DislikedThe second time this year we trade an NFP that the FED has tied serious, direct implications behind. The last time (7 August.) the number was a slight +-10k miss(215, 222 expected.) but I saw it as strong enough for the FED's worded criteria (some further improvement...Ignored

--> We may get a dead cat bounce to the 1.12xx handle (technically the 1.14xx is still v marginally open as for today). Despite the surprising numbers today most serious forecast are aligned for a bit softer/inline core US numbers (inflation/employment) these coming weeks. However, the trigger for the mid term leg may come from the euro side (ECB) not necessarily from the dollar (FED).

--> Markets rate and 'trust' the ECB a lot more than the FED since Yellen took over. At the same time the ECB has always "put the money where the mouth is" and the last massive game changer (last ECB conference) is weighing heavily across the board (equities rallied in manic mode and euro buyers vanished from all fronts).

--> A flop in German numbers next week will be enough to guarantee ECB going all in December but more importantly the board is aligning in favour of equites (surprise surprise the bastards are going to make a killer year).

--> A ECB QE + rate cuts will perfectly allow the FED to hike DEC too as it will offset most of the hike impact leaving equities pretty much 'unch' (wide chop zone) while buffering the short term 'tsunami' in dollar and in particular EURO (it will get hit in both fronts) .

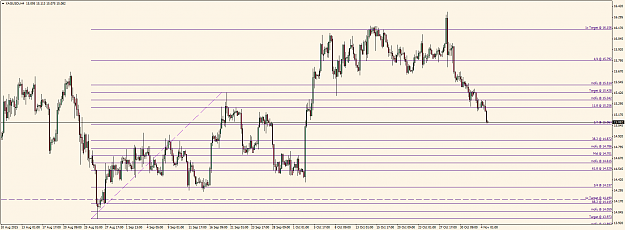

Whatever the case, the perfect storm is aligning in the Euro...

sisse

Pending conversations? PM for a chat...I am mainly in OTM now