidity and volume available to themselves when there was relatively little volume on the market. You can also find some posts about this in this blog.

Experiment own liquidity continues!

Overall, the decisive factor is in the area of limit orders, since most traders ignore them. For this reason, in the past few weeks I have concentrated exclusively on the decisive liquidity (limit orders) that come into the market unnoticed in the form of iceberg orders. I initially invested many hours on the side to put together an individual strategy.

I recommend you first look at the following articles.

A completely new market view

Volume versus liquidity

Why volume trading doesn't work

The Truth of successful Liquidity Traders

The truth about the volume profile

Attached Image (click to enlarge)

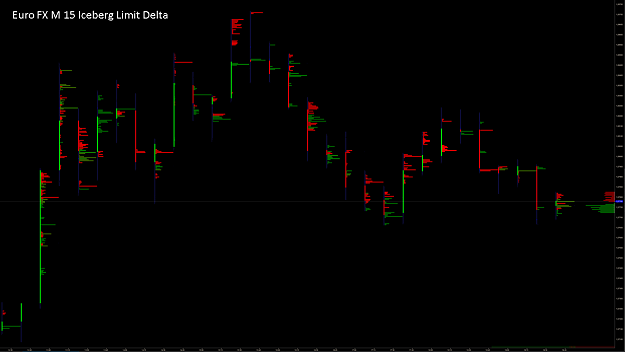

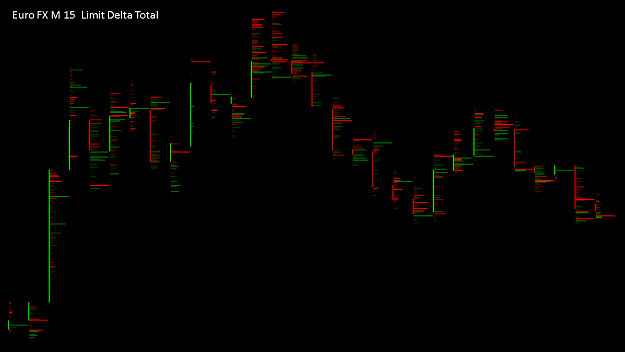

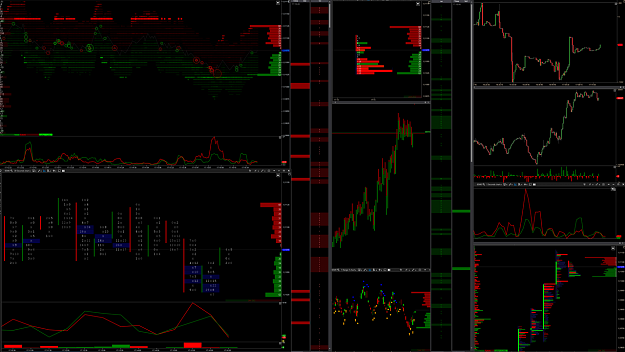

As I mentioned in many articles, it is crucial to find out why a bullish or bearish candle is created. A green, bullish candle arises because the euro is bought or the dollar is sold. A red, bearish candle arises because the euro is sold or the dollar is bought. When a big player pushes the price down and the stops of retail traders trigger a chain reaction by triggering further stops, this bearish candle has arisen because the euro was primarily sold. If this retail sale of euro by retail traders is now intercepted by the buy limit orders of the big players, this is a clear indication of an upward trend in the medium term. In addition to concentrating on limit orders, identifying cumulative market orders, open interest, the cumulative delta of limit orders, and reading out the algorithms of the big players with different tones, I tried to create a setup that made sense for me.

Attached Image (click to enlarge)

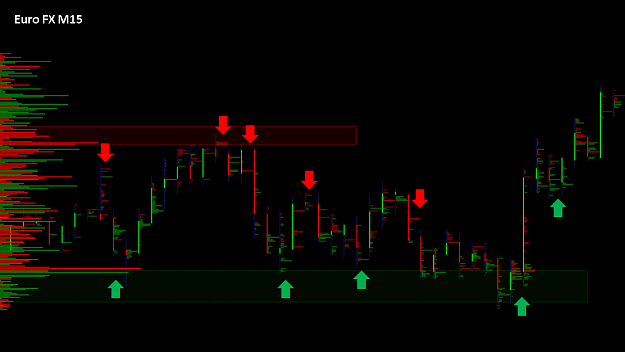

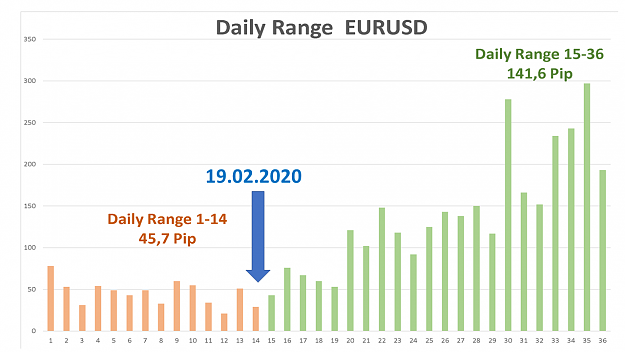

The daily range has tripled in the past 20 days and volatility has increased five-fold. This initially prevented me from starting my test run. After the open gap in the forex closed on Thursday, I expected a small drop in the daily range and volatility for Friday. So I started my first experiment on Friday to find out if my setup had a profitable chance.

Attached Image (click to enlarge)

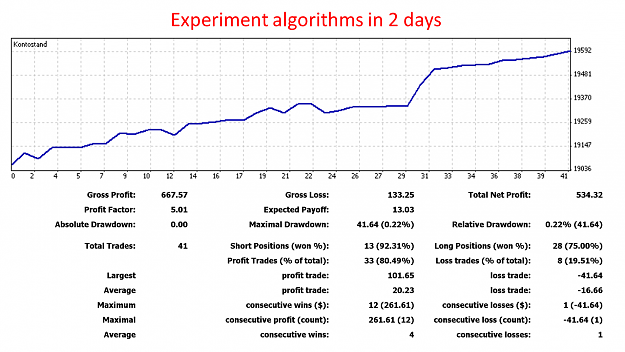

In the past I traded up and down the range in the Equilibrium. With the future data I have now concentrated on the smaller outbreaks that usually take place before a stophunting. At first it was difficult as a scalper to find the right entries, my plan was to use the best 20 trades of the day to generate a profitable trade. I only traded 18 trades because I still lacked some information, which I then corrected immediately. The experiment got off to a good start and I created an evaluation.

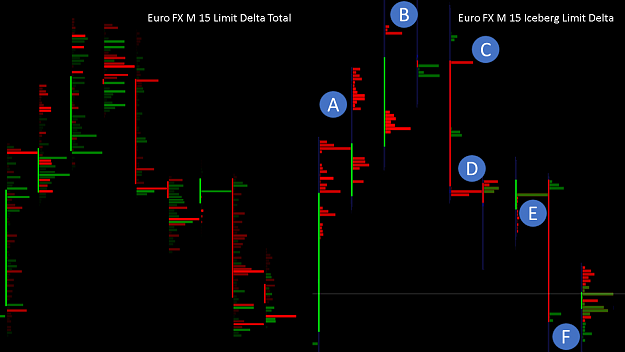

Attached Image (click to enlarge)

Point A

Overall, I made 18 trades in 9 hours from 09:00 CET to 18:00 CET. I lost 3 trades and won 15 trades. This is initially a win ratio of over 83%.

Point B

Overall, I won € 464 and lost € 53, leaving a net € 411. In this case the win ratio was over 88%.

Point C

I paid my broker a spread of € 108 for these 18 trades, which I also had to earn, because I don't have to pay a commission. The spread was a bit higher than usual, normaly I pay € 72. That would have increased my profit again.

The profit factor was 8.72 since I won € 464.16 and lost 53.23 at the same time. I can be very satisfied with this value.

My first stop loss was 2.7 pip, which I reduced to 2 pip after my first loss. Since I traded the small breakouts, the price should move in my direction immediately after I started, so I am considering reducing the stop loss to 1.5 - 1 pip in the future.

Point D

The drawdown was initially very small because I traded with relatively little Lot. This drawdown will increase significantly in the future. With an account size of € 18,000 and a risk of 1.5 pip with 10 lots, the drawdown would increase to 2.5%, with the same profit ratio. The future risk per trade would then be 0.83% and could be increased to 1.7% in exceptional situations. The return of 2.28% is based on the fact that I was very cautious at first. This could increase drastically if the number of lots is increased.

Point E

What I was particularly pleased about is the fact that I won more long trades than short trades, since I was much more successful with short trades in the past. Maybe also because the short trades run about 30-40% faster than the long trades. But let's take a closer look at the analysis.

Point F

With 7 short trades, I was able to win € 129.81 in a total of 96 seconds, which is a profit of € 1.35 per second. With 8 long trades, I was able to win € 334.35 in a total of 258 seconds, which is a profit of € 1.30 per second. Although I won more on the long side than on the short side, the short side is still more efficient. I will keep an eye on that. In the long range I lose 0.73 € per second while on the short side I only lose 0.17 €. This is also an argument for the short area. The longest trade I made was the short loss of 142 seconds. This is once again proof of the principle of hope. I just waited too long and hoped that the trade would develop in my favor. Typical human behavior.

Point G

Overall, I spent 541 seconds in the market with the 18 trades, which is an average of 30 seconds per trade. Of a total of 9 hours (32,400 seconds) I only used 1.67% of the time to trade in the market. That means there is still enough potential for interesting trade entries.

Point H

The net profit was 410.93 that achieved in 9 minutes, that is a profit of € 45.66 per minute and a very good hourly wage. By increasing the number of lots, this profit can be increased significantly in 9 minutes, with a maximum risk of 0.83% per trade. In this experiment I tried to filter out the best signals for me. One would first have to check whether further signals reduce the profit rate. If that were the case, the risk would have to be increased to 1.7%. This would make a profit 20 times as high as in this experiment.

However, one would have to expect significantly lower volatility and range in the future, which would realistically enable a profit 6 times as high as in this experiment. However, it is questionable whether this high probability of winning can be maintained in the future. The best times in EURUSD are from 07:00 CET to 11:30 CET and from 14:00 CET to 19:30 CET. That is 10 hours to identify optimal trading signals. Part of my future experiments will be to find out if I can trade profitably with less qualitative trading signals. This will result in the future strategy. Either I use further trade signals to keep the risk low or I increase the risk to 1.7% per trade to optimize profits.

Conclusion:

The result is initially positive, but should not be overestimated as it could also be a coincidence. At the same time, this result is also confirmation that the experiment will be followed up. The more data is collected, the more precise a statement will be about my approach.

What did I do differently in this experiment than before?

In principle, nothing, since much of my trading is still based on intuition and experience. I don't sit in front of my screen and watch for a signal that tells me to go long or short. It is a series of different information that I intuitively combine from my 8 screens into one story and make an immediate trading decision. In the past 10 years I have done this a few thousand times in the Equilibrium and today I am able to use this experience. A Setup is an individual thing, even if I described my approach exactly, the result for other traders would still be different. You have to compare that with a setup of a racing car. If a racing driver were to drive with his colleague's setup, this could possibly lead to a bad accident. In this blog you will find different ideas to create your own setup. No one else can do this work for you. Successful trading does not work by waiting for intersecting Moving Averages who tell you: Entry or Exit. Successful trading is a hell of a challenge. I work with complicated algorithms and extremely well-resolved and filtered stock market data, but I still lose regularly.

A subscriber on our blog put it so nicely, I would like to quote his words.

In the DAX, I trade in the M1 with very short-term trades to cut out a few points. Why do I achieve a hit rate of 75% in good phases? (By "good phase" I mean: if I can suppress the gambling instinct, that is to say I am maximally disciplined). The fact is that I somehow now see what - probably - is about to happen. Of course not just intuition and gut feeling, but also based on rational considerations (and a lot of screen time in recent years). But I like to compare it to driving on the motorway: Why do I know that the car in the right lane will probably change to the left lane (although it is not flashing)?

I think he put it in a nutshell.

It is precisely this intuition, the gut feeling and a rational approach that will bring the long-term success you want. For that you have to be ready to work hard (screentime, screentime and again screentime). I am very proud that this blog brings together so many traders who take their work very seriously. That will take us all one step further.

Many thanks to all subscribers who make this blog so successful.

I wish you a relaxing weekend

Lovely wishes

Michael

Forget:That does not work, amateurs build the ark, pros the Titanic!

12