Let’s not kid ourselves, stagflation is here, and somebody better admit it.

I’ve had a very interesting few days so far out here in Asia. Normally, those that I interact with pay scant regard to the turning of the globe as they are far too busy being wrapped up in the Asian boom. However, on this particular visit, much focus has been paid to the price of breakfast cereal – something completely unrelated to my employment. It is with coincidence that some editorial this week has been focusing upon small ticket items that have seen 50% plus increases in price in the space of a year or so. I am lucky enough – or possibly, a typical male - to not have given attention to the price of cereal, but when it is put in print, one can’t help but notice the size of inflation occurring. For others, with family to feed, print reminders, I assume, are not necessary.

Further reading reminded me of how in Europe, a lot of consumers do not realize that prices for such things as yoghurts may not have increased too dramatically, but that the content of the pot has been reduced. I suppose upon reflection companies are maintaining profit margins by small increases in small ticket items that people will notice less, or using fewer raw materials per item whilst maintaining an expected price by the consumer. My wife has admitted to paying more attention to the price of familiar items, and not the mass as printed on the side of packaging. I then stumbled across some very interesting interviews concerning hyperinflation in the US – and that, ostensibly, the main reason that the US is not already rioting in the streets is that the dollar is considered the safe haven – and is, for the moment, the transaction currency for oil etcetera – thus the FED can print at will.

Without bespoiling this little rant with figures, Ben Bernake, once a staunch critic of the Bank of Japan when it opted to keep interest rates low and thus entered its lost decade, is now pretty much doing the same. I watched one of his question and answer sessions, and, well, he was as vague and cumbersome as Jean-Claude Trichet, or Mervyn King is, and, for me, a liar. A review of the possible reasons for Bernake’s behaviour would require more space than I am willing to give to this forum submission. As was mentioned in some of the aforementioned interviews, if some of the interviewees are to be proved correct, the US may lose currency dominance, and then it is on the same path as Zimbabwe. Dear me…

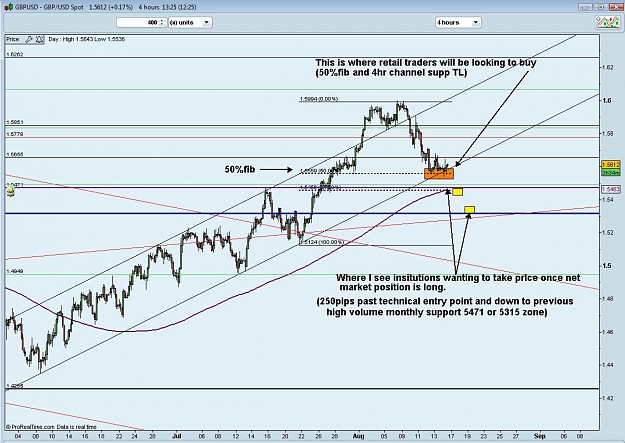

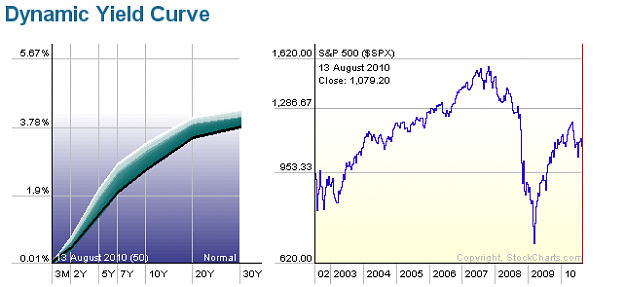

Back to basic sustenance: Taken as a larger consideration, if, globally, people are beginning to realize, and struggle with, the increase in food costs, and are subsequently reducing consumption of even basic sustenance products, what, one has to ask, will be the ramifications? I expect the first to be share price, and as the charts that follow indicate, we may well be making a turn south. Of course, in the case of the FTSE, we have two predictions from leading economists, and which, of course, are diametric; Keith Skeoch anticipates a move up to 6000 for year end, while David Buik points to what is apparently the most feared technical chart pattern, and, dubbed the Hindenburg Omen, will precipitate a drop off the cliff for equities. Either way, I do not forget that 70% of revenue for FTSE companies comes from oversees earnings.

A good chart indication of where we may be going once the traders come back in earnest in mid September is here: http://www.forexfactory.com/showpost...postcount=1950. It would be hard to add to Medici’s presentation.

I did want to include Libor rates, and also make comment upon the DAX etcetera, but Sinner is taking care of that: http://www.forexfactory.com/showpost...&postcount=316.

It is with some alarm that I read that the US, Europe and the UK see export as the way to get us out of all the mess. But, as I have mused upon previously, where, exactly, are we going to export to? China is, by all accounts from respected analysts, contracting and suffering rising inflation and concomitant reluctance by consumers to purchase – and its banks are showing signs of stress. I doubt that the majority of the Asian population is going to be able to afford the products that we wish to export. Add to this the growing fact that Asia is pretty much becoming self reliant on goods ranging from food to mechanics, and we need to dramatically rethink the strategy. I’m not sure the remaining BRICs want our stuff, either. So, the question, as posited previously, is will the elite decide to forego social responsibility, and raise interest rates in order to appease big money? Hmm…

Staying with big money, I was in London recently, and saw a pink Rolls Royce with an Arabic number plate, and what appeared to be a gold-plated Mini, outside of Harrods. But I wasn’t fooled, they are there for the bargains, as on nearly every street that I traversed, shops were conducting sales. Actually, I am seeing sales everywhere I go as of late, and so it is quite obvious that, on the street, at least, the real story is very different from the ‘smoothed’ CPI data.

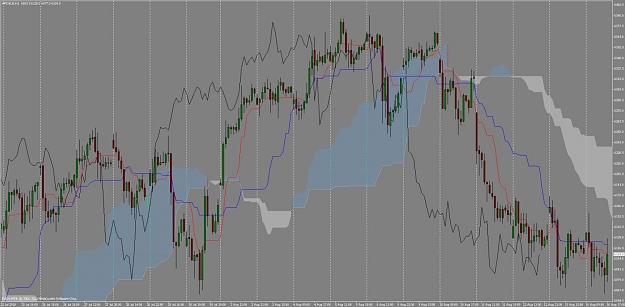

Finally, can anyone remember how in August 2007, we had similar market conditions and change in sentiment from all the movers and shakers from being positive, to negative? Seasonality aside, some analysts contend that chart patterns are similar. Hmm, not sure about that, but my first FTSE chart clearly indicates a compaction of the Guppy profile that has not been seen since August 1989 – as far back as my charts allow. So, I am expecting some bust in the coming weeks/months. If I was a gambler, I would say south.

I’ve had a very interesting few days so far out here in Asia. Normally, those that I interact with pay scant regard to the turning of the globe as they are far too busy being wrapped up in the Asian boom. However, on this particular visit, much focus has been paid to the price of breakfast cereal – something completely unrelated to my employment. It is with coincidence that some editorial this week has been focusing upon small ticket items that have seen 50% plus increases in price in the space of a year or so. I am lucky enough – or possibly, a typical male - to not have given attention to the price of cereal, but when it is put in print, one can’t help but notice the size of inflation occurring. For others, with family to feed, print reminders, I assume, are not necessary.

Further reading reminded me of how in Europe, a lot of consumers do not realize that prices for such things as yoghurts may not have increased too dramatically, but that the content of the pot has been reduced. I suppose upon reflection companies are maintaining profit margins by small increases in small ticket items that people will notice less, or using fewer raw materials per item whilst maintaining an expected price by the consumer. My wife has admitted to paying more attention to the price of familiar items, and not the mass as printed on the side of packaging. I then stumbled across some very interesting interviews concerning hyperinflation in the US – and that, ostensibly, the main reason that the US is not already rioting in the streets is that the dollar is considered the safe haven – and is, for the moment, the transaction currency for oil etcetera – thus the FED can print at will.

Without bespoiling this little rant with figures, Ben Bernake, once a staunch critic of the Bank of Japan when it opted to keep interest rates low and thus entered its lost decade, is now pretty much doing the same. I watched one of his question and answer sessions, and, well, he was as vague and cumbersome as Jean-Claude Trichet, or Mervyn King is, and, for me, a liar. A review of the possible reasons for Bernake’s behaviour would require more space than I am willing to give to this forum submission. As was mentioned in some of the aforementioned interviews, if some of the interviewees are to be proved correct, the US may lose currency dominance, and then it is on the same path as Zimbabwe. Dear me…

Back to basic sustenance: Taken as a larger consideration, if, globally, people are beginning to realize, and struggle with, the increase in food costs, and are subsequently reducing consumption of even basic sustenance products, what, one has to ask, will be the ramifications? I expect the first to be share price, and as the charts that follow indicate, we may well be making a turn south. Of course, in the case of the FTSE, we have two predictions from leading economists, and which, of course, are diametric; Keith Skeoch anticipates a move up to 6000 for year end, while David Buik points to what is apparently the most feared technical chart pattern, and, dubbed the Hindenburg Omen, will precipitate a drop off the cliff for equities. Either way, I do not forget that 70% of revenue for FTSE companies comes from oversees earnings.

A good chart indication of where we may be going once the traders come back in earnest in mid September is here: http://www.forexfactory.com/showpost...postcount=1950. It would be hard to add to Medici’s presentation.

I did want to include Libor rates, and also make comment upon the DAX etcetera, but Sinner is taking care of that: http://www.forexfactory.com/showpost...&postcount=316.

It is with some alarm that I read that the US, Europe and the UK see export as the way to get us out of all the mess. But, as I have mused upon previously, where, exactly, are we going to export to? China is, by all accounts from respected analysts, contracting and suffering rising inflation and concomitant reluctance by consumers to purchase – and its banks are showing signs of stress. I doubt that the majority of the Asian population is going to be able to afford the products that we wish to export. Add to this the growing fact that Asia is pretty much becoming self reliant on goods ranging from food to mechanics, and we need to dramatically rethink the strategy. I’m not sure the remaining BRICs want our stuff, either. So, the question, as posited previously, is will the elite decide to forego social responsibility, and raise interest rates in order to appease big money? Hmm…

Staying with big money, I was in London recently, and saw a pink Rolls Royce with an Arabic number plate, and what appeared to be a gold-plated Mini, outside of Harrods. But I wasn’t fooled, they are there for the bargains, as on nearly every street that I traversed, shops were conducting sales. Actually, I am seeing sales everywhere I go as of late, and so it is quite obvious that, on the street, at least, the real story is very different from the ‘smoothed’ CPI data.

Finally, can anyone remember how in August 2007, we had similar market conditions and change in sentiment from all the movers and shakers from being positive, to negative? Seasonality aside, some analysts contend that chart patterns are similar. Hmm, not sure about that, but my first FTSE chart clearly indicates a compaction of the Guppy profile that has not been seen since August 1989 – as far back as my charts allow. So, I am expecting some bust in the coming weeks/months. If I was a gambler, I would say south.

Attached Image(s) (click to enlarge)

Author of: For Pip's Sake! (Available at Amazon... :-) )