{quote} How important is the choice of the distance (metric) is nearest neighbor? L1, L2, L∞, Mahalanobis.... Do you have a preference?

Ignored

Can be very important or not so important, depending on your problem, in my experience at least (it might not be a general conclusion). As you have done I regularly use Euclidean distance (simplest to implement) where this doesn't work the problem can be more complex, you might want to look into similarity learning. However I think the problem might be getting too complicated (without need to be), you can probably achieve things with much simpler modeling if you change to more favorable inputs.

{quote} Well, machine learning methods find relationships that might not be obvious enough to be found through a more transparent method (like those you suggest).

Ignored

Could you please provide an example of this?

Something simple would suffice.

k

Joined Jan 2011

|

Status: Currently in Asia

|839 Posts

I am also interested in machine learning and I have read probably almost all accessible papers on NN and SVM implementation for financial predictions. Just a heads up, a lot of papers are written about prediction of indices and me trying to apply the same system in a forex environment lead to poor results.

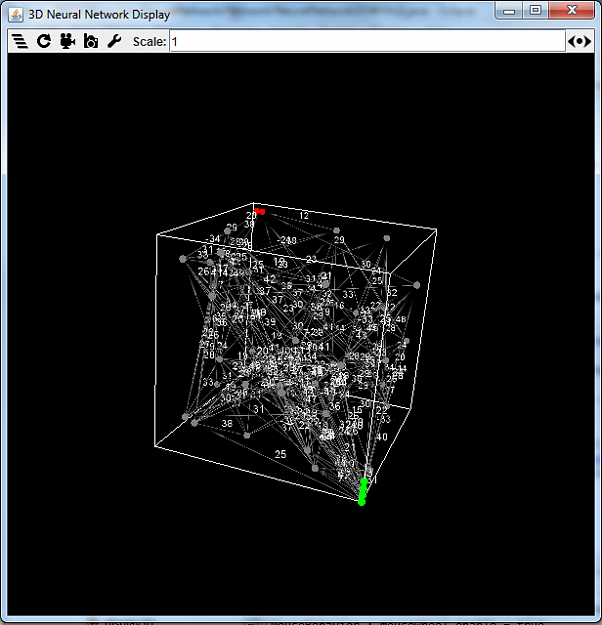

I just happen to be working on my own implementation of a Neural Network which is much more closely modeled to the human brain than common NN's are.

Attached Image (click to enlarge)

I haven't had time to take a deeper look into the thread yet but since this is one of the topics I am really interested in I might join and catch up soon

{quote} So looking at your result it seems you're a step ahead than Daniel, it's really interesting that your NN could be backtested with the same outcome for different runs! About mining bias problem , I don't know if it's a concept that could be applied to NN, btw a nice question to ask Daniel Will follow with interest your work here ! Cheers, Skyline

Ignored

Data-mining bias is a concept that applies to all system searches, regardless of how you are searching for strategies (it applies to machine learning, rule based strategies, etc). I remember a discussion between Eric and Daniel on the Asirikuy forum about the measuring of data-mining bias on machine learning strategies. I believe I am probably ahead of him regarding machine learning developments, simply because he has been centered on other developments related with the automatic generation of rule-based strategies and because I have probably worked longer on the field. Automatic system generation using price action is also very valuable, this is now also part of my live trading repertoire thanks to Asirikuy.

{quote} Could you please provide an example of this? Something simple would suffice. k

Ignored

Outside of the trading world there are many. For example think about face and audio recognition. A neural network can find many non-linear relationships that make the prediction of a face or an audio track possible while doing this with transparent methods is much more complicated. Sure, machine learning methods are simply glorified functions (input to target converters) but sometimes achieving a similar result while understanding everything "behind the scenes" (all variable interactions) is difficult.

It is also worth considering that machine learning does not need to be a total black box. For example models like random forests allow you to obtain significance measurements for your input variables. It is not easy to know how everything works inside but at least you can know that for the model A is much more important than B.

{quote} Outside of the trading world there are many. For example think about face and audio recognition. A neural network can find many non-linear relationships that make the prediction of a face or an audio track possible while doing this with transparent methods is much more complicated. Sure, machine learning methods are simply glorified functions (input to target converters) but sometimes achieving a similar result while understanding everything "behind the scenes" (all variable interactions) is difficult. It is also worth considering that machine...

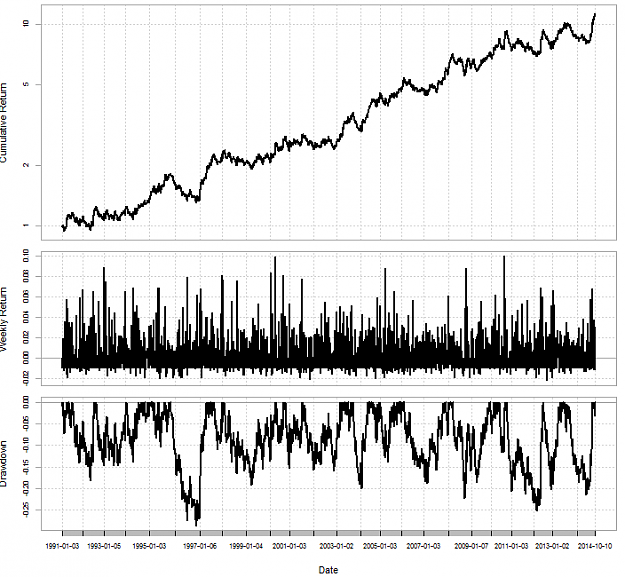

On our last construction of a strategy we used a portfolio of two models, one trading using a K-NN and the other using an SVM. The combination of both models gave something which in the end had a better performance than both separate strategies. Those of you who are keen observers may have noticed that the SVM has two parameters that the K-NN does not have (C and gamma) which are related to how the model classifies data. To make things simple, C is related to how hard the SVM is trained to classify the data and gamma is related to how fine the grain of classification actually is, how much "attention to detail" (those of you versed in statistics might want to give a simple definition that is more accurate if you wish to do so). The bigger the C the harder the training and the larger the gamma the coarser the detail. Using C=10, gamma=0.01 is a good starting point but it might not be the best to obtain the best results. By improving training (increasing C to 20) we actually can obtain better results for our SVM strategy.

Attached Image (click to enlarge)

Using larger values of C is problematic in this case because the simulation reaches a point where training does not converge (we are demanding too much separation). With this system we finally have a case where the maximum drawdown is not reached within the past 2 years but in 1997. This means that we have an algorithm which does seem to have deteriorated in predictive qualities during the past few years. The SVM used here also uses a Gaussian kernel, which means it can find more complex non-linear relationships, using different Kernel types can also change the distribution of predictions for the SVM.

A question that remains is data-mining bias. What is the probability that an SVM reaches the same level of profitability as above given the same degrees of freedom and a data series that contains no causal past-to-future correlations?

@PipMeUp: Thanks for the reference, I will obtain and study the book as soon as I am convinced about the path. (Also, I have a feeling that for the understanding/description of the 6-month drop in eurusd one should probably include the data dating back 2 or 3 years.) @stt: Thanks, I found the paper on arxiv, but in order to understand the language I think I'd better at least read the book PipMeUp recommended. {quote}

Ignored

i think you can get most of the concepts by doing coursera courses (andrew ng has one for starters). also you can get many online books to get started. Also a lot of open source code in every language (c++, python and R) is available so you really dont need to write a lot yourself.

{quote} i think you can get most of the concepts by doing coursera courses (andrew ng has one for starters). also you can get many online books to get started. Also a lot of open source code in every language (c++, python and R) is available so you really dont need to write a lot yourself. check this reddit for good pointers. with your background, i think it wont take much effort to get started.

Ignored

Whatever coding solution you consider it is extremely important that you consider how you will simulate and live trade from the start. A mistake I made in the very beginning was to only concern myself with the building of models and simulations while neglecting how I would actually take those to live trading (which was a headache later on). Make sure from the start that you can simulate your systems and live trade the exact same code it will save you a lot of pain later on.

{quote} Whatever coding solution you consider it is extremely important that you consider how you will simulate and live trade from the start. A mistake I made in the very beginning was to only concern myself with the building of models and simulations while neglecting how I would actually take those to live trading (which was a headache later on). Make sure from the start that you can simulate your systems and live trade the exact same code it will save you a lot of pain later on.

Ignored

Good point. if you are not a programmer, you need some toolkit that is already providing the interfacing. for programmers, it is not too hard to add glue between different systems. for e.g. you can pass prices via some interprocess communication methods, let your model in python do the calculations and pass back trade signal. I anyways dont use MT4 (take price feed over FIX, submit trade over FIX) so i need to build this glue anyways.

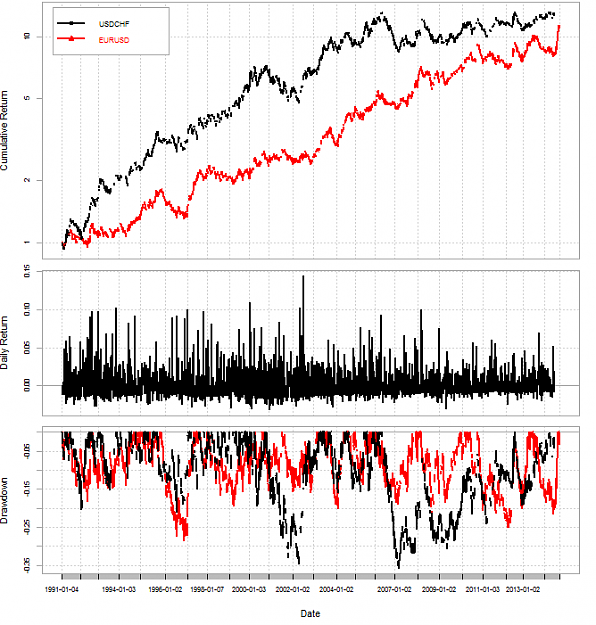

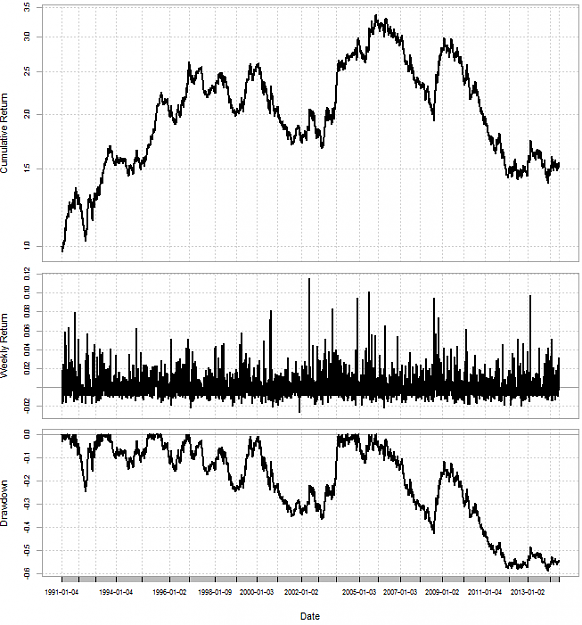

It is also rather interesting to take the same SVM technique and put it to a test on a symbol different than the EURUSD. For example we can test it on the USDCHF and see what results we get (both results are showed now for comparison). All strategy parameters are exactly the same on both currency pair tests. We can see that the results on the USDCHF are also good, although they were initially better and later started to go flat around the year 2007.

Attached Image (click to enlarge)

It is however interesting to see that the USDCHF strategy has been in fact going up steadily (although slowly) since the 35% drawdown it suffered in 2007. Although there has been heavy intervention by the SNB since 2011 the strategy did not tank, but continued to perform in a rather poor but stable manner (no deeper drawdown reached). On the other hand, a test on the GBPUSD (below) shows that the system behaves badly on this pair.

Attached Image (click to enlarge)

There is something fundamentally different when comparing the GBPUSD and the USDCHF. Do you think that it is a matter of tuning the model parameters and inputs? Do you think there is something that makes the GBPUSD fundamentally more difficult to predict?

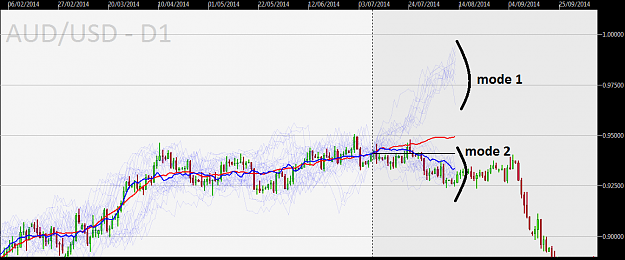

AlgoTrader how do you deal with multimodal predictions? {image}

Ignored

Depends. In my opinion it is first important to determine if the two modes do offer some predictive advantage (do their separate predictions have value or not) then if they both have value it is worth testing whether their intersection performs better (only make decisions if they agree). If the intersection does not yield a better result then it is usually better to trade a portfolio combining both attempting to reduce variance. It is in my view critical to be able to build a system so that you have some trade-related variable to play against, trying to improve accuracy may not lead to improved trading outcomes later on (so it might be heavily misleading, which happens often in academic literature on trading related ML). I have always found that it always leads to more progress when you measure against trading system statistics and attempt to improve them (especially the Sortino/Sharpe ratios).

{quote} i think you can get most of the concepts by doing coursera courses (andrew ng has one for starters). also you can get many online books to get started. Also a lot of open source code in every language (c++, python and R) is available so you really dont need to write a lot yourself. check this reddit for good pointers. with your background, i think it wont take much effort to get started. http://www.reddit.com/r/MachineLearn..._well_written/

Ignored

In addition to the excellent and highly recommended course by Andrew Ng on Machine Learning at Coursera cited by stt, the course Statistical Learning, (also offered by Stanford) was extremely good and offers an introduction to supervised learning methods. Statistical Learning starts Jan 19, 2015. This course requires much less math, and shows how to use many ML, Stat Learning functions in R in addition to providing theory behind the functions and their use:

Also worth noting is that the (FREE) textbook offered for use in the course: An Introduction to Statistical Learning, with Applications in R is a really good resource (many examples and very hands-on). This textbook is a pretty good starting point for jumping into learning statistical learning / machine learning methods, which fairly well overlap or may be seen as two branches of the same discipline offered by competing university departments.

The Machine Learning class has its homework exercises in Octave, a Matlab clone. I think it is week 6: https://class.coursera.org/ml-005/lecture/preview of this class that in my view can be used as a "how to" not overfit a trading strategy, and has some invaluable insights that all trading system developers should be aware of. The Stat Learning course above covers some of that same ground in a slightly different way so the dual insights are very beneficial.

Also to algoTraderJo, thanks for the thread, a topic that is near and dear to my heart. I'm subscribed and grateful to be along for the ride!

Joined Sep 2012

|

Status: Edge,Phsycology And Money Managemen

|949 Posts

wooow, i see alot of potential for this in another field, can someone please be so kind to solve something for me using this sophisticated machine learning algos, would be pretty quick this way

I am what Many Dream to be but only a few can achieve, im a part of the 1%

Hi algoTraderJo I'd like to reproduce your experiment post#10. I don't understand the approach. From what I understand you take the last 200 triplets of days. The first 2 define the input and the 3rd is the target. I took E/U dataset I get these stats up to yesterday:

Inserted Code

Down Down => Down 21

Down Down => Up 25

Down Up => Down 26

Down Up => Up 24

Up Down => Down 24

Up Down => Up 25

Up Up => Down 23

Up Up => Up 32

The two previous days on E/U were Up. I understand that you enter long because of the 32 chances out of 32+23.

How do you apply k-NN or SVM on this datatset? It see it as a cube {0,1}x{0,1}x{0,1}. I imagine you want to cut it with a plan (Voronoi / SVM frontier) into two parts: bullish zone and bearish zone. But the coordinates are discrete and with only two values. I'm puzzled. Can you detail a little bit more?

There is something fundamentally different when comparing the GBPUSD and the USDCHF. Do you think that it is a matter of tuning the model parameters and inputs? Do you think there is something that makes the GBPUSD fundamentally more difficult to predict

Ignored

U/CHF and E/U are strongly (anti-)correlated. It is no wonder that their results are similar. Why do you conclude there is a fundamental difference between E/U and G/U instead of questioning the validity of the strategy? Isn't it simply by random chance or overfitting that it works on E/U and normally fails on G/U? What are the results on all the other majors?

Hi algoTraderJo I'd like to reproduce your experiment post#10. I don't understand the approach. From what I understand you take the last 200 triplets of days. The first 2 define the input and the 3rd is the target. I took E/U dataset I get these stats up to yesterday: Down Down => Down 21 Down Down => Up 25 Down Up => Down 26 Down Up => Up 24 Up Down => Down 24 Up Down => Up 25 Up Up => Down 23 Up Up => Up 32 The two previous days on E/U were Up. I understand that you enter long because of the 32 chances out of 32+23. How do you apply k-NN or SVM...

Ignored

You train your K-NN or SVM using the past N examples, all of which have X bar directions as inputs and the target bar's direction as output. Using just the data you have posted you would build the examples:

Using examples like this you train the model on each bar and then you look for a prediction using the last data available. The last examples use 3 bars as input for the SVM and 4 bars as input for the K-NN. I use the open source shark C++ library for doing the model implementations. I really like this library for doing machine learning (quite fast and has a lot of options). If you want to copy my results I would strongly suggest you use this library as well, that way your model implementation will be exactly the same.

{quote} U/CHF and E/U are strongly (anti-)correlated. It is no wonder that their results are similar. Why do you conclude there is a fundamental difference between E/U and G/U instead of questioning the validity of the strategy? Isn't it simply by random chance or overfitting that it works on E/U and normally fails on G/U? What are the results on all the other majors?

Ignored

It's not that straightforward! Results can be very different for two pairs, even if they are somewhat correlated some of the time. Note that the EURUSD and USDCHF are not always so tightly correlated (a 30 day rolling window correlation measure spanning 10 years shows this). You can also create many systems that work on EURUSD for the past 20 years and then fail on USDCHF or vice versa. This does not mean that the system is "bad" in any sense, it just means that it fits generalities that are unique to each pair. I regard being fit to more than 20 years of data as being fit to general aspects of a currency pair (a level of curve fitting bias I can live with).

You're right in that this suggests that the model is fit to the conditions of the past 20 or so years on EURUSD|USDCHF however this does not mean that the algorithm works by random chance (two different things). Being fit to these conditions on the EURUSD|USDCHF also does not mean that the machine learning strategy won't work, it just means that it is fit to some general behavior that is contained in the EURUSD|USDCHF which is not present on the GBPUSD. It is therefore interesting to wonder what this is and why these generalities fail to show up on the GBPUSD.

In my experience it is useless to attempt to build something that "works for all major pairs" there are simply not enough market wide generalities in the currency markets that are profitable enough for trading in this manner. What I generally do is run strategies that show to be well fitted to the generalities of particular pairs (somewhat alike the last example on EURUSD|USDCHF) which show to have a very low change to come out of randomness (a problem I haven't addressed yet on this thread). This has worked for me over the past decade, with machine learning notably across the past several years.