It has scientifically been estimated that it takes 10 000 hours (4 years, 8 hours a day) to get really good at anything.

Hazard: No risk, no return

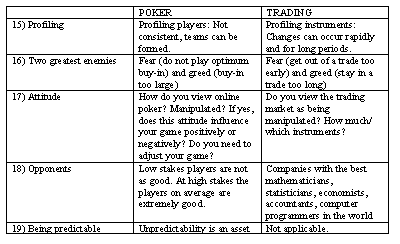

Attachment: Table 1.png

Attachment: Table 2.png

Step 1: Find your niche (i.e. best winning situation form above). If you cannot win at your niche, you will lose at any other combination. A niche is some combination of the above which gives you the best chance of success. Take note: We are not even talking about your method of playing / trading employed.

Step 2: Money Management. One of the hidden purposes of proper money management is to give you an indication over time if you can play and win at your ‘niche’ game. If you cannot, then money management will not save you, it will just prolong the inevitable.

The purpose of money management is also to calculate the optimum amount you should take from your bankroll to a table/tournament. The optimal amount is the amount which will let your bankroll grow the fastest with a given level of risk. I.e. pros know some of them only have a maximum of 2% advantage over another pro. This means there is a huge level of risk of luck involved most of the time.

Chris Ferguson suggests, as a rule of thumb, to take only 5% of your bankroll to a cash game or a sit and go. He also suggest, as a rule of thumb, to only take 2% of your bankroll to a multitable tournament. Chris Ferguson’s estimates are very close to calculations done by traders and mathematicians on calculating the optimum amount to the market/tables for the quickest reward taking into account the risk associated with bad luck streaks.

Discipline means sticking to Step 2.

Mathematics of Kelly Criteria

(for calculating optimal risk taking into account reward/risk)

1) Trading example:

Our probability of winning each time is 60%. Thus Win probability is 0,6. Each time we win we get 150% of our trade size. Every time we lose, we lose 100% of our trade size. This gives a win/loss ratio of 1,5. Then, use the formula:

K=W-((1-W)/(w/l))

where W is the percentage of wins (i.e. Win probability), w is the average dollar win and l is the average dollar loss (i.e. win/loss ratio).

As in your optimal f calculation:

0.6 -((1-0.6)/(1.5/1)) = .33

Now, trade 33% of your bankroll (i.e. R33 333 of a R100 000 bankroll) on a trade that has a probability of 60% and a return of 150% for each winning trade.

2) Poker example (tournament play):

180 entrants, you assume you are better than average. You assume you have 1/33 chance of winning the tournament, i.e. 3,0%. If you win you will get 25% of the total winnings. That means 45 times your buy-in. We ignore getting in the money and for this example view ‘getting in the money’ as just a bonus.

Calculating the Kelly value, you get that you must put only 1% of your bankroll on the line in each tournament.

Remember, the 1/33 chance needs to be established first. This can quite some time before you have a ‘true’ approximation. Else, you must make the approximation by estimation and feel. The more accurate you can estimate your chances, the more accurate answer the Kelly criterion will provide.

As you will find out by putting different values in the Kelly Value is that if the Kelly value < 0 it means you cannot win over the long term and your ‘niche’ game is not good enough. You will have to change your style/method or stop. Try it for roulette calculations and you should get a negative value (not taking card counting into account of cause).

Please comment on this, I am sure we can improve on these initial thoughts.

Add-on:

“A contrarian investor focuses not only on the general sentiment, but more

importantly on how that sentiment can lead to disconnects between the

fundamentals and market expectations.

“To continue with the horse- racing theme … Steven Crist, for many years the

New York Times reporter covering horse racing, contributed a chapter to a book

called Bet with the Best in which he wrote: ‘The issue is not which horse is the

most likely winner, but which horse is offering odds that exceed its chance of

victory …. This may sound elementary, and many players may think that they are

following this principle, but in truth few actually do. Under this mind- set,

everything but the odds fades from view. There is no such thing as “liking” a

horse to win a race, only an attractive discrepancy between his chances and his

price.’ The successful hedge fund manager, Michael Steinhardt, shared a very

similar view in his autobiography, when he wrote: ‘I defined variant perception as

holding a well-founded view that was meaningfully different from the market

consensus …. Understanding market expectation was at least as important as,

and often different from, the fundamental knowledge.’

“Now ask yourself, honestly, how clearly do you distinguish between

fundamentals and expectations? If you’re like most people, not very clearly.

“Psychologist Robert Zajonc, sums it up pretty well when he says: ‘We

sometimes delude ourselves that we proceed in a rational manner and weigh all

of the pros and cons of various alternatives. But this is seldom the case. Quite

often “I decided in favour of X” is no more than “I liked X”.… We buy the cars we

“like”, choose the jobs and houses we find “attractive”, and then justify these

choices by various reasons. Moreover, what we like is heavily influenced by what

other people like. Successful contrarian investing isn’t about going against the

grain per se, it’s about exploiting expectation gaps.”

Hazard: No risk, no return

Attachment: Table 1.png

Attachment: Table 2.png

Step 1: Find your niche (i.e. best winning situation form above). If you cannot win at your niche, you will lose at any other combination. A niche is some combination of the above which gives you the best chance of success. Take note: We are not even talking about your method of playing / trading employed.

Step 2: Money Management. One of the hidden purposes of proper money management is to give you an indication over time if you can play and win at your ‘niche’ game. If you cannot, then money management will not save you, it will just prolong the inevitable.

The purpose of money management is also to calculate the optimum amount you should take from your bankroll to a table/tournament. The optimal amount is the amount which will let your bankroll grow the fastest with a given level of risk. I.e. pros know some of them only have a maximum of 2% advantage over another pro. This means there is a huge level of risk of luck involved most of the time.

Chris Ferguson suggests, as a rule of thumb, to take only 5% of your bankroll to a cash game or a sit and go. He also suggest, as a rule of thumb, to only take 2% of your bankroll to a multitable tournament. Chris Ferguson’s estimates are very close to calculations done by traders and mathematicians on calculating the optimum amount to the market/tables for the quickest reward taking into account the risk associated with bad luck streaks.

Discipline means sticking to Step 2.

Mathematics of Kelly Criteria

(for calculating optimal risk taking into account reward/risk)

1) Trading example:

Our probability of winning each time is 60%. Thus Win probability is 0,6. Each time we win we get 150% of our trade size. Every time we lose, we lose 100% of our trade size. This gives a win/loss ratio of 1,5. Then, use the formula:

K=W-((1-W)/(w/l))

where W is the percentage of wins (i.e. Win probability), w is the average dollar win and l is the average dollar loss (i.e. win/loss ratio).

As in your optimal f calculation:

0.6 -((1-0.6)/(1.5/1)) = .33

Now, trade 33% of your bankroll (i.e. R33 333 of a R100 000 bankroll) on a trade that has a probability of 60% and a return of 150% for each winning trade.

2) Poker example (tournament play):

180 entrants, you assume you are better than average. You assume you have 1/33 chance of winning the tournament, i.e. 3,0%. If you win you will get 25% of the total winnings. That means 45 times your buy-in. We ignore getting in the money and for this example view ‘getting in the money’ as just a bonus.

Calculating the Kelly value, you get that you must put only 1% of your bankroll on the line in each tournament.

Remember, the 1/33 chance needs to be established first. This can quite some time before you have a ‘true’ approximation. Else, you must make the approximation by estimation and feel. The more accurate you can estimate your chances, the more accurate answer the Kelly criterion will provide.

As you will find out by putting different values in the Kelly Value is that if the Kelly value < 0 it means you cannot win over the long term and your ‘niche’ game is not good enough. You will have to change your style/method or stop. Try it for roulette calculations and you should get a negative value (not taking card counting into account of cause).

Please comment on this, I am sure we can improve on these initial thoughts.

Add-on:

“A contrarian investor focuses not only on the general sentiment, but more

importantly on how that sentiment can lead to disconnects between the

fundamentals and market expectations.

“To continue with the horse- racing theme … Steven Crist, for many years the

New York Times reporter covering horse racing, contributed a chapter to a book

called Bet with the Best in which he wrote: ‘The issue is not which horse is the

most likely winner, but which horse is offering odds that exceed its chance of

victory …. This may sound elementary, and many players may think that they are

following this principle, but in truth few actually do. Under this mind- set,

everything but the odds fades from view. There is no such thing as “liking” a

horse to win a race, only an attractive discrepancy between his chances and his

price.’ The successful hedge fund manager, Michael Steinhardt, shared a very

similar view in his autobiography, when he wrote: ‘I defined variant perception as

holding a well-founded view that was meaningfully different from the market

consensus …. Understanding market expectation was at least as important as,

and often different from, the fundamental knowledge.’

“Now ask yourself, honestly, how clearly do you distinguish between

fundamentals and expectations? If you’re like most people, not very clearly.

“Psychologist Robert Zajonc, sums it up pretty well when he says: ‘We

sometimes delude ourselves that we proceed in a rational manner and weigh all

of the pros and cons of various alternatives. But this is seldom the case. Quite

often “I decided in favour of X” is no more than “I liked X”.… We buy the cars we

“like”, choose the jobs and houses we find “attractive”, and then justify these

choices by various reasons. Moreover, what we like is heavily influenced by what

other people like. Successful contrarian investing isn’t about going against the

grain per se, it’s about exploiting expectation gaps.”

Attached Images