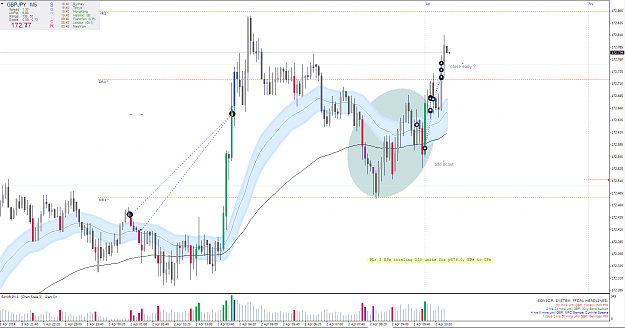

Disliked{quote} I agree with you, the point of PVSRA is to trade small and average out your entries to get a better R:R. I think it all comes down to how much are you willing to 'risk'? This could be a certain % of your account. Or, another point made by the infamous master sonicdeejay is to watch your trade like a hawk. By this I would say always be on the look out for MM's transitioning from bulls to bears and vice versa. Everybody here should be applying PVSRA to all timeframes to paint the picture of what's really going on. If all timeframes are in...Ignored

agreed... I know considerable draw down is expected(if you risk alot) with this system and the amount of R:R justifies it,

but I was curious if there was any other way to mitigate or reduce long periods of exposure without it just being through smaller lot sizes and and amount of trades.

Theoretically, your account should be able to handle -500 pips for each trade(lets say 5-20 trades) for each pair with potentially 6-8 pairs open.

this would mean that your account would need to be able to handle a negative amount of 60,000 pips or $6,000 of draw down when trading 0.01 standard lot sizes...

obviously this is worse case scenario, but we cannot predict where price will go.

fxvps dot biz - Low latency, Low Cost & V. Fast FX VPS Servers - free trial