Information Derived from the Observables

Market observables deal primarily with prices and trading (volume). Auction Market Theory owes it's utility to value. In this section, the first steps are taken to convert the one-dimensional price to the two-dimensional value description of auction markets. First, the observables are fleshed out.

1) Trading hours.

Non-electronic markets open and close at set times. Trading is tied to the market timeframe. Orders accumulate between the close and the next day open, creating an order backlog. At the close, traders who do not wish to hold overnight must exit their positions. In this simple way, market hours exert a level of control over trading structure. One of the ramifications of trading hours is a specialized behavior pattern in the first hour of trading. This timeframe is called the initial balance because floor members seek to define the trading range for the day from the order backlog. How well they accomplish a stable balance affects the subsequent trading for the day. At the market close, those who must trade tend to create an extended closing range. At the very least, the closing range is deleterious to the public trader since their 'market on close' orders most often get the worst side of the range.

Electronic markets tend to show much the same structure as the floor because arbitrage exists and they often take their cues from the floor. As electronic trading matures*, those markets will likely lose a large part of their dependence on the exchange floor. (*that was written 12 yrs. ago)

Exchanges, or clearing authorities for some electronic exchanges, interact with the public principally in setting margins. Margin is 'earnest money' guaranteeing the broker that losses are covered. A trader's interest in margins in part is the amount of money that must be deposited in order to trade. Far more important is how the exchanges set margins. With a lot of experience backing them up, the exchange margin is set to mirror the risk. Trading models inevitably have a risk function of some sort. However, anytime exchange margin is changed, there is a change in the risk being taken. Since exchange margins are not necessarily what a broker charges, (brokers often charge more), keeping track of exchange margins takes some effort.

2) Prices are Set by Negotiation

Each trade has a buyer and a seller

3) Accepted Prices

An accumulating market has a single price - volume distribution roughly in the shape of a bell curve.

4) Rejected Prices

Prices not accepted by the market generate very light volume. Such prices rarely trade and the trader who wants to do business there has little opportunity to do so.

5) Accumulation and Distribution

The accumulating gives way to a distributing, or moving market

6) Day Traders and Swing/Position Traders

Day traders, by definition, are out of the market by the close. They have no long term effect on the market, since they are holding positions only a fractional part of the day and not at all overnight. Markets do move, and sometimes rather violently. Exchange members, as a group, tend to be flat or hedged at the close. Longer term demand, the sort that moves markets, comes from those who hold positions past the close. These are the position traders in the futures, options and debt markets; and the institutions and public in equities. Day traders are the opportunists who jump on a move and hold a short time. Position traders have the patience to hold longer term, creating demand.

7) Day-by-Day Variation in Market Activity

Perception of opportunity drives the day and short term position trader.

8) Heavier Trading at Open and Close

It was pointed out in item 1) that markets with floor trading develop a backlog prior to open. The necessity of day oriented trading exiting prior to close develops a backlog there, also. Since both open and close have associated ranges, demand is artificially changed at these particular times. With the rise of electronic markets, artificial demand from exchange openings and closings will disappear.

9) Trading Ranges

Short timeframe traders gain by quickly recognizing an opportunity, seizing it and just as quickly exiting. Return is a function of the speed and range of the day's internal movements. So is risk. A quantitative measure of risk in the day timeframe evaluates average swing size. Some swings are more risky to trade than others. At the other extreme, some markets are so un- risky that their opportunity is unacceptably small to the day trader. One of the capabilities of Auction Market Theory is to explore and quantize this aspect of auction markets.

10) Serial Correlation and Forecasting

There is little day-to-day serial correlation in auction markets (see e.g. Speculation, Hedging ..., Labys & Granger, 1970; or reference 4, p19). This makes today's trading a poor predictor for tomorrow. Consequently, it would be a questionable aim of a market theory to propose forecasting market behavior. AMT trading is based on understanding the current market situation and having a strategy for change; not predicting "tomorrow's" price.

11) Members Functions

So far market knowledge is equated to an understanding of value based data displays. A market is also comprised of people, the public and the members and/or professional traders. Four classes of futures members inhabit the floor. Non-members must interact with them. It is to the public's advantage to understand member's motivation. Class 1 are the Locals or scalpers, the other side of virtually every transaction. They work for themselves, provide liquidity and are most comfortable with balanced markets. Class 2 are the commercials who's job is to trade and hedge for their companies. These are the businessmen of the floor. Their company will be a large commercial firm, e.g. Morgan Stanley. Since commercials know both the cash and futures markets, they are the best informed traders on the floor. They too work best in balanced markets. In addition to their "business" they may speculate when prices are out of line (capping). Commercials typically do five to fifteen percent of the volume. Class 3 are members clearing for other, off-floor, members. This class accounts for around five to ten percent of the volume. Lastly, Class 4 clears for us, the public. We, the public, are typically twenty to thirty percent of the day's trading volume. Chicago Board of Trade and Chicago Mercantile Exchange release the Liquidity Data Bank reports with volume-price-member type statistics.

12) Electronic Trading Platforms

Electronic platforms are developed primarily to cut trading costs. A side effect is that trades clear faster and more accurately. Member - public interactions are minimized. In some cases simultaneous trading occurs on the floor and on the electronic market. At this time, many traders are placing orders electronically through their computers but the trades are still routed to a trading desk and pass through the standard floor procedures. While how a trade is accomplished is of little moment theoretically; practically there can be a big difference in costs.

As electronic trading grows, the influence of floor members will diminish. The current effects of exchange trading hours will no doubt diminish as well. These changes will little affect the fundamental characteristics of auction markets. Most likely, a trader familiar with auction market basics will have minimal trouble incorporating such changes. For instance, if opens and closes disappear entirely, a new timeframe to replace the exchange day will become apparent, probably defined by trading volume. Currently, the 24 hour electronic markets show consistent times of higher volume tied into the market being traded.

13) Markets Cycle

Markets continually move from balance to testing the balance, to trend, to testing for end of trend and back to balance. The time spent in any one phase may be long or short. There is no valid method of predicting when the phase may change. Further, any phase may be arbitrarily short. The change from balance to trend can occur in minutes or may take days of testing the balance. The progression is known: a market in balance today will surely break out in the future.

Many markets do not report volume along with the price ticks. In fact, some markets never report volume at price, just end of day totals for all prices. A surogate for volume (demand) is price over time.

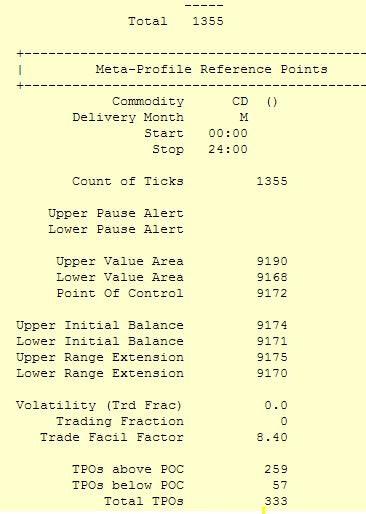

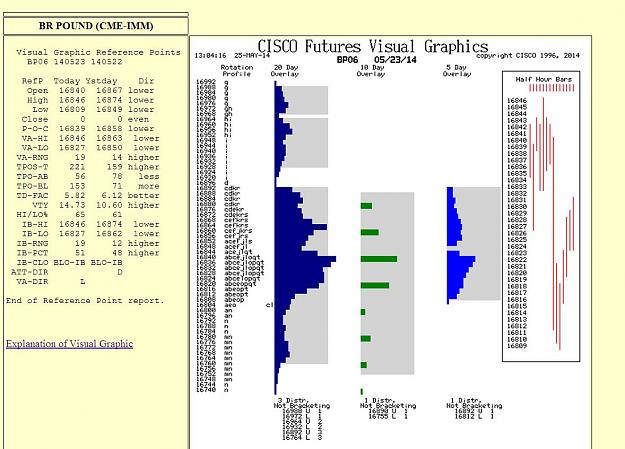

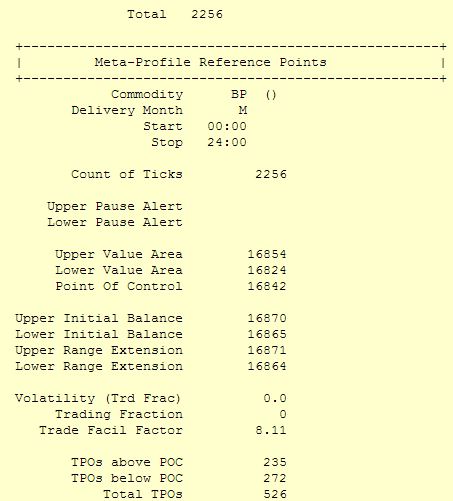

Practically, TPOs greatly simplify defining market structure within the trading day.

Price-over-time, in line with general usage, is designated value. Value maps out a wide area in the mid region of a balanced market.

Market observables deal primarily with prices and trading (volume). Auction Market Theory owes it's utility to value. In this section, the first steps are taken to convert the one-dimensional price to the two-dimensional value description of auction markets. First, the observables are fleshed out.

1) Trading hours.

Non-electronic markets open and close at set times. Trading is tied to the market timeframe. Orders accumulate between the close and the next day open, creating an order backlog. At the close, traders who do not wish to hold overnight must exit their positions. In this simple way, market hours exert a level of control over trading structure. One of the ramifications of trading hours is a specialized behavior pattern in the first hour of trading. This timeframe is called the initial balance because floor members seek to define the trading range for the day from the order backlog. How well they accomplish a stable balance affects the subsequent trading for the day. At the market close, those who must trade tend to create an extended closing range. At the very least, the closing range is deleterious to the public trader since their 'market on close' orders most often get the worst side of the range.

Electronic markets tend to show much the same structure as the floor because arbitrage exists and they often take their cues from the floor. As electronic trading matures*, those markets will likely lose a large part of their dependence on the exchange floor. (*that was written 12 yrs. ago)

Exchanges, or clearing authorities for some electronic exchanges, interact with the public principally in setting margins. Margin is 'earnest money' guaranteeing the broker that losses are covered. A trader's interest in margins in part is the amount of money that must be deposited in order to trade. Far more important is how the exchanges set margins. With a lot of experience backing them up, the exchange margin is set to mirror the risk. Trading models inevitably have a risk function of some sort. However, anytime exchange margin is changed, there is a change in the risk being taken. Since exchange margins are not necessarily what a broker charges, (brokers often charge more), keeping track of exchange margins takes some effort.

2) Prices are Set by Negotiation

Each trade has a buyer and a seller

3) Accepted Prices

An accumulating market has a single price - volume distribution roughly in the shape of a bell curve.

4) Rejected Prices

Prices not accepted by the market generate very light volume. Such prices rarely trade and the trader who wants to do business there has little opportunity to do so.

5) Accumulation and Distribution

The accumulating gives way to a distributing, or moving market

6) Day Traders and Swing/Position Traders

Day traders, by definition, are out of the market by the close. They have no long term effect on the market, since they are holding positions only a fractional part of the day and not at all overnight. Markets do move, and sometimes rather violently. Exchange members, as a group, tend to be flat or hedged at the close. Longer term demand, the sort that moves markets, comes from those who hold positions past the close. These are the position traders in the futures, options and debt markets; and the institutions and public in equities. Day traders are the opportunists who jump on a move and hold a short time. Position traders have the patience to hold longer term, creating demand.

7) Day-by-Day Variation in Market Activity

Perception of opportunity drives the day and short term position trader.

8) Heavier Trading at Open and Close

It was pointed out in item 1) that markets with floor trading develop a backlog prior to open. The necessity of day oriented trading exiting prior to close develops a backlog there, also. Since both open and close have associated ranges, demand is artificially changed at these particular times. With the rise of electronic markets, artificial demand from exchange openings and closings will disappear.

9) Trading Ranges

Short timeframe traders gain by quickly recognizing an opportunity, seizing it and just as quickly exiting. Return is a function of the speed and range of the day's internal movements. So is risk. A quantitative measure of risk in the day timeframe evaluates average swing size. Some swings are more risky to trade than others. At the other extreme, some markets are so un- risky that their opportunity is unacceptably small to the day trader. One of the capabilities of Auction Market Theory is to explore and quantize this aspect of auction markets.

10) Serial Correlation and Forecasting

There is little day-to-day serial correlation in auction markets (see e.g. Speculation, Hedging ..., Labys & Granger, 1970; or reference 4, p19). This makes today's trading a poor predictor for tomorrow. Consequently, it would be a questionable aim of a market theory to propose forecasting market behavior. AMT trading is based on understanding the current market situation and having a strategy for change; not predicting "tomorrow's" price.

11) Members Functions

So far market knowledge is equated to an understanding of value based data displays. A market is also comprised of people, the public and the members and/or professional traders. Four classes of futures members inhabit the floor. Non-members must interact with them. It is to the public's advantage to understand member's motivation. Class 1 are the Locals or scalpers, the other side of virtually every transaction. They work for themselves, provide liquidity and are most comfortable with balanced markets. Class 2 are the commercials who's job is to trade and hedge for their companies. These are the businessmen of the floor. Their company will be a large commercial firm, e.g. Morgan Stanley. Since commercials know both the cash and futures markets, they are the best informed traders on the floor. They too work best in balanced markets. In addition to their "business" they may speculate when prices are out of line (capping). Commercials typically do five to fifteen percent of the volume. Class 3 are members clearing for other, off-floor, members. This class accounts for around five to ten percent of the volume. Lastly, Class 4 clears for us, the public. We, the public, are typically twenty to thirty percent of the day's trading volume. Chicago Board of Trade and Chicago Mercantile Exchange release the Liquidity Data Bank reports with volume-price-member type statistics.

12) Electronic Trading Platforms

Electronic platforms are developed primarily to cut trading costs. A side effect is that trades clear faster and more accurately. Member - public interactions are minimized. In some cases simultaneous trading occurs on the floor and on the electronic market. At this time, many traders are placing orders electronically through their computers but the trades are still routed to a trading desk and pass through the standard floor procedures. While how a trade is accomplished is of little moment theoretically; practically there can be a big difference in costs.

As electronic trading grows, the influence of floor members will diminish. The current effects of exchange trading hours will no doubt diminish as well. These changes will little affect the fundamental characteristics of auction markets. Most likely, a trader familiar with auction market basics will have minimal trouble incorporating such changes. For instance, if opens and closes disappear entirely, a new timeframe to replace the exchange day will become apparent, probably defined by trading volume. Currently, the 24 hour electronic markets show consistent times of higher volume tied into the market being traded.

13) Markets Cycle

Markets continually move from balance to testing the balance, to trend, to testing for end of trend and back to balance. The time spent in any one phase may be long or short. There is no valid method of predicting when the phase may change. Further, any phase may be arbitrarily short. The change from balance to trend can occur in minutes or may take days of testing the balance. The progression is known: a market in balance today will surely break out in the future.

Many markets do not report volume along with the price ticks. In fact, some markets never report volume at price, just end of day totals for all prices. A surogate for volume (demand) is price over time.

Practically, TPOs greatly simplify defining market structure within the trading day.

Price-over-time, in line with general usage, is designated value. Value maps out a wide area in the mid region of a balanced market.

Markets are not efficient, rather they are effective - Jones