The results you see on this post use the same trailing stop and machine learning mechanism as before only that this time we use 17 bars from the GBPUSD and 17 bars from the EURUSD for each example used in training

Ignored

ATJ, Is it an ensemble of two models one for EU and the other for GU? If not, how do you use data from different assets using F4? which input / output functions do you use?

Thanks

Ruby

It took some time to read the whole thread but it was time well spent.

Over past few years I worked with NN, SVM, fuzzy logic, ensembles etc.

I am very glad that I found people that do more or less the same type of algo trading as me.

There are few differences however:

- I do it for futures and stocks

- now I use SVM binary classification

- I use Amibroker, my own dll as a plugin(C++), libsvm

- I use a lot more inputs and samples to train classifiers

- to verify system parameters I did Walk-Forward (knowing about all the limitations)

At first I was very sceptical about number of inputs and samples you use - I thought so little information cannot give you enough power to predict outcome whatever it is (next bar bullish/bearish, crossing atr etc)

Inspired by this thread (by results of backtesting) right now I am trying to test your assumptions.

In few hours I will have some results - but I do not know if it is allowed to post results for futures/different software etc.

Just let me know.

I am not very familiar with Metatrader/Ashirukuy platform - so few questions regarding:

- are all numbers on attached pictures in absolute values ? eg. Cumulative return=50 means 50 * 100% ?

- what are "starting" values - initial equity, leverage, spread or commisions included ?

- do you backtest with fixed position size ?

And regarding DMB:

- how would you estimate number of "random tickers" to generate from original data to test DBM

Now I have search space of 112 parameters - it takes 2h to train and test (15 years, EOD) in case of 100 "random tickers" it would lead to 2 weeks

Now I have search space of 112 parameters - it takes 2h to train and test (15 years, EOD) in case of 100 "random tickers" it would lead to 2 weeks That's it for now - good luck Special thanks to algoTraderJo, PipMeUp, KaBo

{quote} ATJ, Is it an ensemble of two models one for EU and the other for GU? If not, how do you use data from different assets using F4? which input / output functions do you use? Thanks Ruby

Ignored

It's not an ensemble, in this example I am making predictions using rates from two different symbols on the input/output function. None of the functions that come with the F4 framework can do this, but you can modify them to do so if you wish. I'll show you how you can do these modifications to run a test with EURUSD and GBPUSD. The first thing you should do is load rates for another symbol on your rates. If you have these rate reqs:

Inserted Code

rateRequirements = 8000

symbolRequirements = D

timeframeRequirements = 0

change them to this (change GBPUSD to GBPUSD1987 if you are using that set):

See how I also changed from cOpen to iOpen so that I could include the returns from the GBP/USD. When you do this you will have functions that work with return values from two different pairs to train and make predictions. Easy-peasy.

It took some time to read the whole thread but it was time well spent. Over past few years I worked with NN, SVM, fuzzy logic, ensembles etc. I am very glad that I found people that do more or less the same type of algo trading as me. There are few differences however: - I do it for futures and stocks - now I use SVM binary classification - I use Amibroker, my own dll as a plugin(C++), libsvm - I use a lot more inputs and samples to train classifiers - to verify system parameters I did Walk-Forward (knowing about all the limitations) At first I...

Ignored

You can post results for anything you want. Just try to be clear in what software you used and what markets/instruments are involved. To answer what you asked:

Yes, all number are in absolute values. A value of 50 means a 50*100% total return.

Initial equity 100,000 USD, max leverage is 1:50. Spreads are included but depend on the symbol. EURUSD=0.0003, GBPUSD=0.0005, USDJPY=0.03, EURJPY=0.05, GBPJPY=0.07. In practice I could backtest with 1000 USD and obtain the exact same result if I wanted to, since the Oanda min lot size is 0.00001 lots I have no problem with low starting equity values.

Sizing is not constant it's adjusted depending on the SL value such that a fixed % (generally 1%) is lost if the SL is triggered. Position size is adjusted to make the risk per trade a constant % of the account balance at the moment of trade entry.

You cannot estimate IMHO, you need to run as many as needed so that the distribution of average results on random time series converges. Once adding more results from random series causes no changes, you can say you're done. The number will change depending on how much data you have, the nature of your system, etc. And yes, it's a lot of computer time.

{quote} You can post results for anything you want. ...

Ignored

I tested following combinations:

Number of samples: 20 .. 240 (step 20)

Inputs:

past 5 daily bars as

- continues values (Close-Open)/Open scaled

- binary: -1 for bearish +1 for bullish

- binary: -1 for bearish +1 for bullish with some threshold for small movements (those are set as 0)

Targets:

next day

- binary: -1 for bearish +1 for bullish

- binary: -1 for bearish +1 for bullish with some threshold for small movements (those are set as 0)

The best system I got for FW20WS (future contract for polish WIG20 index):

CAR = 4%

MaxDD = -13%

Sharpe = 1.02

Attached Image (click to enlarge)

Attached Image (click to enlarge)

So next step is trying the same idea for forex - could you share what was the best system so far ?

- what inputs and targets

- number of samples

- timeframe

- pair

Good morning, I am going to join you. I am going to start (just for fun) a project by developing a TS based on NN.

Of course I am already worried about few issues that my choices are going to face:

In particular I would like to build a Dynamic Neural network based on outputs (feedback) data.

The main problem for me will be to avoid the overfitting. For that I would like some advices from you?

I hope within this week to set up something in a demo account to start to evaluate this kind of solution.

I ll keep you updated and I ll follow closely this topic.

... In particular I would like to build a Dynamic Neural network based on outputs (feedback) data. The main problem for me will be to avoid the overfitting. ....

Ignored

To avoid overfitting NN you need to

- use as little neurons as possible

- use as many samples as possible

- use early stopping when RMSE/MSE is not that low

- use validation set and stop learning when error (for validation set) is lowest

Not exactly sure what dynamic nn is - is it same/similar to recursive/Elman/time delayed NN ?

Inputs?

This is one of the fundamental aspects of building a NN.

Which according to your experience are the Inputs necessary for good NN perfomance?

I know it's a very generic question. Although I would like to know for instance if technical indicators are useful?

After reading this thread I come to one simple conclusion: It's not real time testable.

Because of the possible long drawn down time (like 6months or better) and due to daily TF and little number of trades it's very difficult to asses if we really make money or just being fooled by variance of outcome. On the other hand the number of training bars is very low so its guarantee very high variance of prediction.

So my question is: Is anybody able to present system on TF like 1H or lower trained on like 5k-20k bars which will generate more trades and will be real time testable ??

{quote} Not exactly sure what dynamic nn is - is it same/similar to recursive/Elman/time delayed NN ?

Ignored

About recurrent neural networks... in my opinion they could be the way to go.

Classic MLP networks don't account for the input geometry.

Convolutional neural networks (CNN) exploit local correlations, but they are invariant to translation and they don't really account for the sequentiality of time series data.

Theoretically, a recurrent neural network such as LSTM, GRU or ESN seems like the best solution if you use a time series as input.

Hi, After reading this thread I come to one simple conclusion: It's not real time testable. Because of the possible long drawn down time (like 6months or better) and due to daily TF and little number of trades it's very difficult to asses if we really make money or just being fooled by variance of outcome. On the other hand the number of training bars is very low so its guarantee very high variance of prediction. So my question is: Is anybody able to present system on TF like 1H or lower trained on like 5k-20k bars which will generate more trades...

Ignored

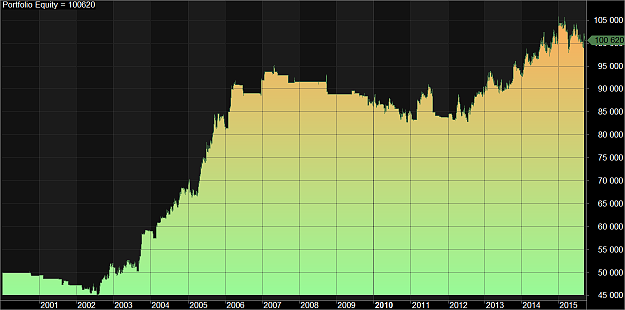

There is a plethora of H1 systems within this thread; in fact, the majority of systems do not trade on the daily timeframe.

Look at the recent post (#720) which provides an M30 system. In my opinion, this is about as good as a backtest can be - a constantly evolving (retraining) algorithm tested over 28.7 years on the M30 timeframe, using a professional development framework (that takes into account historical swaps etc) and uses very high quality historical data (if it is the data that is bundled with the framework, then it is from a source which provides quotes to a variety of different brokers, and is not usually available to the general public). With the way that the framework implements time refactoring, this amounts to roughly 334300 bars. As you start to explore the 15 minute timeframe and below, it becomes difficult to conduct accurate OHLC simulations, thus necessitating the use of tick-by-tick simulations. However, you then run into two problems with regards to machine learning system development: 1.) It is extremely expensive (if not impossible) to acquire tick data which goes back as far as 1987, and 2.) The computation of constantly retraining ML algorithms becomes prohibitively expensive for retail traders. This is why I believe that backtests on the H1, M30 (or perhaps M15) timeframe across 28.7 years, such as the ones within this thread, are necessary in order to reduce curve-fitting bias as much as possible. By then measuring data-mining bias, as described in this thread also, we are able to gain further confidence in the results of our backtests.

In response to your comment about 6 month drawdowns, this is to be expected when conducting backtests over such a long period of time - if you were to backtest over 10 years for example, then would a 6 / 2.87 ≈ 2-month drawdown seem more acceptable? Don't forget that although the systems in this thread may have a 'long' maximum drawdown duration, they are all highly linear (correlation coefficient of the returns is >= 0.95, or in a lot of cases, >= 0.99) over a substantial period of time. This property of these ML systems is a very significant and strong one - these systems are able to survive (and profit from) an enormous array of market conditions.

{quote} There is a plethora of H1 systems within this thread; in fact, the majority of systems do not trade on the daily timeframe. Look at the recent post (#720) which provides an M30 system. In my opinion, this is about as good as a backtest can be - a constantly evolving (retraining) algorithm tested over 28.7 years on the M30 timeframe, using a professional development framework (that takes into account historical swaps etc) and uses very high quality historical data (if it is the data that is bundled with the framework, then it is from a source...

Ignored

Can you generate the trades of this system and post it together with the currency data ?? I will try to reproduce it.

Can you generate the trades of this system and post it together with the currency data ?? I will try to reproduce it. Krzysztof

Ignored

I am not allowed to post the currency data, as it is licensed to paid members only.

Unfortunately I do not have the code for the system, and I don't have the time to code it myself at the moment. algoTraderJo may be kind enough to provide the trade list once he returns to the thread.