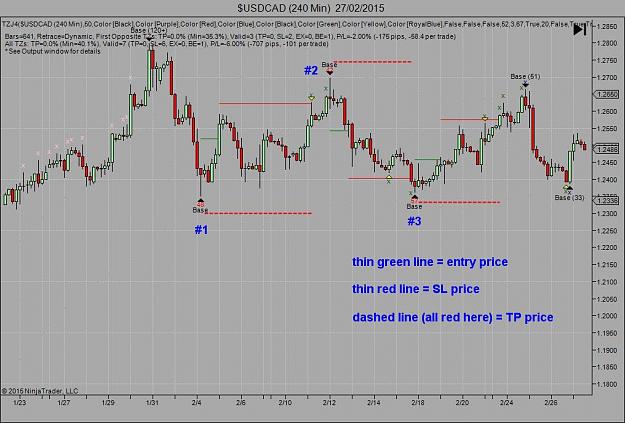

Setting stops to break even

You know, I've often wondered about the effectiveness of setting your stop to break even (or thereabouts) once a trade has started moving in your favour. On the one hand, it's very frustrating to be stopped out by a few pips, and then watch price reverse and eventually hit TP without you. I'm sure that's happened to all of us at some point! But on the other hand, a stop at BE (break even) means you've got nothing to lose, and if you can handle the frustration then your P/L might benefit in the long run.

So, I've programmed a crude stop adjustment parameter into the analysis indicator, just to get a feel for how this will affect P/L over the long term. I've been careful to avoid ambiguities in the code (such as price hitting BE and TP on the same bar). I then optimised the parameter for P/L.

The parameter indicates the % between entry and TP that price must close at or beyond in order to move the SL to BE. So, if you enter at 1.20, TP is at 1.21, and the parameter is set to 70%, then as soon as a bar closes with closing price >= 1.207 (70% between 1.20 and 1.21), then the stop is moved to BE (1.20).

To cut a long story short, the sweet spot for this parameter on M240 bars is in the 50-70% range (for the First Opposite TZ system). Here is the P/L for the 60% setting, expressed as a percentage of initial account balance if initially risking 1% per trade, for 9 pairs since Jan-2008. All other parameters set as before:

+44% for First TZs

+115% for All TZs

The number of trades is the same as before, but of course there are more SLs and less TPs. The TP rate is now 37.4% to 51.2% (depending on the pair).

Of course this is just a crude test and in reality you probably wouldn't move your stop only once, nor to exactly BE. As always, it depends on the conditions at the time. But it's interesting how even this crude method boosts performance in the long run from 86% to 115% for 1429 trades.

Next up: dynamic TPs!

You know, I've often wondered about the effectiveness of setting your stop to break even (or thereabouts) once a trade has started moving in your favour. On the one hand, it's very frustrating to be stopped out by a few pips, and then watch price reverse and eventually hit TP without you. I'm sure that's happened to all of us at some point! But on the other hand, a stop at BE (break even) means you've got nothing to lose, and if you can handle the frustration then your P/L might benefit in the long run.

So, I've programmed a crude stop adjustment parameter into the analysis indicator, just to get a feel for how this will affect P/L over the long term. I've been careful to avoid ambiguities in the code (such as price hitting BE and TP on the same bar). I then optimised the parameter for P/L.

The parameter indicates the % between entry and TP that price must close at or beyond in order to move the SL to BE. So, if you enter at 1.20, TP is at 1.21, and the parameter is set to 70%, then as soon as a bar closes with closing price >= 1.207 (70% between 1.20 and 1.21), then the stop is moved to BE (1.20).

To cut a long story short, the sweet spot for this parameter on M240 bars is in the 50-70% range (for the First Opposite TZ system). Here is the P/L for the 60% setting, expressed as a percentage of initial account balance if initially risking 1% per trade, for 9 pairs since Jan-2008. All other parameters set as before:

+44% for First TZs

+115% for All TZs

The number of trades is the same as before, but of course there are more SLs and less TPs. The TP rate is now 37.4% to 51.2% (depending on the pair).

Of course this is just a crude test and in reality you probably wouldn't move your stop only once, nor to exactly BE. As always, it depends on the conditions at the time. But it's interesting how even this crude method boosts performance in the long run from 86% to 115% for 1429 trades.

Next up: dynamic TPs!

You reap what you sow.