Disliked{quote} The probability of 93.75% is for n=2!!! The theorem stated that clearly!!! Good work thoughIgnored

Thank you for your answer.

Do you use only n=2 ?

When I read the ultimate truth thread, I thought that we need to work with long sub-sequences.

But if we need only n=2, that makes calculation easier. Thats good.

Thank you,

Disliked{quote} Hi Jimsterk, Thanks for the code, but as i tried it, i got err message: "Error: object 'data5' not found". How can i put the bars data from MT4 / NT to buffer "data5" ? If i do it manually, i think it will time consume .... {quote} Thanks in advance. Edit: Does any one have used this (MT4 - R connection) ? http://www.forexfactory.com/showthread.php?t=260422 Or any othersimple example of using NT-R connection is also ok, thanksIgnored

I have exported the histrocal data from my mt4 into csv file.

Then the csv data is read like "data5 <- read.csv(-------)".

I use "R for mt4" made by 7bit to connect mt4 and R.

I do not know other interface...

my knowledge about programming is very poor...

One thing I want to note is that R is good to calculate vectors, but very bad to iterate.

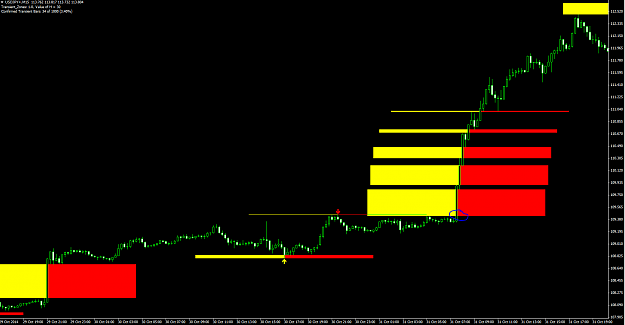

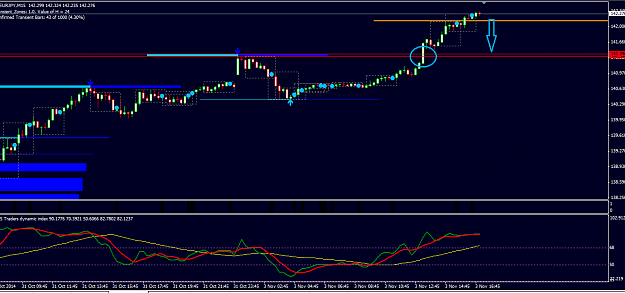

For example, I have posted this picture few months ago:

Attached Image

The data is 1-hour eurusd and sample size is about 20000.

It took about 24 hours for iteration. very slow.

C++ or matlab or other softwares are faster than R.

So if you are not already familiar to R, I do not recommend to use R.

(I am R user because I am a time series analyst and R already has packages like arma, garch, copula, etc.)

Thank you,