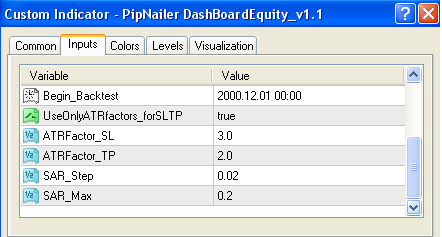

If we take the values for SL and TP as 'ATR * factor', the results changed (please check also other factor combinations...).

(ATR period = 21)

Just a remark:

Begin_Backtest is setted to '2000.12.01', but you can see the real begin of trades ('FirstTradeDate') in the TradeSimulator. This is for the most time frames higher!

.

(ATR period = 21)

Just a remark:

Begin_Backtest is setted to '2000.12.01', but you can see the real begin of trades ('FirstTradeDate') in the TradeSimulator. This is for the most time frames higher!

.

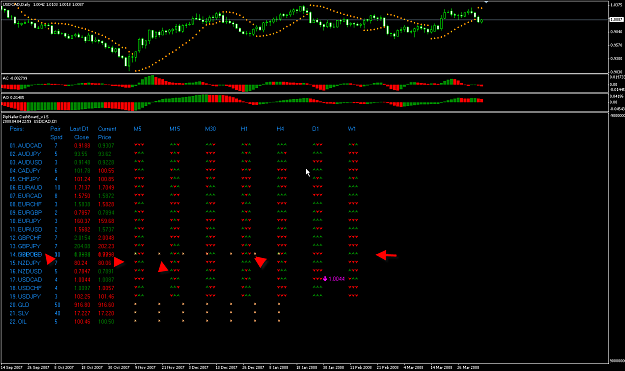

Attached Image (click to enlarge)

Attached Image