When I develop a new automated Forex strategy, I run a backtest on the last few years and use Monte Carlo simulation to tune the lot size such that the maximum drawdown at the 98th-percentile is no more than 35%. This is just my arbitrary personal maximum risk tolerance before I start loosing sleep at night, so nothing magical about these numbers. To be able to scale this risk independent from my current capital or whatever starting balance I selected during backtesting, my EAs don't use a "LotSize" input parameter, but rather a "LotsPer1kEquity" input parameter. The above risk profile results in my EAs to use only between 2%-10% deposit load each when using a broker with high leverage. That enables me to safely run about 10 strategies in parallel on a single account.

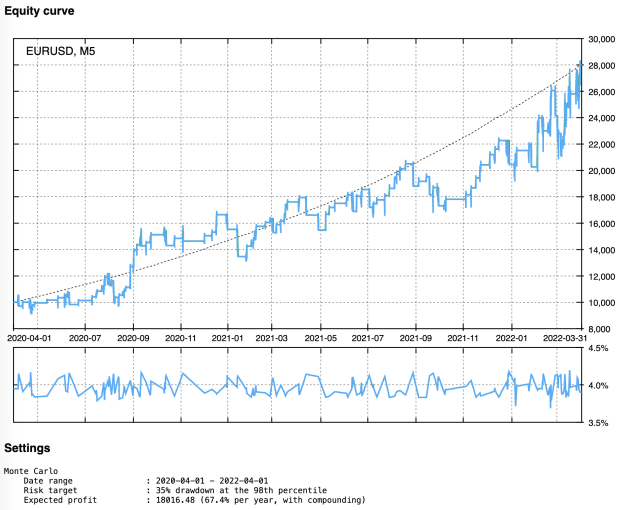

For example, this particular strategy uses 0.192 lots per 1k equity which is 4% deposit load at 1:500 leverage. The dotted line is the Monte Carlo estimate of 67.4% growth per year given the risk target of maximum 35% drawdown at the 98th-percentile.

While I feel the above is a solid scientific method for the initial sizing of the strategies in my portfolio, it does feel inadequate once a certain strategy starts to clearly loose money. Obviously, it is impossible to say if that is just a temporary drawdown or whether the strategy has lost it edge and should be abandoned.

I am seeking your advice and suggestions on how to keep the portfolio updated based on recent trading results.

- Should I just keep running the strategy at the initial risk allocation and only remove it from the portfolio in the unlikely event that it actually reached 35% drawdown? I know that theoretically there is only a 2% chance that the drawdown will be 35%, so once it reaches that, it is likely that it has lost its edge.

- Or should I continuously rescale all strategies in the portfolio based on recent results? What methodologies / algorithms exist?

Can you recommend certain literature? Or certain keywords I can search for on Google?

For example, this particular strategy uses 0.192 lots per 1k equity which is 4% deposit load at 1:500 leverage. The dotted line is the Monte Carlo estimate of 67.4% growth per year given the risk target of maximum 35% drawdown at the 98th-percentile.

Attached Image (click to enlarge)

I am seeking your advice and suggestions on how to keep the portfolio updated based on recent trading results.

- Should I just keep running the strategy at the initial risk allocation and only remove it from the portfolio in the unlikely event that it actually reached 35% drawdown? I know that theoretically there is only a 2% chance that the drawdown will be 35%, so once it reaches that, it is likely that it has lost its edge.

- Or should I continuously rescale all strategies in the portfolio based on recent results? What methodologies / algorithms exist?

Can you recommend certain literature? Or certain keywords I can search for on Google?