DislikedWow, It looks like you could be on to something here. This is very interesting. Did you enter all these trades by hand or did you use some sort of DDE fill? If you entered them by hand, it would be obvious that you actually checked each one for validity.Ignored

Hi smjones -

Sorry, I'm not sure what you mean by DDE.

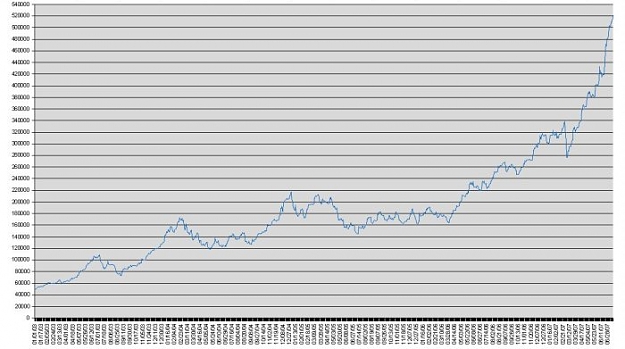

The historical study I did was on a spreadsheet with daily open/high/low/close prices. Obviously, the results are theoretical, since they are all based on the exact close/open price. In reality, this won't happen and the actual returns will vary. However, if I make my trades consistently at the same time every day near the close or open, then on average my prices should not be far from the actual close/open.

Also, I should point out that I have not deducted spreads/commissions, so this will reduce the real-world returns as well. The spreads on these particular pairs are not huge, but over more than 1100 days, this will still have an impact. I would estimate that spreads would reduce the theoretical monthly returns by 10-20 pips on average, so that the real-world results without any optimization might be around 280-290 pips.

I don't think I actually answered your question, because I didn't understand it. But if you can clarify for me, I will try again :-)