- Does the market have a constant mean ? If yes how to approximate it ?

- If the mean is not constant, its variable as the market changes structure, how to approximate it given out sample size ?

- My research to find the best model that models the mean.

By the "mean" i mean the statistical mean ,not the median, which is the separator half of the distribution in case of the price the half line of the entire market which for example aproximately the (alltime highest highs + alltime lowest lows) /2

So since the market is ever changing, i fixed the sample size to 1440 M1 bars which is 1 day of data, since its probably a logical separator between samples because the volatility distribution is also separated by the low liquidity nights when the London SE and NY SE is closed.

So i chooses 1440 to be out sample size, perhaps it could have been 7200 aswell which is 1 week, because there is a volatility gap between Friday afternoon and Monday morning aswell.

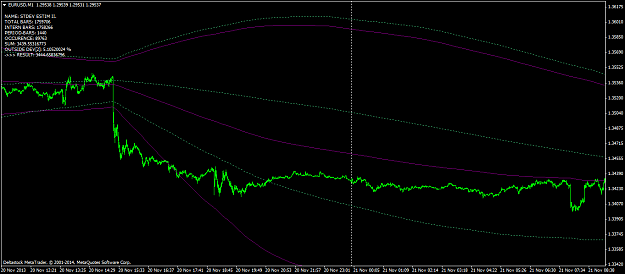

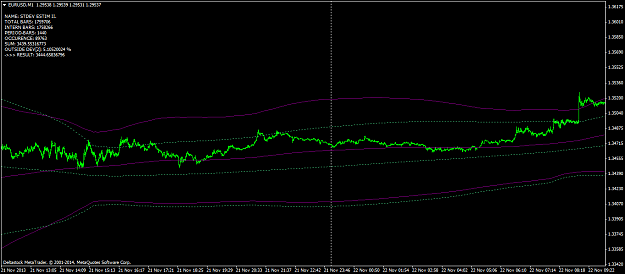

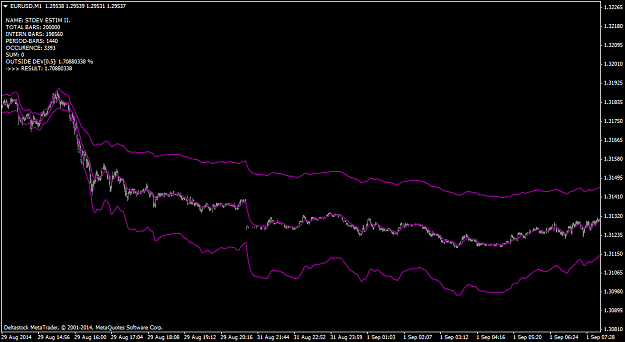

I`ve tested various moving averages to find the mean but most of them werent responsive to the price.Here are the classical moving averages, i always used Median Price ,dont confuse it with market median, which is (High[position]+Low[position]) /2 because it reflects the market better than Close price.

So these averages have PERIOD 1440, M1 bars, MEDIAN PRICE ,SHIFT 0

And by colour are the following: Yellow=Smoothed Simple,Blue =Simple(Arithmetic) ,Purple=Exponential Weighted, Red=Linear Weighted

As you can see the linear weighted is the most responsive, and less lagging, and the smoothed is the worst,also the simple moving average is pretty far from a mean.

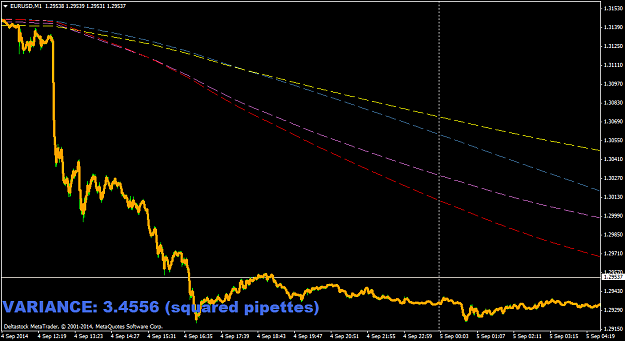

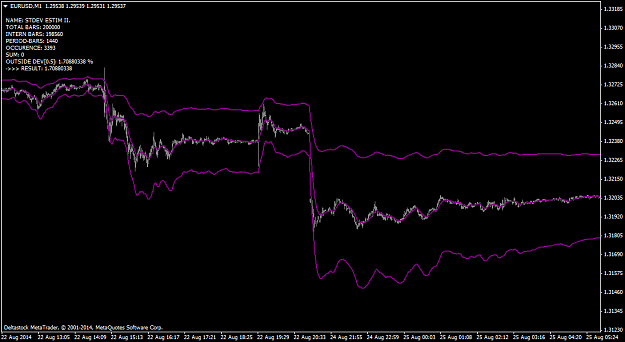

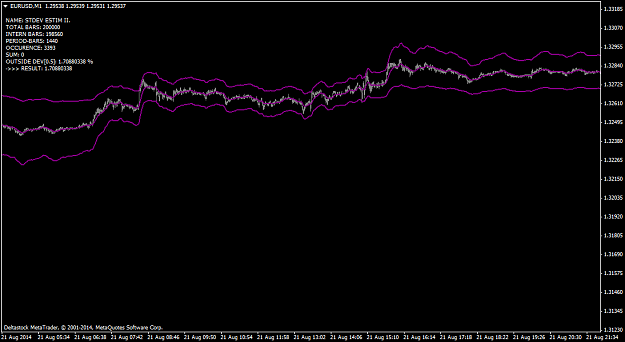

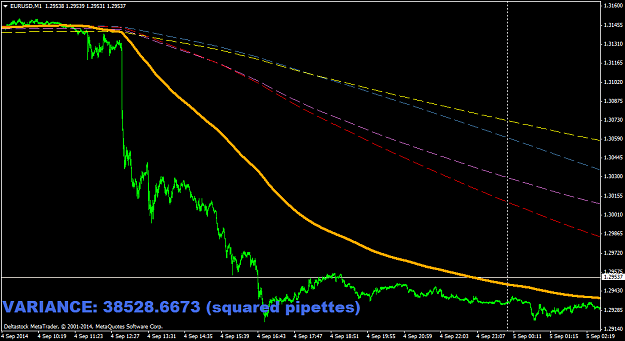

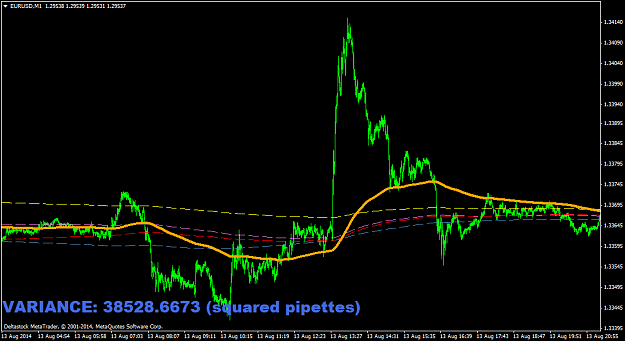

And then i saw that these "classical" moving averages are as far away from a statistical mean as the sky is from the ground, so i took my skills and coded my own moving average, and i`ve been experimenting with it.Set also to PERIOD 1440, and its orange colored, while the other MA's are the same color but set them dashed so that it becomes more visible:

As you can see its much more responsive to the price, and less lagging.Also i`m measuring the variance of the price around my moving average to try to gauge in the dispersion of price around it.

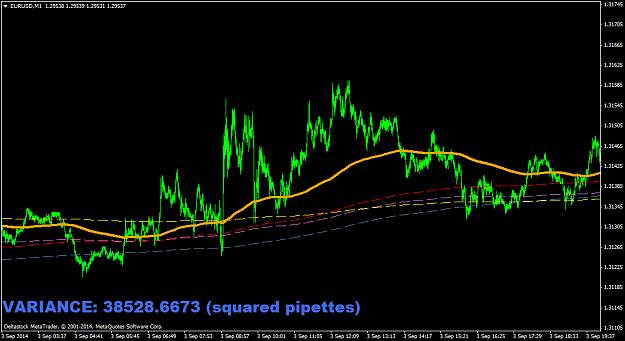

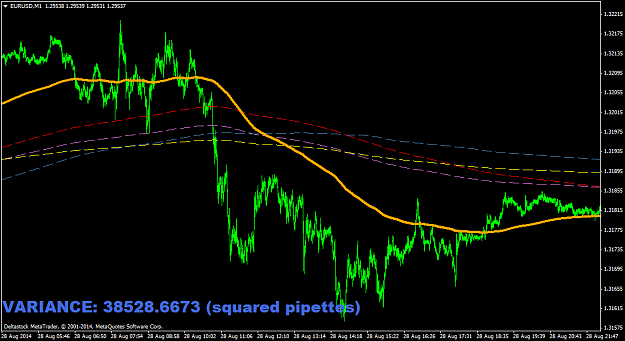

I suppose the less the variance is, the more accurately my MA measures the mean, the problem is that if i increase the magnitude of my MA's filter then the variance decreases almost to 0, and my MA becomes identical with a PERIOD 1 moving average.

So its almost like a period 1 moving average is the mean of the market, that is, that every tick is the current mean.However this is absurd because then the MA doesnt tell anything about the trend or the bias in the price.

So i would need a perfect balance between LAGG AND ACCURACY or in other words the mean which the price will hover around the most, which is not itself (not the last price).

=============££££££££££============$$$$$$$$$$$$$==============€€€€€€€€€€€€===============¥¥¥¥¥¥¥¥¥¥¥¥¥================

LATEST MODEL: Version 2.8 of my filter

- MY RESEARCH GOAL: 5,000% GROWTH (BASED ON BACKTEST)