Good post initiated by umbro & responded by tah. I'm by no means a successful trader nor an expert, but to add the points I put illustrations below:

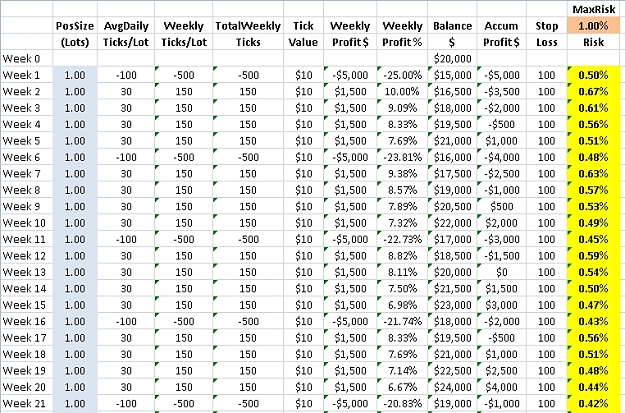

Picture 1: A hypothetical trades journal with:

SL 100 pips

TP 30 pips

Losing/Winning 1:4

Number of trades 5/week

Position size 1/trade

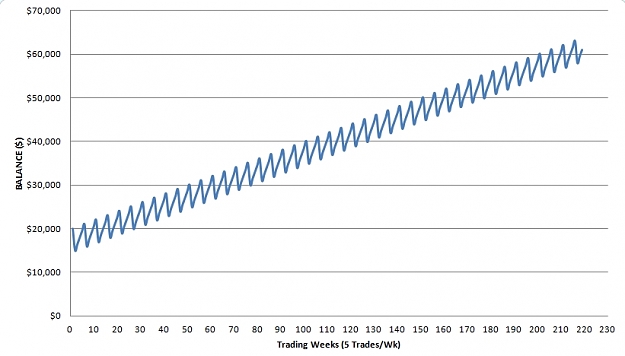

Picture 2: Graph of your account balance over number of weeks trading with the above hypothetical trades.

It shows that with the above scenario, you will more than double your money in 4 years time. Is that return good enough? Does that take too long to achieve? Depends. It all depends on our objectives, risk profile, trading style, etc etc. Thus each of us has got our own work to do.

This illustrates that even with RR less than 1:1, you can still making positive return if you win more than you lose (in this case, I have to reduce my max risk to <1% so that I will still be in the game long enough to cover the loses. On the other hand, I pay the price of being conservative by getting smaller returns. I guess this illustrates also that trading is NOT a getting-rich-quick business). In my case, atm this is what I'm trying to achieve with SonicR system: mastering it so that I can win more time than I lose (acquiring an edge). By back testing & forward/paper trading hopefully I would then generate enough data to analyze my performance with SonicR system.

Just my two cents...

Picture 1: A hypothetical trades journal with:

SL 100 pips

TP 30 pips

Losing/Winning 1:4

Number of trades 5/week

Position size 1/trade

Picture 2: Graph of your account balance over number of weeks trading with the above hypothetical trades.

It shows that with the above scenario, you will more than double your money in 4 years time. Is that return good enough? Does that take too long to achieve? Depends. It all depends on our objectives, risk profile, trading style, etc etc. Thus each of us has got our own work to do.

This illustrates that even with RR less than 1:1, you can still making positive return if you win more than you lose (in this case, I have to reduce my max risk to <1% so that I will still be in the game long enough to cover the loses. On the other hand, I pay the price of being conservative by getting smaller returns. I guess this illustrates also that trading is NOT a getting-rich-quick business). In my case, atm this is what I'm trying to achieve with SonicR system: mastering it so that I can win more time than I lose (acquiring an edge). By back testing & forward/paper trading hopefully I would then generate enough data to analyze my performance with SonicR system.

Just my two cents...

Attached Image(s) (click to enlarge)