DislikedI have been testing out strategies in my backtesting program and the results has been showing some drawdowns which I am uncomfortable with.

From anyones experience, is there some ways to decrease DD while increase the annualized return (CAGR%) and also boosting the MAR ratio? Is there a process or approach since I don't want to curve fit my system. Any inputs would be great.Ignored

The actual question is: How to find those events that repeat themselves so you curve fit to the correct parts of the curve.

One answer is to use so much data that the system that actually works always works better than curve fitted system. How to do that is much harder to find than it sounds.

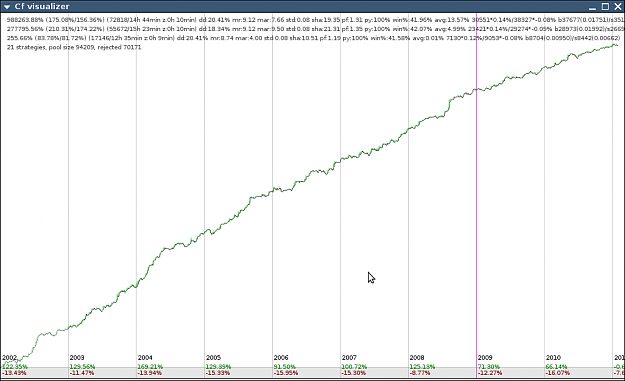

About the dd question, the best way to decrease DD while increasing profit is to use multiple negatively/ low correlated systems. Also remember that DD changes directly when you adjust your trade risk so you might want to compare how different weightings (assuming you have multiple systems) affect your curve.