@GoldTheHun, thanks for your explanation.

@ezcurrency, thank you. You propose a predictive model. I don't judge if it is good or not (didn't check). Actually I expected a more qualitative answer. Something like "I would go long because the next bar is big and green. The lower wick is short. I could have entered with a small SL and take nice pips in a single day. Should I went short I would have made much more pips, sure, but the SL would be much bigger and the pips per day much less."

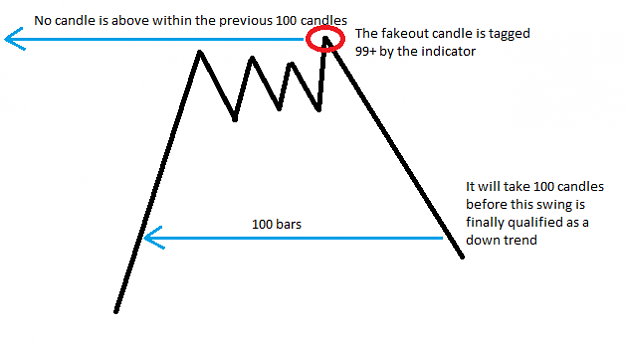

The goal is to infer the statistic rules you propose. Not to predict where the market will go the next X bars but rather to predict what an "omniscient trader" (who can see the future) would have done. In this example for instance the holding period is 1 day. But for the next bar the "perfect" holding period is 13 days. Unless you want to go long the two little green bars.

I limit myself to label the bars, I limit the decision at the bar close. Because of the huge number of bars I can't label them by hand. I need a way to label them automatically but also precisely. The ultimate goal is the get an algo that can learn reading the PA. A funny little project ;-)

Unfortunately the labelling I use for now is too simplistic. I need to somehow include the cost of being wrong. But due to the fact that the perfect trader knows the next bars he takes no risk: the algo tends to take profit early and pick all the possible tops and bottoms. I think it comes from the fact that nothing looks more like a trend bottom than all the lower lows before it. It can't learn that following the trend is safer. Perhaps I should include the perfect SL/TP in the labels...

@ezcurrency, thank you. You propose a predictive model. I don't judge if it is good or not (didn't check). Actually I expected a more qualitative answer. Something like "I would go long because the next bar is big and green. The lower wick is short. I could have entered with a small SL and take nice pips in a single day. Should I went short I would have made much more pips, sure, but the SL would be much bigger and the pips per day much less."

The goal is to infer the statistic rules you propose. Not to predict where the market will go the next X bars but rather to predict what an "omniscient trader" (who can see the future) would have done. In this example for instance the holding period is 1 day. But for the next bar the "perfect" holding period is 13 days. Unless you want to go long the two little green bars.

I limit myself to label the bars, I limit the decision at the bar close. Because of the huge number of bars I can't label them by hand. I need a way to label them automatically but also precisely. The ultimate goal is the get an algo that can learn reading the PA. A funny little project ;-)

Unfortunately the labelling I use for now is too simplistic. I need to somehow include the cost of being wrong. But due to the fact that the perfect trader knows the next bars he takes no risk: the algo tends to take profit early and pick all the possible tops and bottoms. I think it comes from the fact that nothing looks more like a trend bottom than all the lower lows before it. It can't learn that following the trend is safer. Perhaps I should include the perfect SL/TP in the labels...

No greed. No fear. Just maths.