Hello,

I would like to develop a trading algorithm that is consistent with the random walk hypothesis; in order to do this, we must assume market fluctuations are fundamentally unpredictable.

A successful system that makes this assumption would be profitable under virtually every condition in the market since the market direction becomes irrelevant. In addition, this profitability would exist regardless of whether the assumption was true (but the same cannot be said about systems that rely on market prediction).

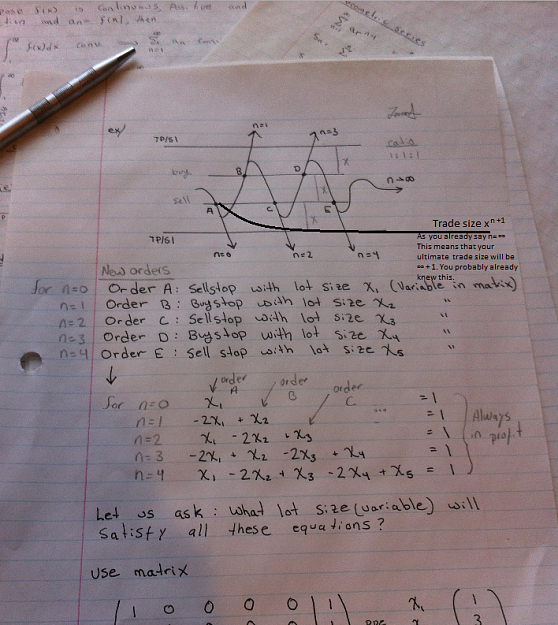

Furthermore, an approach of this kind would allow us to simplify trading to the point where we should be able to quantify all the possible actions of a trader. This is because, if we assume market fluctuations are purely random, it becomes easy to ignore trading strategies that depend on technical/fundamental analysis and thus, trading simply becomes a combination of various operations (buy/sell) and techniques (such as hedging).

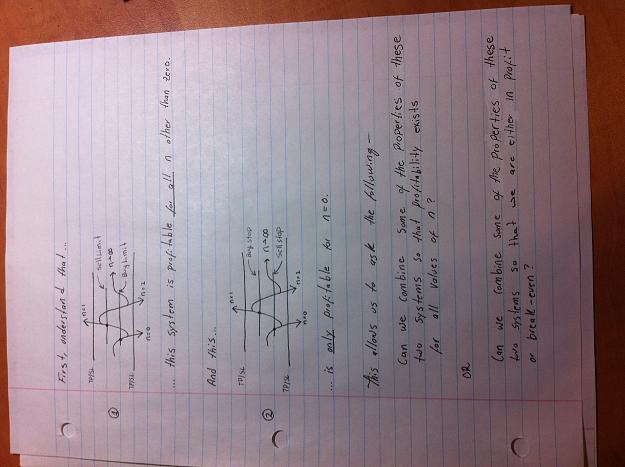

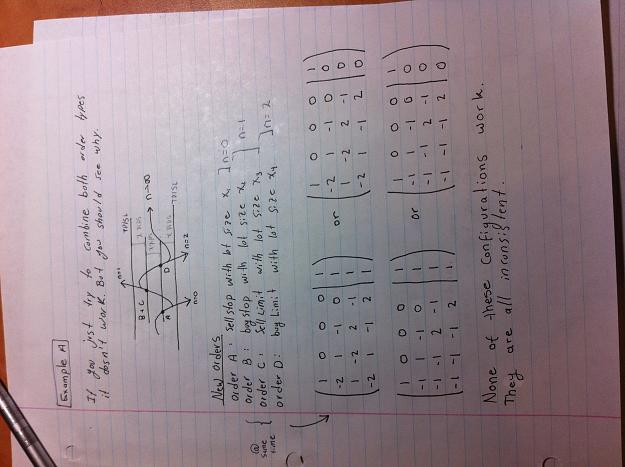

If all the actions of a trader can be reduced to a finite set of elements, it is reasonable to wonder if one could analyze the profitability of all possible configurations of these elements. An analysis of this kind would be a very efficient way to assess the profitability of nearly every possible trading system (we would no longer need to waste time mindlessly searching for an optimal strategy/Holy Grail).

For instance, one should be able to systematically evaluate the profitability of all possible combinations of trading strategies through a series of mass computations involving multiple large/sparse systems of linear equations.

I won’t go into much detail at the moment-- but I would like to know if anyone in this community is aware of such an analysis? Has research in this area ever been attempted? If not, would anyone else be interested in investigating this topic?

Thanks!

I would like to develop a trading algorithm that is consistent with the random walk hypothesis; in order to do this, we must assume market fluctuations are fundamentally unpredictable.

A successful system that makes this assumption would be profitable under virtually every condition in the market since the market direction becomes irrelevant. In addition, this profitability would exist regardless of whether the assumption was true (but the same cannot be said about systems that rely on market prediction).

Furthermore, an approach of this kind would allow us to simplify trading to the point where we should be able to quantify all the possible actions of a trader. This is because, if we assume market fluctuations are purely random, it becomes easy to ignore trading strategies that depend on technical/fundamental analysis and thus, trading simply becomes a combination of various operations (buy/sell) and techniques (such as hedging).

If all the actions of a trader can be reduced to a finite set of elements, it is reasonable to wonder if one could analyze the profitability of all possible configurations of these elements. An analysis of this kind would be a very efficient way to assess the profitability of nearly every possible trading system (we would no longer need to waste time mindlessly searching for an optimal strategy/Holy Grail).

For instance, one should be able to systematically evaluate the profitability of all possible combinations of trading strategies through a series of mass computations involving multiple large/sparse systems of linear equations.

I won’t go into much detail at the moment-- but I would like to know if anyone in this community is aware of such an analysis? Has research in this area ever been attempted? If not, would anyone else be interested in investigating this topic?

Thanks!

"What glory would attend the discovery..."