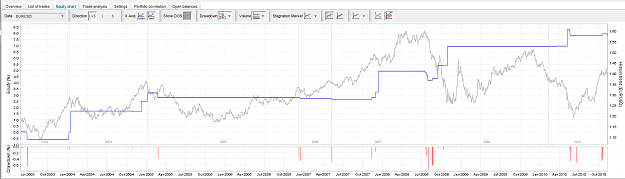

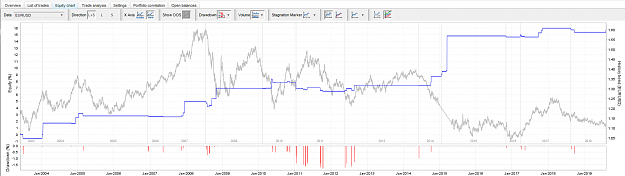

DislikedBack-testing - The Traditional Pitfall of Curve Fitting So we have run our backtest over a long term data range and we peer at our equity curve. The first thing that crosses our mind is, how do we reduce that drawdown and how do we lift the curve?.....and here enters the fickle world of curve fitting. What we do is choose an incremental adjustment to our variables and then run it again over the same data. As our equity curve is being reshaped into our liking what we often fail to realise is that we are adjusting our system design to best deal with...Ignored