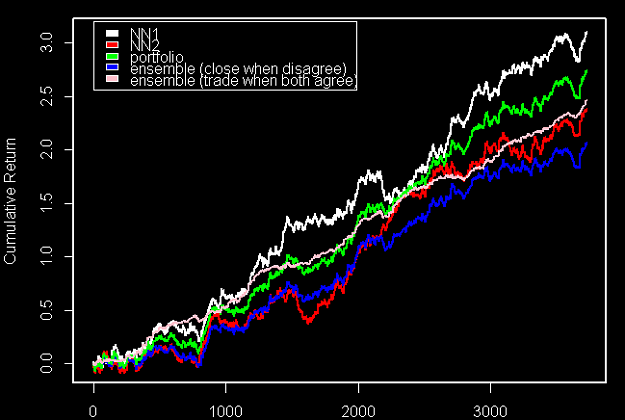

Disliked{quote} Yes, thats right if what I was saying was true, then any ensembles wouldn't work because of that. What I think now, is that an ensembles in this case wouldn't work because both NN are constructed the same way, so if there is a behaviour of the series that can't be capture by the NN structure, both NN will miss that in their forecast and could have bad trading results in the same time. I think that an "ideal" ensembles will be one that when NN1 get losses then NN2 take profits, what I wouldn't prefer is that both neural networks get losses....Ignored

There is a much stronger reason why the before showed ensemble does not give good results. Think about how the two models trade and what changes when you trade in an ensemble. There is a very fundamental change in trading behavior between an ensemble and the separate models that does not happen in a portfolio. Do experiments, ask questions, I'll try to guide you as well as I can.