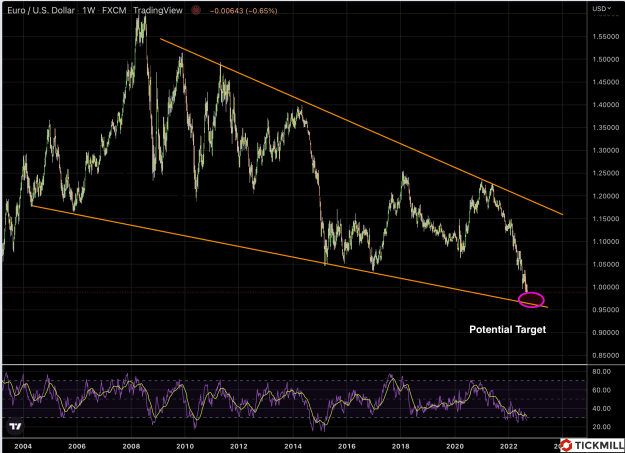

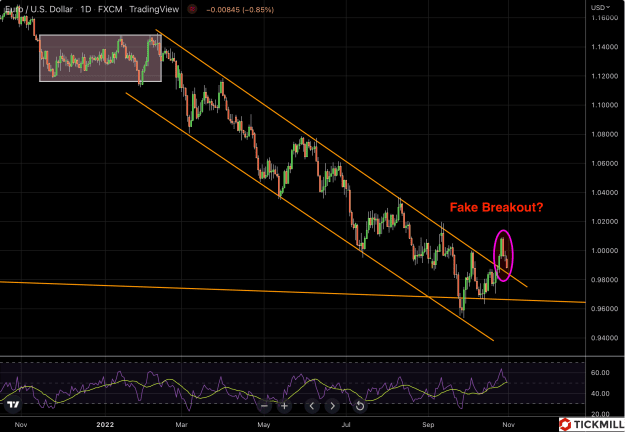

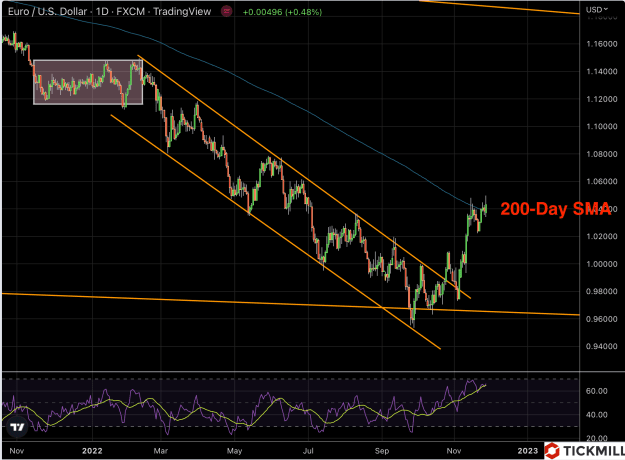

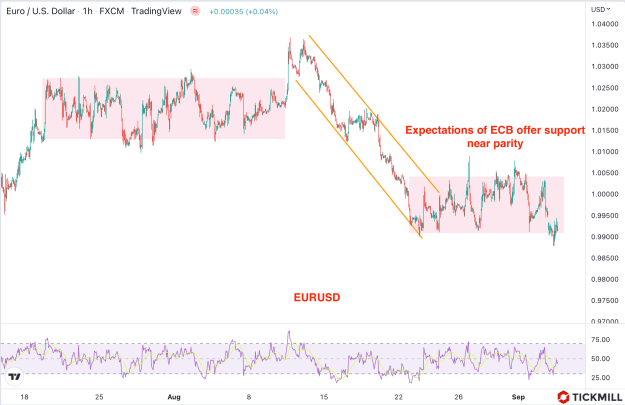

EURUSD remains glued to parity on expectations of uber-hawkish ECB this week

European asset markets started the week with a fresh round of downside as Gazprom said gas supplies via Nord Stream 1 pipeline would be suspended indefinitely. The currencies of the European continent expectedly came under pressure and the fiscal aid packages announced by the European governments are unlikely to reverse the bearish trend.

The end of last week looked encouraging after release of US labor market data, however, the announcement of Gazprom late in the evening that the gas supply via Nord Stream is being frozen for an indefinite period reversed the risk-on move. And although European countries have made some progress in filling gas storage facilities in preparation for winter, the signal of a complete shutdown of supplies means that the way up for gas prices is open, i.e. new shocks in the market are inevitable.

Over the weekend, the authorities in Sweden and Finland announced liquidity guarantees for large utilities companies, signaling that they do not want the fire in the energy market to spread to the financial sector. Indicators of financial stress in the EU, such as the spread between the interbank lending rate (Euribor) and

ESTR does not yet indicate an increase in risks in the market, being at a relatively low level. However, it is clear that international capital will rather try to avoid European assets.

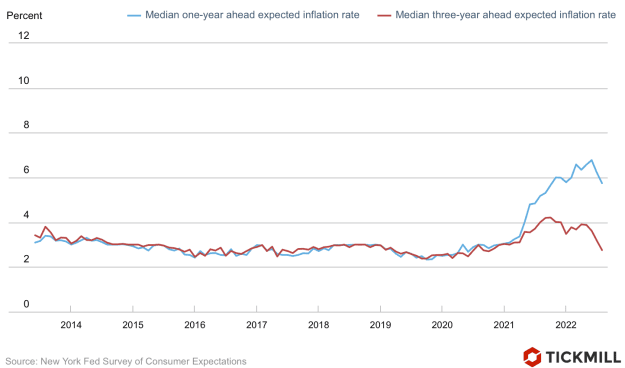

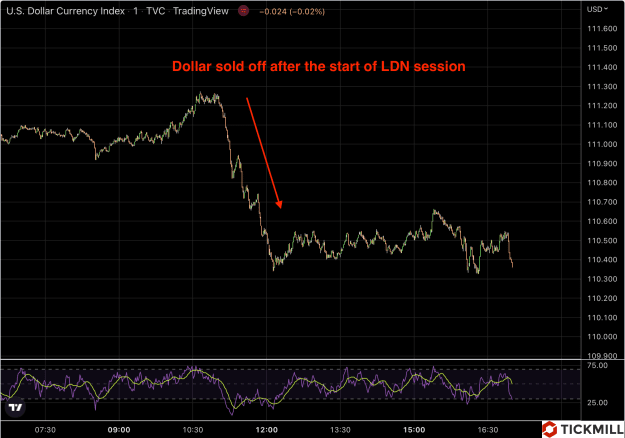

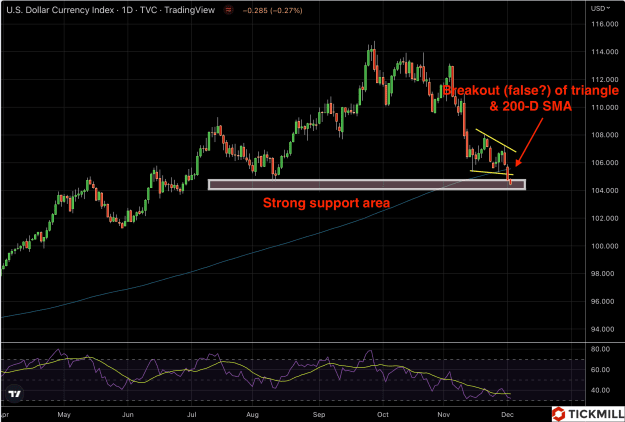

Risk-free fixed income instruments, i.e. Treasuries are now offering 2.3%, while the energy risks for the US economy are low, due to independence from supplies from foreign markets, so it is clear where the focus of investors will be now. From here we can expect a stable investment-motivated demand for the dollar. The Japanese yen has lost the status of a safe haven, as the energy crisis has taken away from Japan the main argument why it is worth buying in yen at a time of instability - a trade surplus due to the rapid growth in the cost of imports and weakening of exports.

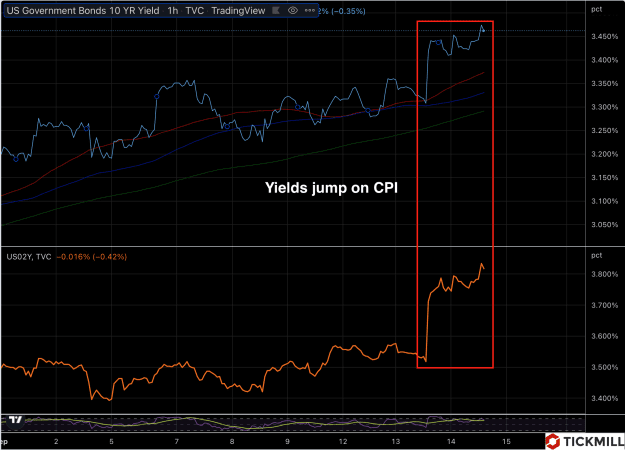

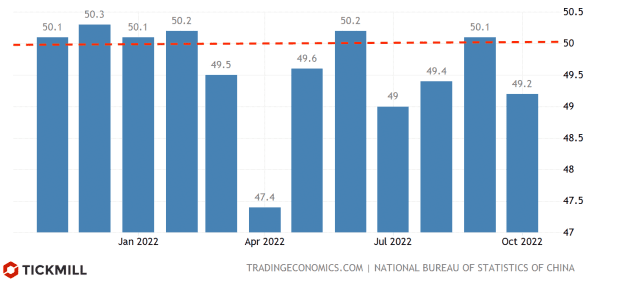

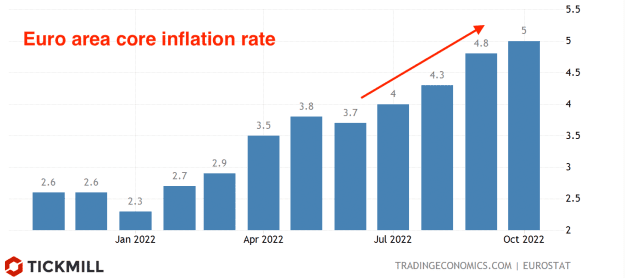

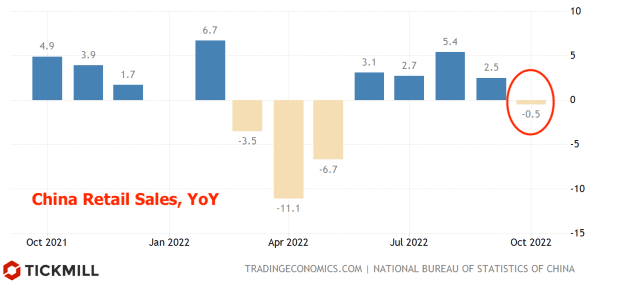

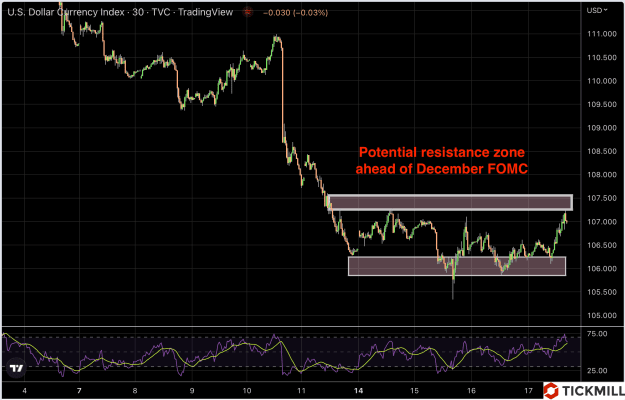

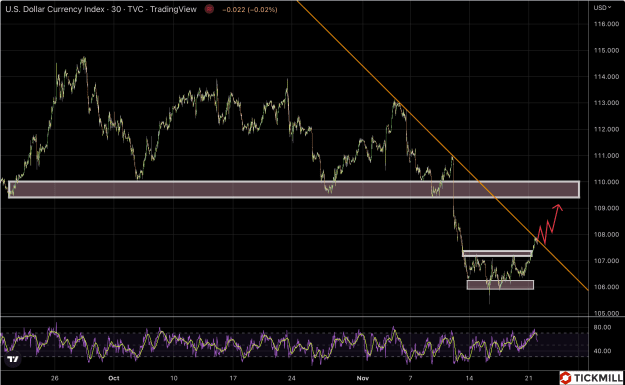

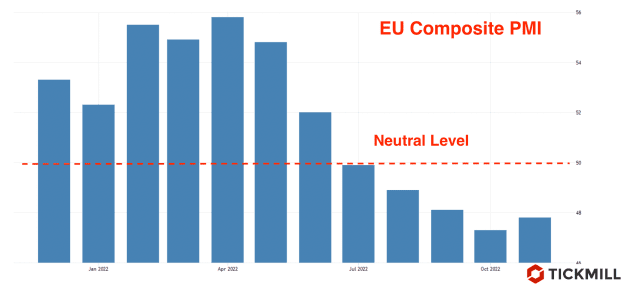

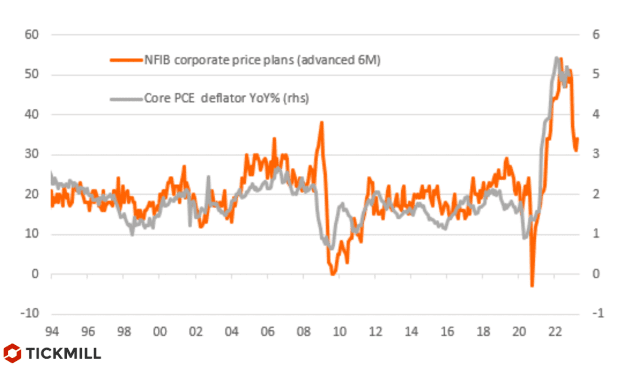

This week there are several significant events that can cause volatility in the market. These are the RBA meeting on Tuesday, speeches by a number of EU, UK and US central bank officials on Wednesday, the Bank of Canada meeting on the same day, the ECB meeting on Thursday, and inflation data in China on Friday. The ECB meeting deserves special attention as the market is discussing a possible rate hike of 75 basis points, which represents a very aggressive pace of tightening. The expectations of this outcome have not yet been fully factored in the market, therefore, if this outcome is realized, we can expect a positive reaction from EURUSD. A rate hike of 50 basis points is likely to disappoint, causing a fairly large decline (0.965-0.960):

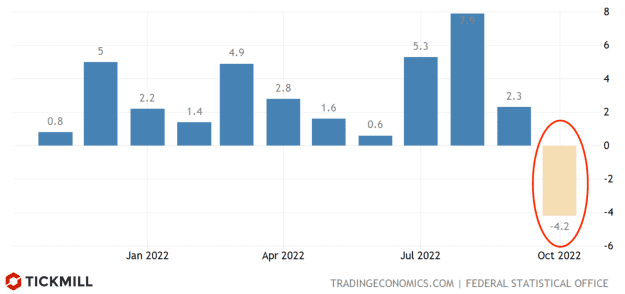

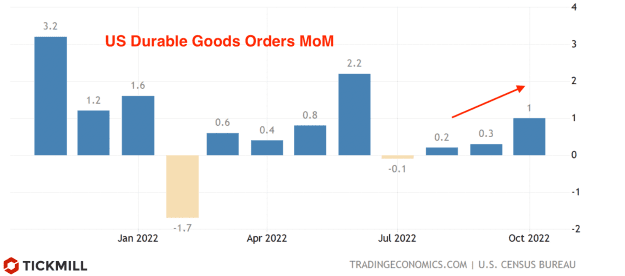

Germany's attempts to help the economy through a fiscal package of 2% went almost unnoticed by the market, since compared to the package of 15% of GDP at the height of the pandemic, this is a very insignificant amount.

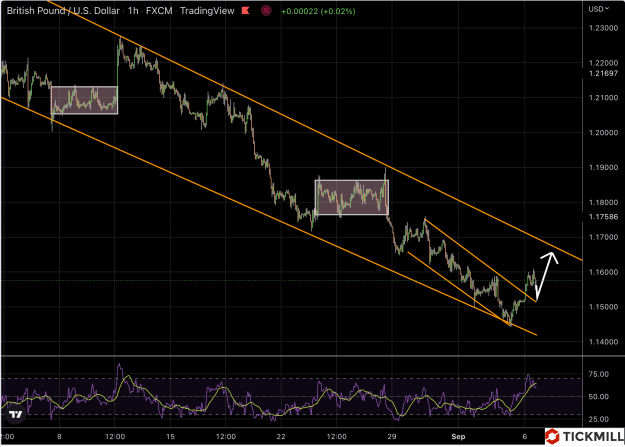

GBPUSD fell below 1.15 and the March 2020 low was already in sight, when the rate was 1.1410 at the lowest point. Today the market will follow the appointment of a new prime minister - most likely it will be Liz Truss. She previously spoke of a £100bn fiscal bailout. In moments of crisis, loose monetary policy has a beneficial effect on the exchange rate, so now, if expectations of rate hikes rise due to the fact that the government with fiscal support has entered the game, they can, on the contrary, weaken the pound. In the near-term, from the point of view of technical analysis, a test of the March low (1.141) is possible, followed by a rebound to 1.15-1.1550:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

European asset markets started the week with a fresh round of downside as Gazprom said gas supplies via Nord Stream 1 pipeline would be suspended indefinitely. The currencies of the European continent expectedly came under pressure and the fiscal aid packages announced by the European governments are unlikely to reverse the bearish trend.

The end of last week looked encouraging after release of US labor market data, however, the announcement of Gazprom late in the evening that the gas supply via Nord Stream is being frozen for an indefinite period reversed the risk-on move. And although European countries have made some progress in filling gas storage facilities in preparation for winter, the signal of a complete shutdown of supplies means that the way up for gas prices is open, i.e. new shocks in the market are inevitable.

Over the weekend, the authorities in Sweden and Finland announced liquidity guarantees for large utilities companies, signaling that they do not want the fire in the energy market to spread to the financial sector. Indicators of financial stress in the EU, such as the spread between the interbank lending rate (Euribor) and

ESTR does not yet indicate an increase in risks in the market, being at a relatively low level. However, it is clear that international capital will rather try to avoid European assets.

Risk-free fixed income instruments, i.e. Treasuries are now offering 2.3%, while the energy risks for the US economy are low, due to independence from supplies from foreign markets, so it is clear where the focus of investors will be now. From here we can expect a stable investment-motivated demand for the dollar. The Japanese yen has lost the status of a safe haven, as the energy crisis has taken away from Japan the main argument why it is worth buying in yen at a time of instability - a trade surplus due to the rapid growth in the cost of imports and weakening of exports.

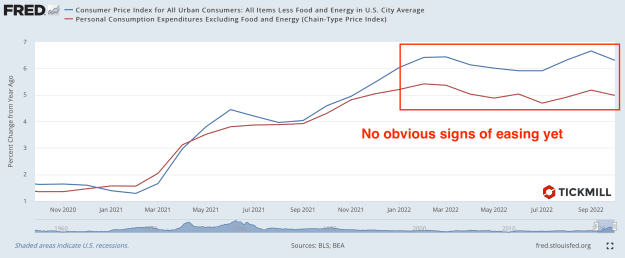

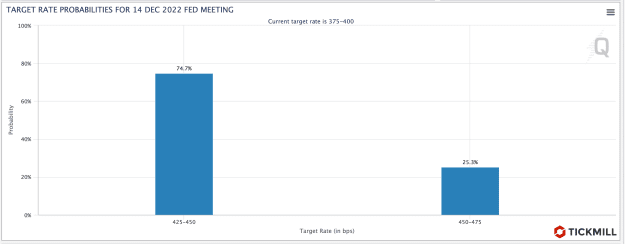

This week there are several significant events that can cause volatility in the market. These are the RBA meeting on Tuesday, speeches by a number of EU, UK and US central bank officials on Wednesday, the Bank of Canada meeting on the same day, the ECB meeting on Thursday, and inflation data in China on Friday. The ECB meeting deserves special attention as the market is discussing a possible rate hike of 75 basis points, which represents a very aggressive pace of tightening. The expectations of this outcome have not yet been fully factored in the market, therefore, if this outcome is realized, we can expect a positive reaction from EURUSD. A rate hike of 50 basis points is likely to disappoint, causing a fairly large decline (0.965-0.960):

Attached Image (click to enlarge)

Germany's attempts to help the economy through a fiscal package of 2% went almost unnoticed by the market, since compared to the package of 15% of GDP at the height of the pandemic, this is a very insignificant amount.

GBPUSD fell below 1.15 and the March 2020 low was already in sight, when the rate was 1.1410 at the lowest point. Today the market will follow the appointment of a new prime minister - most likely it will be Liz Truss. She previously spoke of a £100bn fiscal bailout. In moments of crisis, loose monetary policy has a beneficial effect on the exchange rate, so now, if expectations of rate hikes rise due to the fact that the government with fiscal support has entered the game, they can, on the contrary, weaken the pound. In the near-term, from the point of view of technical analysis, a test of the March low (1.141) is possible, followed by a rebound to 1.15-1.1550:

Attached Image (click to enlarge)

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.