- 3 Reasons Why the Dollar Erased Post NFP Gains

- What is the Greatest Risk for EUR Next Week?

- What Could Drive GBP to 1.70

- Will NZD Hit for Fresh 2 Year Highs?

- AUD: Busy Week Ahead with RBA, PMI and Retail Sales on Tap

- CAD: Oil and Gold Prices Rebound

- Rally in Yen Crosses Fizzle, Disposable Incomes in Japan Fall

3 Reasons Why the Dollar Erased Post NFP Gains

When the non-farm payrolls report was initially released, the U.S. dollar traded sharply higher against all of the major currencies but by the end of the North American trading session not only did the greenback give up all of its gains but the S&P 500 and Treasury yields also turned lower. Even though non-farm payrolls rose by the largest amount since January 2012 and the unemployment rate dropped to its lowest level since September 2008, investors were not impressed. We can provide at least 3 reasons why the dollar erased its pose NFP gains. #1 - There was underlying weakness in the data with the improvement in the unemployment rate driven primarily by the drop in labor force participation. #2 - The NFP report won't change the Fed's stance on monetary policy. When Yellen speaks next week, she will remind us that tapering does not equal tightening #3 - The slide in U.S. yields after a strong jump in payrolls makes the dollar a more attractive funding currency. All of this has investors thinking that if the dollar can't rise after the increase in payrolls, nothing will be able to drive it higher in the near term. Outside of the ISM non-manufacturing report, there are no major U.S. data scheduled for release next week and with NFPs released before ISM, Monday's report carries even less significance. Instead, speeches from Federal Reserve officials will play a bigger role in how the dollar trades but we don't expect any excessive optimism.

The April labor market report blew out everyone's expectations. Non-farm payrolls rose 288k in the month of April, up from 203k. The most optimistic Wall St economists were calling for a 250k rise but what really caught the market by surprise was the sharp improvement in the unemployment rate, which fell to 6.3%, its lowest level since September 2008. At best, economists were looking for an improvement to 6.5% from 6.7%. The report would have been unambiguously positive for the dollar if not for the drop in the labor force participation rate, which indicates that the only reason why the unemployment rate declined was because 806k people dropped out of the work force. Average hourly earnings also stagnated so for the time being no there's major risk of inflation.

Everyone will be looking to next week's speech by Janet Yellen for indications on whether the improvement in the unemployment rate will accelerate the central bank's plans for tightening and unfortunately we think that the answer is still no. Internally, policymakers may consider pulling forward their rate hike plans but these views will not be shared publicly because of the upside risk they pose to yields. Job growth was very strong and the unemployment rate declined but Yellen will most likely downplay the improvement by saying that tapering does not equal tightening. When she delivered her first post monetary policy meeting press conference, she said rates could rise 6 months after QE ends. If the central bank continues its current pace of tapering, asset purchases should reach zero by October or December at the latest and 6 months after that would be sometime between April and June which is right in line with current market expectations. Given the drop in labor force participation and zero wage growth, there's no reason for the Fed to ramp up expectations for tighter monetary policy. In fact, it would be in their interest rates to keep rates low to encourage workers to return to the workforce.

Here are My Top 10 Takeaways from US Jobs Report:

- Not a Game Changer for Fed Since Labor Force Participation Down and Wage Growth Flat

- Flattening of yield curve post NFPs - Means USD Rally Limited

- Rate Hike Expectations Pulled forward to June 2015 form July 2015 - No big deal

- Non-Farm Payrolls 288k vs. 203k - Strongest since Jan 2012

- Unemployment Rate 6.3% vs. 6.7% - Lowest since September 2008

- Labor Force Participation Rate drops to 62.8% from 63.2% - Improvement in unemployment rate caused by shrinking workforce (806k people dropped out)

- Broader U-6 Unemployment Rate drops to 12.3% from 12.7%

- Average Hourly Earnings Stagnates - No Wage Growth

- Manufacturing Employment grows 12k from 7k

- ***Yellen is speaking next week, she will most likely repeat tapering does not equal tightening

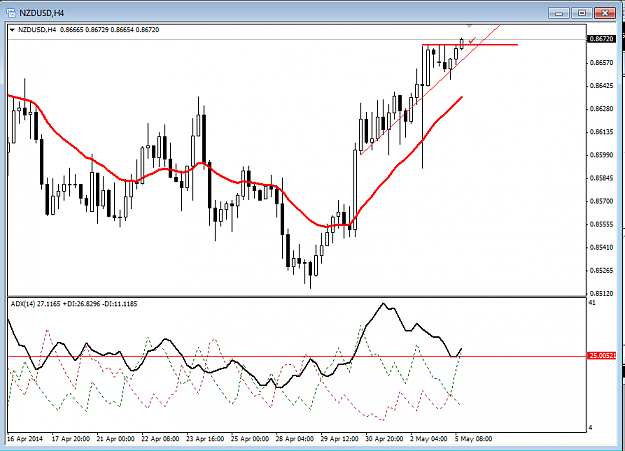

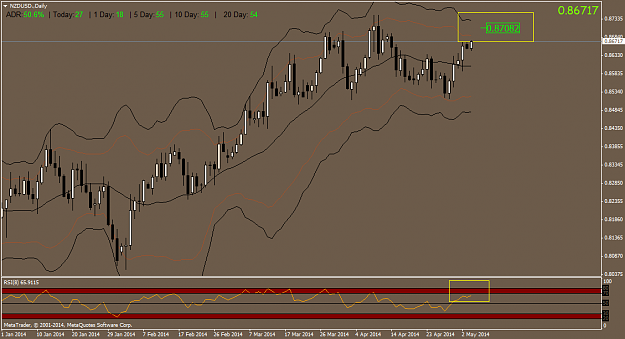

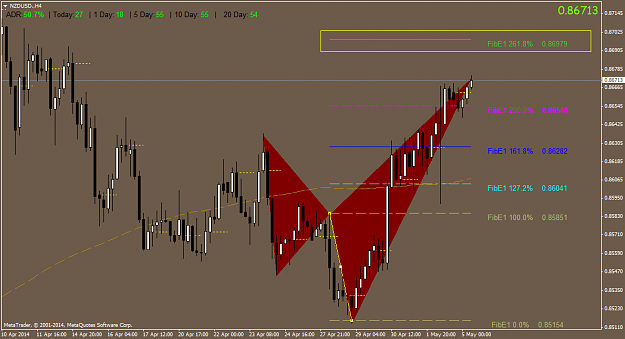

Will NZD Hit for Fresh 2-Year Highs?

The best performing currency pair this week was NZD/USD. On Friday alone, the currency added approximately 0.4% to its gains. Although there was very little New Zealand data released this week to support the rally, NZD benefited from its yield advantage over the dollar. NZD/USD appreciated 4 out of the last 5 trading days and in order for the rally to continue and for the currency to hit fresh 2-year highs, next week's New Zealand employment report needs to be strong. Economists are looking for the unemployment rate to drop to 5.8% from 6% and employment change to rise by 0.6%. Considering that these are optimistic forecasts to begin with, if the data simply meets expectations, NZD/USD could test 0.8745. There are a lot of important economic reports scheduled for release from the 3 commodity producing-countries next week. AUD will be in play with RBA, retails sales, PMI services and Chinese data scheduled for release. Canada has trade, IVEY PMI and its monthly employment report. Unlike NZD, AUD has been stuck in a narrow 0.9203 to 0.9316 trading range versus the dollar for the past week and there are enough Tier 1 economic reports on the calendar for the range to be broken. The Canadian dollar on the other hand is vulnerable to additional losses if job growth slowed in April.

Rally in Yen Crosses Fizzle, Disposable Incomes in Japan Fall

A number of Japanese economic reports were released overnight but it was U.S. non-farm payrolls that dictated the performance of USD/JPY. After the initial NFP report, USD/JPY touched 103 but by the end of the North American trading session, it had given up all of its gains and this sell-off dragged all of the Yen crosses lower. We need to look no further than the intraday reversal in Treasury yields for an explanation of why the rally in USD/JPY fizzled. According to the latest economic reports from Japan, consumers spent voraciously ahead to consumption tax hike. Overall household spending jumped 7.2%, the largest increase ever. While this is great news for Japan, it is also worth noting that real disposable incomes dropped 3.2%, marking the 8th straight month of decline. In order to maintain a steady recovery, the Japanese government needs to make sure that wages rise in lockstep with inflation. If disposable incomes continue to fall as prices rise, it would be viable reason for the central bank to ease monetary policy. However for the time being, the data has been good. In addition to spending, the job to applicant ratio also rose slightly to its highest level since July 2007. Looking ahead we have a quiet week in Japan but with the abundance of Tier 1 economic reports from other parts of the world, don't expect the Yen pairs to remain dormant. The 102-level is still at risk and it won't take much for the support level to break.