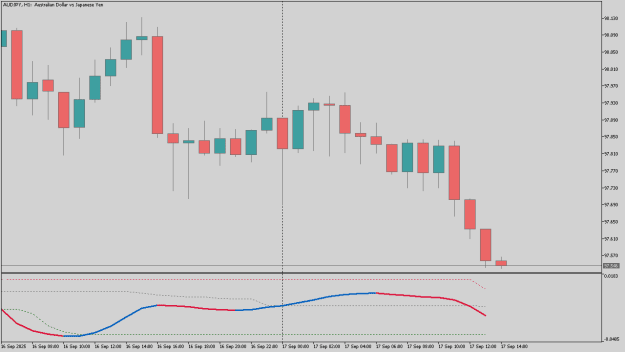

There was no MQL5 source code available for the Dynamic Zones Polychromatic Momentum, so I attempted to create this version.

To summarize:

To summarize:

- It doesn’t repaint on closed bars.

- The problem is the signal line and dynamic zones don’t recalculate or display correctly on the current (open) bar.

If you don’t need the current bar, the code can be tweaked so it just leaves bar 0 blank. If you do find the current bar useful, I’d really appreciate if someone could help fix that part.

Inserted Code

//+------------------------------------------------------------------+

//| Created by Th3W1z4rd using ChatGPT 5 Thinking model |

//| Dynamic Zones Polychromatic Momentum for MT5 |

//| MT4 version by Mladen Rakic |

//| https://forex-station.com/attach/file/3257739 |

//+------------------------------------------------------------------+

#property copyright "Public domain"

#property version "1.961"

#property strict

// separate subwindow, 5 buffers, 4 plotted lines

#property indicator_separate_window

#property indicator_buffers 5

#property indicator_plots 4

// plot 0: zero line

#property indicator_type1 DRAW_LINE

#property indicator_color1 clrDimGray

#property indicator_label1 "Zero"

#property indicator_style1 STYLE_DOT

// plot 1: upper dynamic zone

#property indicator_type2 DRAW_LINE

#property indicator_color2 clrCrimson

#property indicator_label2 "Overbought"

#property indicator_style2 STYLE_DOT

// plot 2: lower dynamic zone

#property indicator_type3 DRAW_LINE

#property indicator_color3 clrDarkGreen

#property indicator_label3 "Oversold"

#property indicator_style3 STYLE_DOT

// plot 3: main momentum line with color by slope

#property indicator_type4 DRAW_COLOR_LINE

#property indicator_color4 C'0,95,190', clrCrimson

#property indicator_width4 3

#property indicator_label4 "Momentum"

// price source options

enum enPrices { pr_close=0, pr_open, pr_high, pr_low, pr_median, pr_typical, pr_weighted, pr_average };

// core settings

input int MomentumLength = 14; // momentum lookback length

input enPrices Price = pr_close; // price used for momentum

input int SmoothLength = 10; // adaptive smoother length

input double SmoothPhase = 0.0; // adaptive smoother phase

// dynamic zones settings

input int DzLookBackBars = 35; // rolling window for quantiles

input double DzStartBuyProbability = 0.05; // lower zone quantile

input double DzStartSellProbability = 0.95; // upper zone quantile

// optional redraw controls

input bool UseTimerRecalc = false; // enable timer-based redraw

input int TimerSeconds = 1; // timer interval seconds

input int TimerRecalcBars = 1500; // reserved

// behavior flags

input bool StrictClosedBars = true; // keep history frozen

input bool MirrorBar1ToBar0 = false; // legacy toggle, not used

// indicator buffers

double ZeroBuffer[]; // median of momentum (DZ mid)

double ObBuffer[]; // upper dynamic zone

double OsBuffer[]; // lower dynamic zone

double MomBuffer[]; // smoothed momentum

double MomColor[]; // color index for momentum slope

// scratch arrays for smoothing and quantiles

static double qtmp[]; // temp values for window quantile

double wrk[][10]; // state used by iSmooth

#define bsmax 5

#define bsmin 6

#define volty 7

#define vsum 8

#define avolty 9

// state tracking

uint g_last_calc_ms = 0; // timestamp of last calc

uint g_skip_timer_until_ms = 0; // throttle chart-change refresh

int g_last_committed_closed = -1;// last closed bar processed

// clamp index into [0, n-1]

int clamp_index(int idx, int n)

{

if(n <= 0) return 0;

if(idx < 0) return 0;

if(idx >= n) return n - 1;

return idx;

}

// adaptive smoother, keeps rolling state in wrk

double iSmooth(double price, double length, double phase, int i, int bars, int s=0)

{

if(length <= 1) return(price);

if(bars <= 0) return(price);

if(ArrayRange(wrk,0) != bars) ArrayResize(wrk, bars);

int r = bars - i - 1;

r = clamp_index(r, bars);

// seed on first record

if(r == 0)

{

int k;

for(k = 0; k < 7; k++) wrk[r][k + s] = price;

for(; k < 10; k++) wrk[r][k + s] = 0.0;

return(price);

}

// volatility-adaptive section

double len1 = MathMax(MathLog(MathSqrt(0.5 * (length - 1))) / MathLog(2.0) + 2.0, 0);

double pow1 = MathMax(len1 - 2.0, 0.5);

double del1 = price - wrk[r - 1][bsmax + s];

double del2 = price - wrk[r - 1][bsmin + s];

double div = 1.0 / (10.0 + 10.0 * (MathMin(MathMax(length - 10, 0), 100)) / 100);

int forBar = MathMin(r, 10);

wrk[r][volty + s] = 0;

if(MathAbs(del1) > MathAbs(del2)) wrk[r][volty + s] = MathAbs(del1);

if(MathAbs(del1) < MathAbs(del2)) wrk[r][volty + s] = MathAbs(del2);

int r_for = clamp_index(r - forBar, bars);

wrk[r][vsum + s] = wrk[r - 1][vsum + s] + (wrk[r][volty + s] - wrk[r_for][volty + s]) * div;

wrk[r][avolty + s] = wrk[r - 1][avolty + s] + (2.0 / (MathMax(MathMin(length, 30) + 1.0, 1.0))) * (wrk[r][vsum + s] - wrk[r - 1][avolty + s]);

double dVolty = wrk[r][avolty + s] > 0 ? wrk[r][volty + s] / wrk[r][avolty + s] : 0;

if(dVolty < 1) dVolty = 1.0;

double pow2 = MathPow(dVolty, pow1);

double len2 = MathSqrt(0.5 * (length - 1)) * len1;

double Kv = MathPow(len2 / (len2 + 1), MathSqrt(pow2));

if(del1 > 0) wrk[r][bsmax + s] = price; else wrk[r][bsmax + s] = price - Kv * del1;

if(del2 < 0) wrk[r][bsmin + s] = price; else wrk[r][bsmin + s] = price - Kv * del2;

// filter core

double R = MathMax(MathMin(phase, 100), -100) / 100.0 + 1.5;

double beta = 0.45 * (length - 1) / (0.45 * (length - 1) + 2);

double alpha = MathPow(beta, pow2);

wrk[r][0 + s] = price + alpha * (wrk[r - 1][0 + s] - price);

wrk[r][1 + s] = (price - wrk[r][0 + s]) * (1 - beta) + beta * wrk[r - 1][1 + s];

wrk[r][2 + s] = (wrk[r][0 + s] + R * wrk[r][1 + s]);

wrk[r][3 + s] = (wrk[r][2 + s] - wrk[r - 1][4 + s]) * MathPow((1 - alpha), 2) + MathPow(alpha, 2) * wrk[r - 1][3 + s];

wrk[r][4 + s] = (wrk[r - 1][4 + s] + wrk[r][3 + s]);

return(wrk[r][4 + s]);

}

// pick price per input setting

double getPrice(enPrices p, const double &open[], const double &close[], const double &high[], const double &low[], int i)

{

int n = ArraySize(close);

i = clamp_index(i, n);

switch(p)

{

case pr_close: return close[i];

case pr_open: return open[i];

case pr_high: return high[i];

case pr_low: return low[i];

case pr_median: return (high[i] + low[i]) / 2.0;

case pr_typical: return (high[i] + low[i] + close[i]) / 3.0;

case pr_weighted:return (high[i] + low[i] + close[i] + close[i]) / 4.0;

case pr_average: return (high[i] + low[i] + open[i] + close[i]) / 4.0;

}

return close[i];

}

// rolling quantile over closed bars only; excludes bar 0

double window_quantile(const double &arr[], int i, int bars, int lookBack, double q, int last_closed)

{

if(bars <= 0) return EMPTY_VALUE;

i = clamp_index(i, bars);

if(lookBack <= 1) return arr[i];

if(q < 0.0) q = 0.0;

if(q > 1.0) q = 1.0;

int start = MathMax(i, 1); // avoid using bar 0 in zone stats

if(last_closed < start) return arr[i];

int max_take = MathMin(lookBack, last_closed - start + 1);

if(max_take <= 0) return arr[i];

ArrayResize(qtmp, max_take);

int count = 0;

// collect valid values

for(int j = 0; j < max_take; j++)

{

double v = arr[start + j];

if(v != EMPTY_VALUE && MathIsValidNumber(v))

qtmp[count++] = v;

}

if(count <= 0) return arr[i];

ArrayResize(qtmp, count);

ArraySort(qtmp);

// linear interpolation between ranks

double pos = q * (count - 1);

int idx = (int)MathFloor(pos);

double frac = pos - idx;

if(idx >= count - 1) return qtmp[count - 1];

return qtmp[idx] * (1.0 - frac) + qtmp[idx + 1] * frac;

}

// compute momentum and zones for bar i using data up to last_closed

void compute_bar(const int bars_clamped,

const double &open[],

const double &high[],

const double &low[],

const double &close[],

int i,

int last_closed)

{

int n = ArraySize(close);

if(n <= 0) return;

last_closed = clamp_index(last_closed, n);

i = clamp_index(i, n);

// weighted momentum using 1/sqrt(k+1)

double sumMom = 0.0, sumW = 0.0;

for(int k = 0; (i + k + 1) <= last_closed && k < MomentumLength; k++)

{

double w = MathSqrt(k + 1.0);

double price_i = getPrice(Price, open, close, high, low, i);

double price_ik1 = getPrice(Price, open, close, high, low, i + k + 1);

sumMom += (price_i - price_ik1) / w;

sumW += w;

}

double raw = (sumW > 0.0) ? sumMom / sumW : 0.0;

// smooth momentum

MomBuffer[i] = iSmooth(raw, SmoothLength, SmoothPhase, i, bars_clamped, 0);

// dynamic zones from quantiles of closed bars only

const double loq = DzStartBuyProbability;

const double hiq = DzStartSellProbability;

OsBuffer[i] = window_quantile(MomBuffer, i, bars_clamped, DzLookBackBars, loq, last_closed);

ObBuffer[i] = window_quantile(MomBuffer, i, bars_clamped, DzLookBackBars, hiq, last_closed);

ZeroBuffer[i] = window_quantile(MomBuffer, i, bars_clamped, DzLookBackBars, 0.5, last_closed);

// color by slope vs next bar

int next = i + 1;

double slope = (next <= last_closed && MomBuffer[next] != EMPTY_VALUE)

? (MomBuffer[i] - MomBuffer[next]) : 0.0;

MomColor[i] = (slope >= 0.0) ? 0.0 : 1.0;

}

// set buffers and visuals

int OnInit()

{

SetIndexBuffer(0, ZeroBuffer, INDICATOR_DATA);

SetIndexBuffer(1, ObBuffer, INDICATOR_DATA);

SetIndexBuffer(2, OsBuffer, INDICATOR_DATA);

SetIndexBuffer(3, MomBuffer, INDICATOR_DATA);

SetIndexBuffer(4, MomColor, INDICATOR_COLOR_INDEX);

ArraySetAsSeries(ZeroBuffer, true);

ArraySetAsSeries(ObBuffer, true);

ArraySetAsSeries(OsBuffer, true);

ArraySetAsSeries(MomBuffer, true);

ArraySetAsSeries(MomColor, true);

IndicatorSetString(INDICATOR_SHORTNAME, " ");

// minimal legend

for(int p=0; p<4; ++p)

{

PlotIndexSetInteger(p, PLOT_SHOW_DATA, false);

PlotIndexSetString(p, PLOT_LABEL, "");

}

// color indexes for momentum plot

PlotIndexSetInteger(3, PLOT_COLOR_INDEXES, 2);

// warmup period before first drawn momentum

PlotIndexSetInteger(3, PLOT_DRAW_BEGIN, MomentumLength + SmoothLength + DzLookBackBars);

if(UseTimerRecalc && TimerSeconds > 0) EventSetTimer(TimerSeconds);

g_last_committed_closed = -1;

return(INIT_SUCCEEDED);

}

// main calculation loop

int OnCalculate(const int rates_total,

const int prev_calculated,

const datetime &time[],

const double &open[],

const double &high[],

const double &low[],

const double &close[],

const long &tick_volume[],

const long &volume[],

const int &spread[])

{

// need at least one closed bar

if(rates_total < 2)

{

if(rates_total > 0)

{

ZeroBuffer[0] = ObBuffer[0] = OsBuffer[0] = MomBuffer[0] = EMPTY_VALUE;

MomColor[0] = 0.0;

}

return(prev_calculated);

}

// clear on first run

if(prev_calculated == 0)

{

int upto = rates_total - 1;

for(int i = 0; i <= upto; ++i)

{

ZeroBuffer[i] = EMPTY_VALUE;

ObBuffer[i] = EMPTY_VALUE;

OsBuffer[i] = EMPTY_VALUE;

MomBuffer[i] = EMPTY_VALUE;

MomColor[i] = 0.0;

}

}

// indices

int last_closed = rates_total - 2; // last closed bar

int bars_clamped = last_closed + 1; // working length for smoother

int min_index = 0; // include bar 0

// full recompute when needed

if(prev_calculated == 0 || g_last_committed_closed > last_closed || g_last_committed_closed < 0)

{

for(int i = last_closed; i >= min_index; --i)

compute_bar(bars_clamped, open, high, low, close, i, last_closed);

g_last_committed_closed = last_closed;

}

// new closed bars: update recent window and refresh bar 0

else if(last_closed > g_last_committed_closed)

{

int warm = MomentumLength + SmoothLength + DzLookBackBars + 5;

int first = MathMax(min_index, last_closed - warm);

for(int i = last_closed; i >= first; --i)

compute_bar(bars_clamped, open, high, low, close, i, last_closed);

compute_bar(bars_clamped, open, high, low, close, 0, last_closed);

g_last_committed_closed = last_closed;

}

// no new closed bars: keep history frozen, refresh bar 0 only

else

{

compute_bar(bars_clamped, open, high, low, close, 0, last_closed);

}

g_last_calc_ms = GetTickCount();

return(rates_total);

}

// rebuild closed history on chart re-scale or symbol/TF change

void FullRecomputeFromChart()

{

int bars_total = Bars(_Symbol, _Period);

if(bars_total < 2) return;

int last_closed = bars_total - 2;

int bars_clamped = last_closed + 1;

int min_index = 0;

MqlRates rates[];

int copied = CopyRates(_Symbol, _Period, 0, bars_clamped, rates);

if(copied < bars_clamped) return;

ArraySetAsSeries(rates, true);

static double o[], h[], l[], c[];

ArrayResize(o, bars_clamped); ArrayResize(h, bars_clamped);

ArrayResize(l, bars_clamped); ArrayResize(c, bars_clamped);

for(int i=0; i<bars_clamped; i++){ o[i]=rates[i].open; h[i]=rates[i].high; l[i]=rates[i].low; c[i]=rates[i].close; }

if(ArrayRange(wrk,0) != bars_clamped) ArrayResize(wrk, bars_clamped);

for(int i = last_closed; i >= min_index; --i)

compute_bar(bars_clamped, o, h, l, c, i, last_closed);

g_last_committed_closed = last_closed;

g_last_calc_ms = GetTickCount();

ChartRedraw();

}

// minimal event handlers

void OnChartEvent(const int id, const long &lparam, const double &dparam, const string &sparam)

{

if(id == CHARTEVENT_CHART_CHANGE)

{

g_skip_timer_until_ms = GetTickCount() + 1500;

FullRecomputeFromChart();

}

}

void OnTimer()

{

if(!UseTimerRecalc) return;

ChartRedraw();

}

void OnDeinit(const int reason)

{

if(UseTimerRecalc) EventKillTimer();

} Attached Image (click to enlarge)