So, you put these two ideas together, and when there's two CAD red-flag news items in a row, you get repetitious patterning, and one along, a temporary balance bar from which pivots happen. Like the single CAD reds, the two CAD reds work with each other to make a compound turn twice as far along the chart. Again, nothing to trade on, if smalltime; just a guide.

Two CAD reds paired on 0807 1400 and 1700 gmt+2, producing a news-laden middle with an incredibly repetitious pattern between the two CAD reds; in this instance, the entirety was a longterm pivot, so there was no division of a run or an eventual pivot from the both of them. 1,2,3,4,5.

Thus, it seems that each CAD red is reliable as a temporary balance-bar-type pivot, and when it hooks up with another CAD red, unusual, reasonably logical things happen to change the timing of this formula.

(The reasoning is that Canada is mostly a former Great Britain colony, and a fairly sedate pair with occasional jumps. I demo-traded the u/c half a year ago, while scouting around different pairs. What struck me immediately were the long level holds with significant jumps between them. And, look at this. I mean, I know it's the Asian and all, but they don't make runways so horizontal. So that sendentariness's gotta rub off on its mother country at the news intersection from, with g/u, CAD. And, for now, it seems it does.)

Also, I included JPY, because Asia is big. (Another Duh.) Switzerland is small. Australia is, land-wise, big, only the currency is obscure. New Zealand is small. Another reason, I guess, to include JPY is that it's a big oil importer, where CAD is a big oil exporter. (Yeah, right. THat's a reason.)

JPY doesn't have a lot of red-flag news items. They're at weird times, such as a few minutes after the hour instead of on the hour.

I did find a good pairing with CAD on 0811, 1019 and 1515 gmt+2, respectively. Made some good temporary hz's and derivatives, until US, GB news arrived.

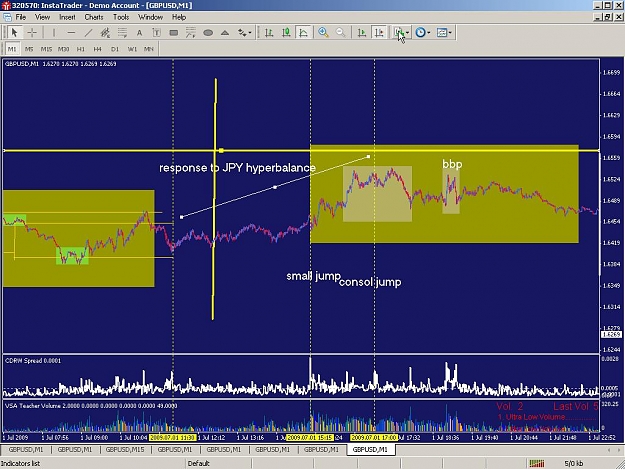

There's another interesting thing: JPY and the next prime news (USD, GB and EUR) item after it balance each other in a dip perfectly aligned, a little like two CAD reds in a row (1,2).

Just as there's a variety, to two CAD reds or a CAD and a main red, there is with JPY: In this example, a whole lot of pure jumping between widely-spread levels happened before this JPY news item on 0817 250gmt+2, and after a main news item. It seems that the further away the main news item before the JPY news is and, at the same time, the closer the next main news item is to the JPY news item, the simpler the dip pattern between the JPY and the next (main) news items.

Thus, with the rare variety, the gap pre-JPY was narrower than the one after. The post- gap lost its edge and never returned price until much later. Pic 1. JPY's level failed to balance price, and price fell precipitously (pic 2.) My new basing-patterns area method, discussed in 'EUR/USD Patterns' thread, would help decipher this unusual behavior; pic 3 shows the loosely-drawn hz's from those middle patterns. In pics 4 and 5, price returned to the JPY-next news item span levels (green dotted hz's included), producing an awaited fulfilling the usual of these two news items.

Get this -- This version within the JPY-main rule produced such an effect that it lasted another half-dozen screens! (Pics 6, 7, 8, 9, 10, 11 and 12.)

Recall that I've only studied two months of 1' TF data, so take the above rule with a very large grain of salt.

Okay, next I wanted to study why the main currencies' news items sometimes did well, and other times didn't.

Two CAD reds paired on 0807 1400 and 1700 gmt+2, producing a news-laden middle with an incredibly repetitious pattern between the two CAD reds; in this instance, the entirety was a longterm pivot, so there was no division of a run or an eventual pivot from the both of them. 1,2,3,4,5.

Thus, it seems that each CAD red is reliable as a temporary balance-bar-type pivot, and when it hooks up with another CAD red, unusual, reasonably logical things happen to change the timing of this formula.

(The reasoning is that Canada is mostly a former Great Britain colony, and a fairly sedate pair with occasional jumps. I demo-traded the u/c half a year ago, while scouting around different pairs. What struck me immediately were the long level holds with significant jumps between them. And, look at this. I mean, I know it's the Asian and all, but they don't make runways so horizontal. So that sendentariness's gotta rub off on its mother country at the news intersection from, with g/u, CAD. And, for now, it seems it does.)

Also, I included JPY, because Asia is big. (Another Duh.) Switzerland is small. Australia is, land-wise, big, only the currency is obscure. New Zealand is small. Another reason, I guess, to include JPY is that it's a big oil importer, where CAD is a big oil exporter. (Yeah, right. THat's a reason.)

JPY doesn't have a lot of red-flag news items. They're at weird times, such as a few minutes after the hour instead of on the hour.

I did find a good pairing with CAD on 0811, 1019 and 1515 gmt+2, respectively. Made some good temporary hz's and derivatives, until US, GB news arrived.

There's another interesting thing: JPY and the next prime news (USD, GB and EUR) item after it balance each other in a dip perfectly aligned, a little like two CAD reds in a row (1,2).

Just as there's a variety, to two CAD reds or a CAD and a main red, there is with JPY: In this example, a whole lot of pure jumping between widely-spread levels happened before this JPY news item on 0817 250gmt+2, and after a main news item. It seems that the further away the main news item before the JPY news is and, at the same time, the closer the next main news item is to the JPY news item, the simpler the dip pattern between the JPY and the next (main) news items.

Thus, with the rare variety, the gap pre-JPY was narrower than the one after. The post- gap lost its edge and never returned price until much later. Pic 1. JPY's level failed to balance price, and price fell precipitously (pic 2.) My new basing-patterns area method, discussed in 'EUR/USD Patterns' thread, would help decipher this unusual behavior; pic 3 shows the loosely-drawn hz's from those middle patterns. In pics 4 and 5, price returned to the JPY-next news item span levels (green dotted hz's included), producing an awaited fulfilling the usual of these two news items.

Get this -- This version within the JPY-main rule produced such an effect that it lasted another half-dozen screens! (Pics 6, 7, 8, 9, 10, 11 and 12.)

Recall that I've only studied two months of 1' TF data, so take the above rule with a very large grain of salt.

Okay, next I wanted to study why the main currencies' news items sometimes did well, and other times didn't.