EURO

The downturn also shows further signs of spreading from manufacturing to services. While the goods-producing sector is stuck in its deepest downturn since 2012, the service sector has also seen its growth rate slow sharply to one of the weakest for six years. “The deteriorating picture is being led by a downturn in Germany, but France and Italy are also close to stalling and Spain has seen growth slow to the joint-lowest in around six years.

“The growing risk of recession, coupled with a further moderation of inflationary pressures, will add to expectations that the ECB will need to do more to stimulate the economy in coming months

ECB interest rates to remain at their present or lower levels until it saw the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence was consistently reflected in underlying inflation dynamics.

Net purchases would be restarted under the Governing Council’s APP at a monthly pace of €20 billion as from 1 November.

quarterly targeted longer-term refinancing operations (TLTRO III) would be changed to preserve favourable bank lending condition. For banks whose eligible net lending exceeded a benchmark, the rate applied in TLTRO III operations would be lower, and could be as low as the average interest rate on the deposit facility prevailing over the life of the operation. The maturity of the operations would be extended from two to three years.

Overall, loan growth was still benefiting from historically low bank lending rates. Bank lending conditions for firms and households continued to be very favourable.

In short, further easing of the monetary policy stance was warranted .

so in mid term, inflation will be achieved but coming for next month onwards, you will see more weaker Euro in order to achieve their low target monetary policy..

The downturn also shows further signs of spreading from manufacturing to services. While the goods-producing sector is stuck in its deepest downturn since 2012, the service sector has also seen its growth rate slow sharply to one of the weakest for six years. “The deteriorating picture is being led by a downturn in Germany, but France and Italy are also close to stalling and Spain has seen growth slow to the joint-lowest in around six years.

“The growing risk of recession, coupled with a further moderation of inflationary pressures, will add to expectations that the ECB will need to do more to stimulate the economy in coming months

ECB interest rates to remain at their present or lower levels until it saw the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence was consistently reflected in underlying inflation dynamics.

Net purchases would be restarted under the Governing Council’s APP at a monthly pace of €20 billion as from 1 November.

quarterly targeted longer-term refinancing operations (TLTRO III) would be changed to preserve favourable bank lending condition. For banks whose eligible net lending exceeded a benchmark, the rate applied in TLTRO III operations would be lower, and could be as low as the average interest rate on the deposit facility prevailing over the life of the operation. The maturity of the operations would be extended from two to three years.

Overall, loan growth was still benefiting from historically low bank lending rates. Bank lending conditions for firms and households continued to be very favourable.

In short, further easing of the monetary policy stance was warranted .

so in mid term, inflation will be achieved but coming for next month onwards, you will see more weaker Euro in order to achieve their low target monetary policy..

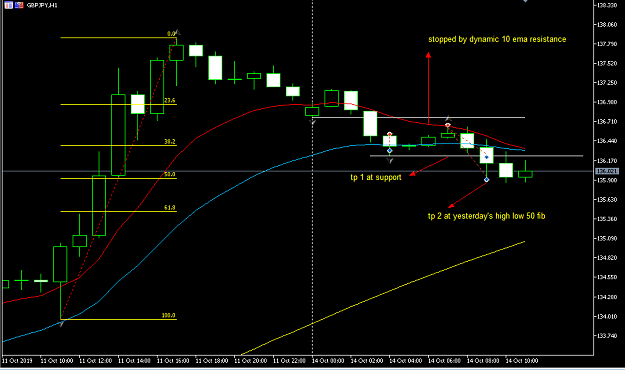

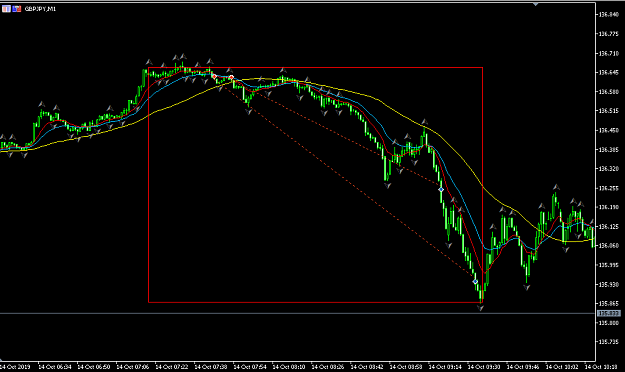

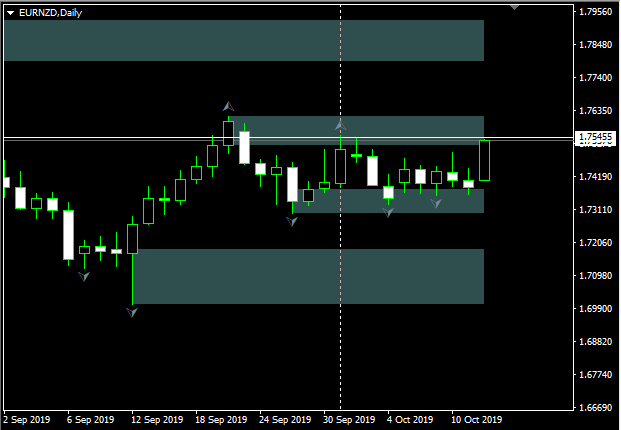

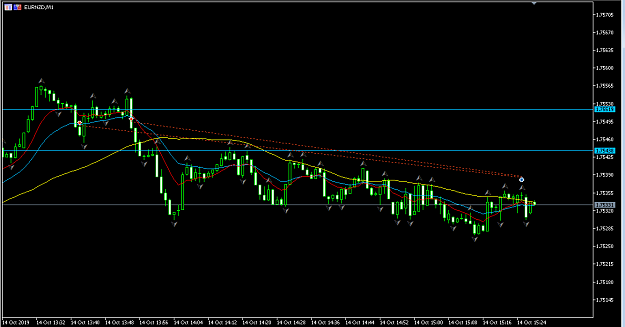

Attached Image(s) (click to enlarge)

Let Market Tell You

2