|

Additional Username

|

Joined Dec 2012

|129 Posts

Hi,

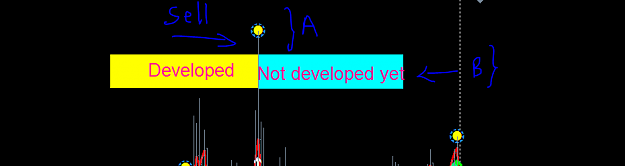

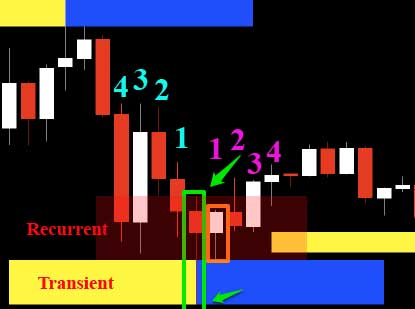

I borrow smallcat's image found here: http://www.forexfactory.com/showthre...83#post7814283. At his image, the recurrent zone is the rest of Hi/Lo - tz, the tz is at the end (low) of candle . But if i saw Eurusdd's image, the recurrent zone is a little different, it is still in Hi/Lo area, but in other side of price direction, the tz is below it. Seeing the image of Eurusdd, the transient zone is not at the end (high) of candle, where we can see a star with yellow circle there.

a) Seeing Eurusdd's image, the tz is not at high of candle. Does it mean this is the "historical" level ? If this is not the case, then we must use edited kprsa's instead of using firefox's ?

b) If this is a historical one , so current candle can go through that historical tz at a time. If this happened at H4-M15, and because this tz has small high, in H4 it can be some 5-20 pips. So, we do not need to wait at big TF, but we can go to M1 looking for a signal to enter, targeting 1-40 pips.

c) Seeing these 2 images in attachments, does it mean the both way of +/- ? the area can be upper/below of tz?

{quote} 1)Prices are 97ish % recurrent, full stop. 2)h is a value you use to identify prices that have yet to fulfill condition (1) 3)(2) does not affect nature of price. only the kind of information you receive

Ignored

Thanks mate. Yes, i think i must play with kprsa's to get my optimal h first for each TF. Then can move to other thing later ....

Hi, I borrow smallcat's image found here: http://www.forexfactory.com/showthre...83#post7814283. At his image, the recurrent zone is the rest of Hi/Lo - tz, the tz is at the end (low) of candle . But if i saw Eurusdd's image, the recurrent zone is a little different, it is still in Hi/Lo area, but in other side of price direction, the tz is below it. Seeing the image of Eurusdd, the transient zone is not at the end (high) of candle, where we can see a star with yellow circle there. a) Seeing Eurusdd's image, the tz is not at...

Ignored

What some of you don't realize when looking at that picture is that its not accurate. Eurusdd also mentioned he just "borrowed" it to give a visual of what he is talking about. When have you a forming zone, by assuming it is transient, it allows you to work with the hypothesis that prices above and below that zone is recurent.

{quote} I found the original explanations in the Similarity thread given by eurusdd. The original propositions and deductions state that with the proper h value, 97% of prices are recurrent. It does NOT say that if your h value is correct, that 97% of potentially transient bars are recurrent. To answer your other question, yes, trading purely transient zones will result in you always trading against the current trend. You will need additional tools/extrapolations from the propositions to trade in sync with...

Ignored

Hi mate, regarding your red text above, does he really say prices, and not bars? I think most of us are basing our h values on bars. The thing is, even a TZ bar (a bar containing a transient price zone) will have recurrent prices as well as transient ones, so if 97% of prices are recurrent, then much less than 97% of bars will be recurrent. [Edit: scratch that, need to think about it some more]

Regarding your blue text, I completely agree. Here are some interesting figures to chew over:

1) If the current bar is a PTZ (21 bars to the left didn't touch all prices in the current bar), then the chance of it becoming right-only recurrent within the next 21 bars is nearly four times greater than the chance of it becoming full transient.

2) If the current bar is recurrent (all prices were touched by at least one of the last 21 bars to the left), then the chance of it becoming fully recurrent within the next 21 bars is nearly four times greater than the chance of it becoming left-only recurrent.

3) So, the chance of price returning to all prices in the current bar, within the next 21 bars, is always nearly four times greater than price not returning to them.

Now if you get the h right for a given time frame and at the current price p, the previous bars never hit p, then probability is on your side for a hit within the next h bars because the probability that p is h-transient is very low. If your h is right, this probability should be about 3%. That is 97% of the time, at least one of the next h bars should hit p. This works in theory and in practice for any stochastic process similar to the ones that govern currency prices!!! Very important: If your h is correct, then the height of...

Ignored

It's possible that I misinterpreted it but it sounds like he's saying that the 97/3 rule only works if h is right, and p is referring to a set of prices, not bars. Thus, if a bar is partially transient and partially recurrent, I call it a transient bar. So if your h value is for example 3, then there are transient bars (and also transient prices) in a LOT of areas, way more than 3%.

{quote} What some of you don't realize when looking at that picture is that its not accurate. Eurusdd also mentioned he just "borrowed" it to give a visual of what he is talking about. When have you a forming zone, by assuming it is transient, it allows you to work with the hypothesis that prices above and below that zone is recurent. RRRRRRRRRRRRRRRR LTZLTZLTZ????????? RRRRRRRRRRRRRRRR With this in mind consider how price can possibly move

{quote} {quote} It's possible that I misinterpreted it but it sounds like he's saying that the 97/3 rule only works if h is right, and p is referring to a set of prices, not bars. Thus, if a bar is partially transient and partially recurrent, I call it a transient bar. So if your h value is for example 3, then there are transient bars (and also transient prices) in a LOT of areas, way more than 3%. Not sure if that answers your question or not

Ignored

No I don't think so. I mentioned it a few post earlier. Price is 97% recurrent. h is what you use to filter out the 3% via your indicator. If your h value is small then of course you will see a lot of false positives. The optimal h is a value you use to filter down the data such that it returns only 3% of the values as positive. 97/3 is the nature of price, h is the value you use to identify this values correctly. To phrase in yet another way, price remains 97/3. If you set your h to something not optimal then you are looking at data that tells you price is say 65/35 while the true nature of price remains unchanged at 97/3. Good luck.

{quote} No I don't think so. I mentioned it a few post earlier. Price is 97% recurrent. h is what you use to filter out the 3% via your indicator. If your h value is small then of course you will see a lot of false positives. The optimal h is a value you use to filter down the data such that it returns only 3% of the values as positive. 97/3 is the nature of price, h is the value you use to identify this values correctly. To phrase in yet another way, price remains 97/3. If you set your h to something not optimal then you are looking at data that...

Ignored

Sorry, how do you know price is truly 97/3? I thought h was the metric used to determine price transience/recurrence, and 97/3 was a "goal" and not a "fact".

{quote} No I don't think so. I mentioned it a few post earlier. Price is 97% recurrent. h is what you use to filter out the 3% via your indicator. If your h value is small then of course you will see a lot of false positives. The optimal h is a value you use to filter down the data such that it returns only 3% of the values as positive. 97/3 is the nature of price, h is the value you use to identify this values correctly. To phrase in yet another way, price remains 97/3. If you set your h to something not optimal then you are looking at data that...

Ignored

Thanks mate for this good post. I just think, it must be exactly 97/3 %, or it can be have some tolerance, may be like : 96.5/3.5 , 97.1/2.99, 96.85/3.15, etc. If yes, then it must be a "tolerance" value for this . Hm , it becomes more complex. Now it is not only h & k, but there is new variable "tolerance" .....

{quote} Thanks mate for this good post. I just think, it must be exactly 97/3 %, or it can be have some tolerance, may be like : 96.5/3.5 , 97.1/2.99, 96.85/3.15, etc. If yes, then it must be a "tolerance" value for this . Hm , it becomes more complex. Now it is not only h & k, but there is new variable "tolerance" .....

{quote} Sorry, how do you know price is truly 97/3? I thought h was the metric used to determine price transience/recurrence, and 97/3 was a "goal" and not a "fact".

Ignored

I don't. It is an accepted and reasonable working probability.

h and k is what we use to tune the indicators such that it provides a reliable reflection of the nature of price

h is the metric you can use to determine the kind of data you receive form your indicator.

No indicator can possibly make the nature of price more transient or recurrent.

Joined Apr 2012

|

Status: ipsa scientia potestas est

|682 Posts

Just to think aloud, there should be one more variable added to the calculation of possibility of potential transient zone to become recurrent zone which should be connected with the price distance from that zone. (May be the standard deviation of price ranges for the x period back)

{quote} If you set your h to something not optimal then you are looking at data that tells you price is say 65/35 while the true nature of price remains unchanged at 97/3. Good luck.

Ignored

If nature of price is 97/3 why looking for H? Better to buy or sell randomly than looking for a H that reduce your probabilties...

Bottomless wonders spring from simple rules, which are repeated without end

{quote} LOL that has crossed my mind. If you don't like to use H to get you 97/3, you can use K instead.

Ignored

Lets agree for now that price is indeed 97/3, then your hypothesis is correct. In fact given that condition, all you need to do is just randomly pick any price value of X on your chart and you have a 97% working probability that price will return to your chosen value of X at some point in time.

But do you really think the above premise can really be traded? If you cannot get past this point I am afraid the discussion will have to end here.

{quote} {quote} Lets agree for now that price is indeed 97/3, then your hypothesis is correct. In fact given that condition, all you need to do is just randomly pick any price value of X on your chart and you have a 97% working probability that price will return to your chosen value of X at some point in time. But do you really think the above premise can really be traded? If you cannot get past this point I am afraid the discussion will have to end here.

Ignored

CFD beat me to it.

This is at the heart of using h as the filter for trading.

The entire premise (by Eurusdd) was to negate the alternative proposition that the market is random. If that proposition is false, why trade randomly? That would not make sense.

If you knew that price was recurrent most of the time 97% and you spotted a range. And you had an edge that allowed you to catch a bottom or top, then how more probably are you that you will hit the range you spotted? 97% confident?

I suspect that people here are confusing or placing more emphasis on Trade Entry instead of Trade Exit.

A pip is only worth it if you know how much you risked to earn it

{quote} {quote} Lets agree for now that price is indeed 97/3, then your hypothesis is correct. In fact given that condition, all you need to do is just randomly pick any price value of X on your chart and you have a 97% working probability that price will return to your chosen value of X at some point in time. But do you really think the above premise can really be traded? If you cannot get past this point I am afraid the discussion will have to end here.

Ignored

If i take a randomly price now, for example 1232 on gold. I wait 5 minutes for example, and price is now at 1231 and price have not yet come back to 1232 on a tick by tick chart. Does that mean that price have 97% if i buy now, that price will come back to 1232?.

Of course you dont need bars for that, cause you cant really see if price come back or not, you need a tick by tick chart.

Sure i need time, 5 minutes in this case, but in another case it will be 10 minutes, 4 minutes or 30 minutes, so i'd better take a tick by tick chart and dont matter about time, cause H will be different for each trade, pips potentiel win will be different on every trade. I must just focus on one price not revisited.

Does it makes sense? or am i totally out of business?

(sorry for that post i work on TZ too on the same way that the thread, but i want to be sure to well understand).

Bottomless wonders spring from simple rules, which are repeated without end