-

Commodity Market Report: Bonds Forex Metals Energy - Elliott Wave Trading Strategies

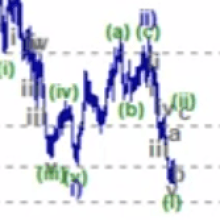

Commodity Market Report Technical Analysis Elliott Wave and Trading Strategies. Content: US Bond Yields, USD, DXY, USDCAD USDJPY, EURUSD, GBPUSD, AUDUSD, US Gold, GDX, Silver, Copper, Iron Ore, Lithium, Nickel, Crude Oil, Natural Gas. Commodities Market Summary: US Dollar is confirmed as bearish, opening the door for long trades in markets such as AUD, GBP, EUR, Gold, Silver. Trading Strategies: See video. Video Chapters: 00:00 US Gov Bonds 10 Yr Yields / AU 10 Yr Bonds. 00:51 Forex: US Dollar Index, DXY, USDCAD USDJPY, EURUSD, GBPUSD, AUDUSD. 09:34 Precious Metals: Spot Gold / GDX ETF / US Spot Silver. 20:43 Base ... (full story)

- Comments

- Subscribe

-

- Older Stories

From rbnz.govt.nz|Jul 11, 2023|1 comment

From rbnz.govt.nz|Jul 11, 2023|1 commentThe Monetary Policy Committee today agreed to leave the Official Cash Rate (OCR) at 5.50%. The level of interest rates are constraining spending and inflation pressure as anticipated and required. The Committee agreed that the OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1 to 3% annual target range, while supporting maximum sustainable employment. Global economic growth remains weak and inflation pressures are easing. This follows a period of significant monetary policy tightening by central banks internationally. Global inflation rates continue to decline, assisted by the normalisation of international supply chains, and the decline in shipping costs and energy prices. The weaker global growth has led to lower export prices for New Zealand's goods. In New Zealand, inflation is expected to continue to decline from its peak, and with it measures of inflation expectations. Core inflation is expected to decline as capacity constraints ease. While employment is above its maximum sustainable level, there are signs of labour market pressures dissipating and vacancies declining. Consumer spending post at 10:06pm: RBNZ: #OCR To Remain Restrictive For The Foreseeable Future - Committee Reached Consensus To Leave OCR Unchanged - Confident Restrictive Rates Will Return CPI To Target $NZDUSD https://t.co/Mx0Zj8WdgP post at 10:06pm: RBNZ: Level Of Rates Constraining Spending, Inflation - Inflation Expected To Continue To Decline - Signs Job Market Pressures Dissipating, Vacancies Falling - Consumer Spending Growth Has Slowed $NZDUSDOCR decision: RBNZ hits pause after two years of OCR hikes as economy shows signs of slowing The Reserve Bank left the Official Cash Rate (OCR) unchanged at 5.50% at its monetary policy review on Wednesday, ending almost two years of consecutive rate hikes. “The level of interest rates are constraining spending and inflation pressure as anticipated and required,” it said in a statement. Economists and traders had agreed the central bank would not increase the benchmark interest rate at its July meeting, as foreshadowed in its May Monetary Policy Statement. It was the first meeting since October 2021 that the Monetary Policy Committee did not lift the OCR. During that time, the cash rate was increased 525 basis points in a dozen consecutive decisions and is now at its highest level since late 2008 at 5.50%. In May, the RBNZ said it believed interest rates were high enough to bring inflation back into the target range and signalled it would freeze the OCR until mid-2024. On Wednesday, it said global economic growth remained weak and inflation pressures were easing following significant monetary policy tightening. Stephen Toplis, BNZ’s head of research, said the central bank would be “feeling comfortable” about the data released since then. First quarter gross domestic product was weaker than expected, the quarterly survey of business opinion showed the labour shortage easing, while pricing intentions and inflation expectations have fallen. However, some analysts are still predicting another 25 basis point hike before the end of the year. Markets were priced for another increase by November. This view could be encouraged (or discouraged) by a Consumer Price Index (CPI) data release next week, which is likely to show an annual inflation rate of around 6% in the second quarter. Annual inflation was running at 6.7% in the first quarter of 2023 and has been as high as 7.3%. The Reserve Bank said it expects headline inflation to continue to decline from its peak and core inflation to also fall as capacity constraints ease. “While employment is above its maximum sustainable level, there are signs of labour market pressures dissipating and vacancies declining,” it

From fxempire.com|Jul 11, 2023

From fxempire.com|Jul 11, 2023It is a relatively quiet start to the day, with no economic indicators to provide direction to the AUD/USD and NZD/USD. However, while there are no economic indicators to ...

From forexlive.com|Jul 11, 2023

From forexlive.com|Jul 11, 2023Australian Treasurer Chalmers says yet to finalise who the next Reserve Bank of Australia Governor will be. Cabinet is yet to vote on it. The current Governor Lowe's term expires ...

-

- Newer Stories

From news.com.au|Jul 11, 2023

From news.com.au|Jul 11, 2023RBA Governor Philip Lowe is set to deliver his last speech today before finding out whether he will be replaced in a huge shake up. The central banker who infamously predicted ...

From rba.gov.au|Jul 11, 2023|1 comment

From rba.gov.au|Jul 11, 2023|1 commentThank you for the invitation to address the Economic Society of Australia, here in Queensland. This is the fourth time that I have had the honour to do so, and it is a great ...

From channelnewsasia.com|Jul 11, 2023

From channelnewsasia.com|Jul 11, 2023Japan's wholesale inflation slowed for a sixth straight month in June due to sliding fuel and commodity prices, data showed on Wednesday, a sign the cost-push pressure that drove ...

- Story Stats

- Posted: Jul 11, 2023 10:28pm

- Submitted by:Category: Technical AnalysisComments: 0 / Views: 3,919