DislikedPrice heteroskedasticity is not new, it was discovered in the 80s, if not even earlier. I think you've been reading the wrong studies. Instead of reading papers coming from the economists side, which assume EMH, rational investors and the like, try reading from the quant side, which actually measure the real market and study behavioral patterns.

Today almost all volatility models assume it, with the GARCH model (and it's offspring) being the most famous.

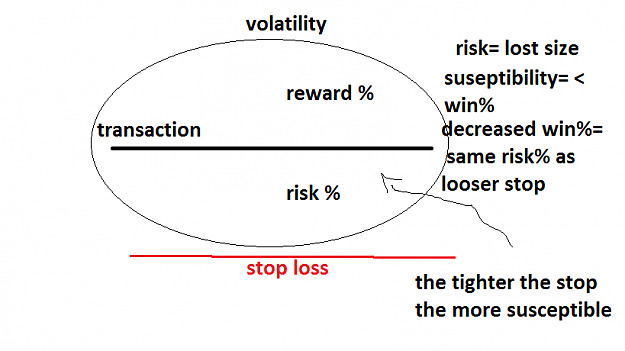

This stuff is very important in the options world, but you can also use it for trading...Ignored

oh ok now I see what you are saying, well in effect volatility cannot be predicted as is a derivative of price variations and unless you can mathematically predict price then they are pretty much correlated, I was aware of this already, but i just didn't tie the idea together.

future volatility is dependent on current volatility for its predictive model, but at the end of the day it ends up being homoskedastic anyway, as it is assumed that a continuation of current variance will continue.

however the idea of heteroskedasticity will have to be taken into account when running risk assessments. which then leads to a more lax view on projected volatility same as price movement, uncertainty forces us to be less precise and more general.

as complicated as the models get it is no better than plain vanilla calculations.

so in fact as you mentioned ATR, Standard Deviations will do to evaluate volatility,

AVT INVENIAM VIAM AVT FACIAM