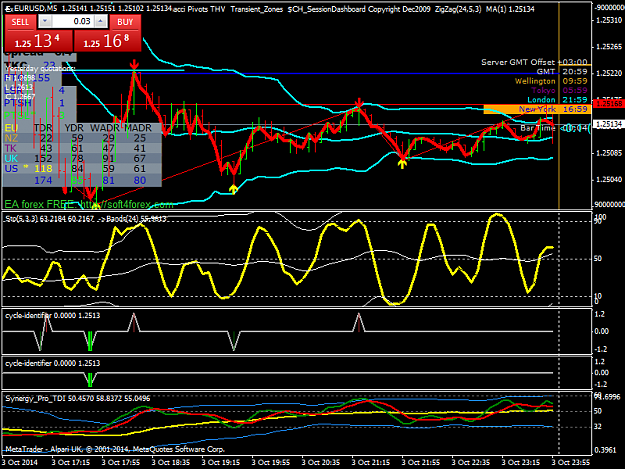

Could it be this simple?

Open DS zone has X% chance of clearing within Y-time, where X is a function of Y=H, given by our friend K (not k the variable). If correct, next would be to assess relative strength of zone based on size as well as age, and another variable related to ATR, slope of price, or current volatility, since Markov may or may not be at home.

Also if correct, some of the account histories posted, while all green, were much less than 1:1 R:R. This still means we are missing the key to EURUSDD's trades, 10 Pt SL, never 3 losses in a row... but we are working with only 60% true DS bars... so seems to jive. Not that it is needed, but, like a proper jungle cat, I may as well die if I no longer hunt.

If I have this part correct, I will start working on the range bars idea. Interesting to see what happens when time is pulled from the equation. It may purify or destroy the analytics, since time is absolutely relevant. But is time relevant simply with regard to rate of price change, or is it predictive all by itself - akin to the likelihood of spilling the beans after being tortured for time(t0,t1,t2). Will see. Plz someone give me a nudge if the above is correct - would like to move onto testing range bars rather than testing to see if I got it right.

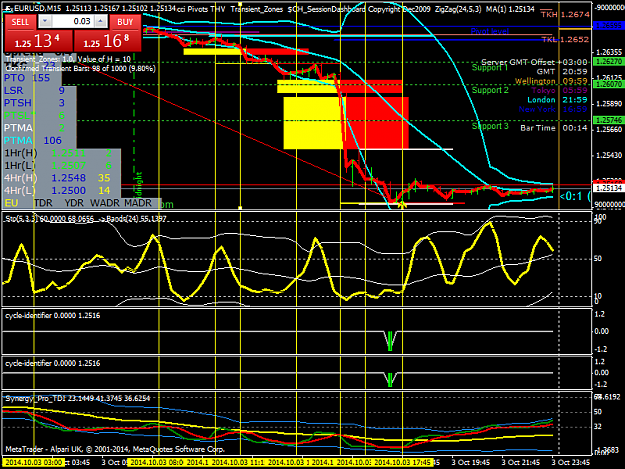

Open DS zone has X% chance of clearing within Y-time, where X is a function of Y=H, given by our friend K (not k the variable). If correct, next would be to assess relative strength of zone based on size as well as age, and another variable related to ATR, slope of price, or current volatility, since Markov may or may not be at home.

Also if correct, some of the account histories posted, while all green, were much less than 1:1 R:R. This still means we are missing the key to EURUSDD's trades, 10 Pt SL, never 3 losses in a row... but we are working with only 60% true DS bars... so seems to jive. Not that it is needed, but, like a proper jungle cat, I may as well die if I no longer hunt.

If I have this part correct, I will start working on the range bars idea. Interesting to see what happens when time is pulled from the equation. It may purify or destroy the analytics, since time is absolutely relevant. But is time relevant simply with regard to rate of price change, or is it predictive all by itself - akin to the likelihood of spilling the beans after being tortured for time(t0,t1,t2). Will see. Plz someone give me a nudge if the above is correct - would like to move onto testing range bars rather than testing to see if I got it right.