AO, you have shared plenty of extremely valuable information and ideas around the concept of mean reversion.

Many of us sincerely appreciate your contributions and sharing of information. We look forward to more details regarding your thinking around this concept to grow our knowledge within this area.

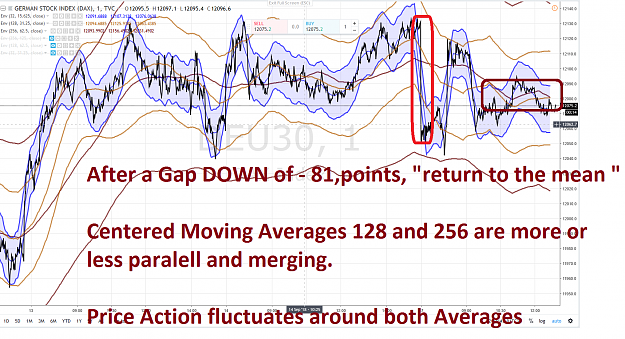

For me, the concept of "mean" is a reference point. This reference point could come in many forms. It could be measured by simple moving averages, ATR, or even using various forms of custom indicators.

These 3 factors have kept me grounded when it comes to creating a mean reverting portfolio:

1) Diversification

2) Position sizing

3) Trade management

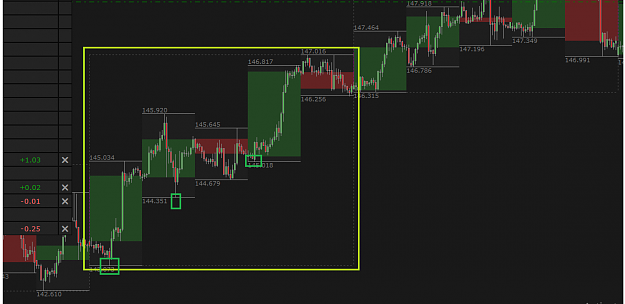

Entry and exit conditions would form part of the equation of a mean reverting strategy, and could range stretch from intraday, weekly to monthly in terms of time horizon. This is not to discount the fact that intraday closures are not optimal - I just couldn't replicate better results with a day-end close.

I couldn't stress more about the importance of diversification for pure mean reverting portfolios because of the fact that you need to spread your risk out across as many currency pairs as possible, and it's not always a bed of roses if you trade just one single currency pair.

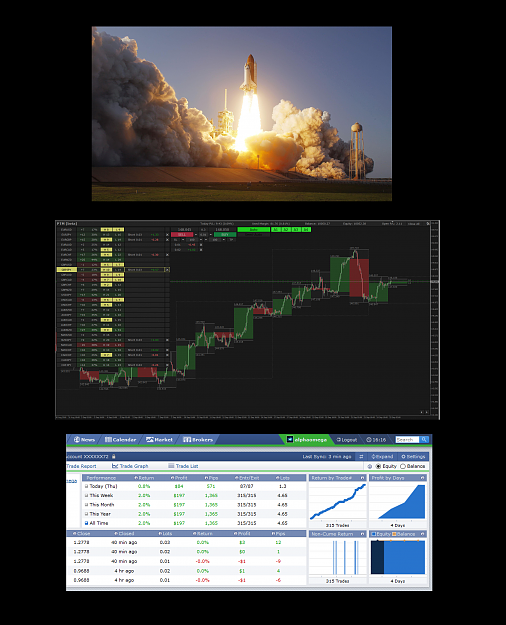

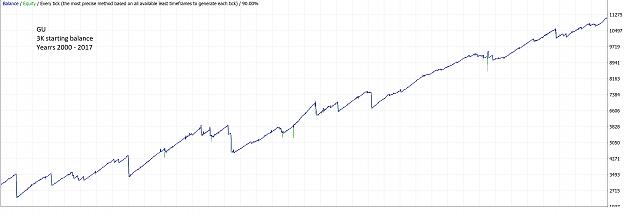

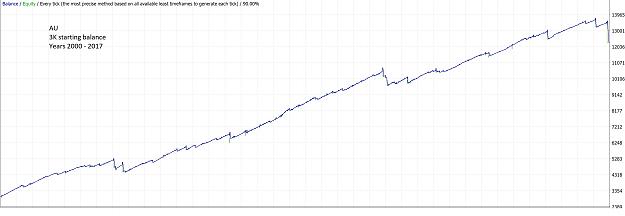

View the attachments for some examples for GU and AU. I may spend more time elaborating and I am keen to hear more from AO about his current methodology.

Time to hit the bed, it's been a long day..

Many of us sincerely appreciate your contributions and sharing of information. We look forward to more details regarding your thinking around this concept to grow our knowledge within this area.

For me, the concept of "mean" is a reference point. This reference point could come in many forms. It could be measured by simple moving averages, ATR, or even using various forms of custom indicators.

These 3 factors have kept me grounded when it comes to creating a mean reverting portfolio:

1) Diversification

2) Position sizing

3) Trade management

Entry and exit conditions would form part of the equation of a mean reverting strategy, and could range stretch from intraday, weekly to monthly in terms of time horizon. This is not to discount the fact that intraday closures are not optimal - I just couldn't replicate better results with a day-end close.

I couldn't stress more about the importance of diversification for pure mean reverting portfolios because of the fact that you need to spread your risk out across as many currency pairs as possible, and it's not always a bed of roses if you trade just one single currency pair.

View the attachments for some examples for GU and AU. I may spend more time elaborating and I am keen to hear more from AO about his current methodology.

Time to hit the bed, it's been a long day..

Attached Image(s) (click to enlarge)

3