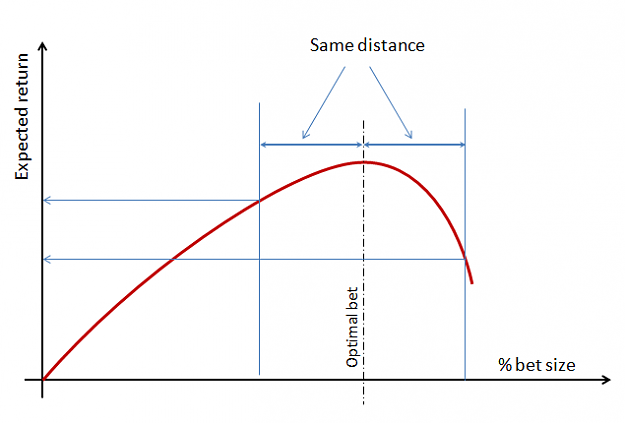

Disliked{quote} The increase of probability is a required yet not sufficient condition. The optimal bet size of a system can be calculated from a choosen utility function, based on personal risk aversion. The most known example is the log return which leads to the Kelly bet size. If you don't know the characteristics of your system, i.e. its winrate and R:R and their associated confidence intervals, such a function still exist. You simply dont know it. If you look at the Kelly curve you notice that it drops more sharply after the optimal point (too big...Ignored

That doesnt necessarly have to be in 1 session,and doesnt necessarly have to blow your account. 0.64 lot size on a 100-200 $ startick pack is not a relatively huge risk.If we scalp small pieces of a candle when the probability of its reversal is good, we could theoretically get an edge if the spread & slippage is good.That would provide us a 55 or so permanent winrate (theoretically) and if its from 1 to 20 pips size with 1:1 RR of course, a 0.64 lot size loss would be only max ~12$ on a 5 decimal broker.

QuoteDislikedQuote

we still avoid the losing strikes more efficiently with martingale

Not correct. Your probability of winning is independent of the betting size.

Not with the martingale, since we are talking about relative loss.What you count loss here, we must define the word "loss" in the martingale context, the actual trade that was gone negative? Or the actual loss after we ran out of levels , ie we reached the 8 losses in a row, since i was talking about lot^7 system.

So of course if we imagine the market as a 50-50 system and apply martingale to it it wont change the actual/individual outcome of the trade so you are partially correct.

But with marty we are not interested in the individual outcome of the trade, but rather that our doubling series will end in a win or a lose.

And for that my friend, (given that you say that the bets are independent from eachother) we can use hannover's nice binomial distribution table to find out.

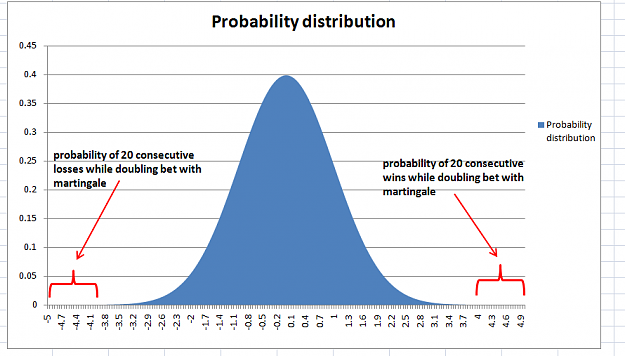

So,lets take 100 trades for example.We will only trade 100 trades in a set, now since we only lose at 8 losses in a row, so thats the only loss that we are interested in.We have a 31% of getting an 8 times a row loss, which is the real loss, not the hedged ones, which will result, in our case in a LOT^7 loss which in our case (given that we start with 100$ and our initial lot size is 0.01 with a 5 decimal broker) we only lose 12$

So we have a 12$ loss with a 31% probability in 100 trades while we got a 69% probability that the other trades will end in a hedged loss (anything below LOT^7), OR an initial win.And since each real loss will deplete 8 trades the probability now becomes dependent of the outcomes of the row, and continuous.So the next trade since we depleted 8 trades will only have 92 trades left to run so the distribution will now be different.

"There's a sucker born every minute" - P.T. Barnum