Hey,

I haven't posted here in years. I have gone through the ups and downs of trading for nearly a decade (mostly downs). The last couple of months seem to me like I've figured out a way to be consistent in my returns and method. I want to share the method. I think if some people joined this method, we can quickly gather enough data to make sure this method is robust for not just a year but for many years to come. I'll spare you the details of how I got here.

This method is about not blowing up your account and gives an actionable plan to "cutting your losses early". If you expect to make a living from this in 6 months time you can stop reading now.

There's 3 sections to this, which I scatter over 3 posts.

Some of this may seem wordy and I'm not great at explaining things.

1) Money/trade management - Losing money smarter

2) Charting analysis - Not losing money quickly

3) Collecting data together

TLDR;

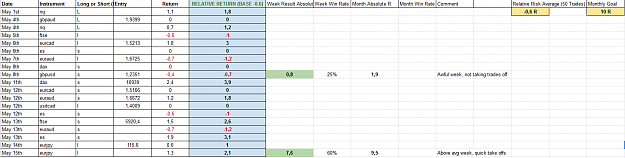

Found a way that's been making me money for a while and I think it's solid. Would like others to join the concept to prove its robustness with varying entry parameters. Reduce stops on every trade to an average of -0.6R. Make more money than lose on average. Try to make 10R a month. Technical analysis is a waste of time. Go with HTF momentum trends. Use momentum entries in the most volatile hours of the day (London Open and NY Open for 2-2.5 hrs each) and try your best to be consistent in reducing stops and don't go for home runs. Started a spreadsheet to track this method's performance with other people. Let me know if you want to start your own sheet in this file:

https://docs.google.com/spreadsheets...it?usp=sharing

-------------------------------------------------------------------

1) Money management - Losing Money Smarter

To kick things off, the money management part is the most important bit of it all.

The way I calculate losers and winners is based on risk and return. A lot has been written on this topic, so I don't think it's necessary to repeat it all. If this is new to you, look into Van Tharp or just google it. To sum it up, if you consistently risk $1 a trade, your aim is to return a multiple > 1 of your trades on average. Easier said than done. What my method does is modify this logic just a little bit (and its hardly revolutionary).

Assume the risk for a trade is consistently $1 and my targeted multiple is 1.5R. This means I now risk $1 to make $1.50 and in theory, if you don't risk a large % of your account per trade, this could be enough to significantly reduce your risk of ruin and be profitable on < 40% win rates. Weird that I still was never able to make money consistently every month with this. That's because it's hard to reliably assess the market will move an absolute of 1.5R in my favor.

This method deals with that problem. Instead of focusing on absolute risk and return, I now focus on relative risk and return.

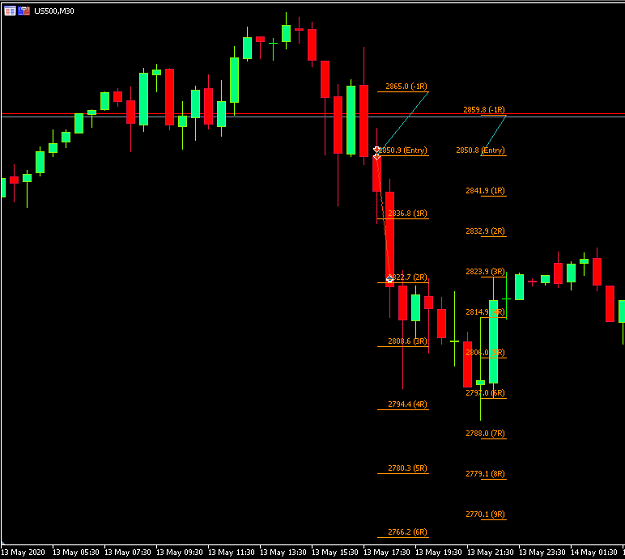

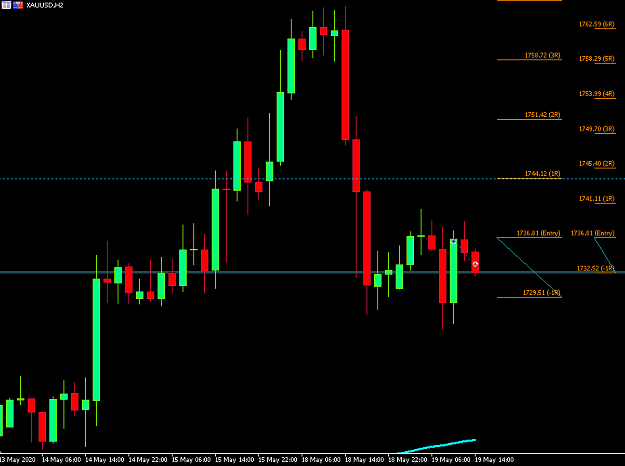

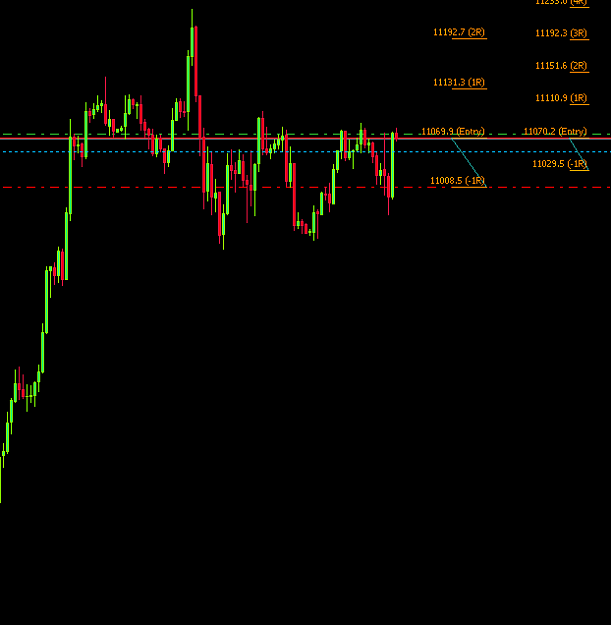

To continue the example from above, the way it works is that my absolute risk of $1 (-1R) basically means that I have a stop loss in place, and I accept my trade just didn't work out once it hits -1R. However, if I entered with a full $1 risk, and consistently reduced my stop size on virtually every trade to a figure less than $1 before being stopped, then I would consistently lose less than $1 based on the relative -1R. Also, I wouldn't need to rely on the market moving an absolute of 1.5R in my favor anymore to achieve the same relative return multiple of 1.5R. That's the underlying logic of my method.

Consider this scenario - On average:

I enter a trade that has a stop of 30 pips.

My absolute risk is -1R. -30 pips.

I reduce my stop to -15 pips.

My absolute risk is for a stop is now -0.5R. -15 pips. My relative risk is -1r. -15 Pips.

The trade moves 25 Pips in my favor and I take it off. My absolute return is garbage at 0.8R at a static stop of -1R. I'd need a win rate > 60% to make this sustainable.

Considering I move my stop on average to -0.5R, my relative return is 1.7R. This way I don't need to rely on absolute moves.

There's a few more details to this simplified example and if you're skeptical (which you should be), go ahead and ask me.

The biggest question that comes up is how can you guarantee you will reduce your stop to -0.5R on average? I'll try my best to discuss this in the second section.

I feel like this should explain the money management part of this method but I'll be happy to edit this post over time if you think this doesn't make sense. Ask questions or tell me if you think it's unclear, so that people reading this for the first time can get the hang of it quickly. There's clearly tons of scenarios that can unfold, so if you think something's missing, let me know.

I haven't posted here in years. I have gone through the ups and downs of trading for nearly a decade (mostly downs). The last couple of months seem to me like I've figured out a way to be consistent in my returns and method. I want to share the method. I think if some people joined this method, we can quickly gather enough data to make sure this method is robust for not just a year but for many years to come. I'll spare you the details of how I got here.

This method is about not blowing up your account and gives an actionable plan to "cutting your losses early". If you expect to make a living from this in 6 months time you can stop reading now.

There's 3 sections to this, which I scatter over 3 posts.

Some of this may seem wordy and I'm not great at explaining things.

1) Money/trade management - Losing money smarter

2) Charting analysis - Not losing money quickly

3) Collecting data together

TLDR;

Found a way that's been making me money for a while and I think it's solid. Would like others to join the concept to prove its robustness with varying entry parameters. Reduce stops on every trade to an average of -0.6R. Make more money than lose on average. Try to make 10R a month. Technical analysis is a waste of time. Go with HTF momentum trends. Use momentum entries in the most volatile hours of the day (London Open and NY Open for 2-2.5 hrs each) and try your best to be consistent in reducing stops and don't go for home runs. Started a spreadsheet to track this method's performance with other people. Let me know if you want to start your own sheet in this file:

https://docs.google.com/spreadsheets...it?usp=sharing

-------------------------------------------------------------------

1) Money management - Losing Money Smarter

To kick things off, the money management part is the most important bit of it all.

The way I calculate losers and winners is based on risk and return. A lot has been written on this topic, so I don't think it's necessary to repeat it all. If this is new to you, look into Van Tharp or just google it. To sum it up, if you consistently risk $1 a trade, your aim is to return a multiple > 1 of your trades on average. Easier said than done. What my method does is modify this logic just a little bit (and its hardly revolutionary).

Assume the risk for a trade is consistently $1 and my targeted multiple is 1.5R. This means I now risk $1 to make $1.50 and in theory, if you don't risk a large % of your account per trade, this could be enough to significantly reduce your risk of ruin and be profitable on < 40% win rates. Weird that I still was never able to make money consistently every month with this. That's because it's hard to reliably assess the market will move an absolute of 1.5R in my favor.

This method deals with that problem. Instead of focusing on absolute risk and return, I now focus on relative risk and return.

To continue the example from above, the way it works is that my absolute risk of $1 (-1R) basically means that I have a stop loss in place, and I accept my trade just didn't work out once it hits -1R. However, if I entered with a full $1 risk, and consistently reduced my stop size on virtually every trade to a figure less than $1 before being stopped, then I would consistently lose less than $1 based on the relative -1R. Also, I wouldn't need to rely on the market moving an absolute of 1.5R in my favor anymore to achieve the same relative return multiple of 1.5R. That's the underlying logic of my method.

Consider this scenario - On average:

I enter a trade that has a stop of 30 pips.

My absolute risk is -1R. -30 pips.

I reduce my stop to -15 pips.

My absolute risk is for a stop is now -0.5R. -15 pips. My relative risk is -1r. -15 Pips.

The trade moves 25 Pips in my favor and I take it off. My absolute return is garbage at 0.8R at a static stop of -1R. I'd need a win rate > 60% to make this sustainable.

Considering I move my stop on average to -0.5R, my relative return is 1.7R. This way I don't need to rely on absolute moves.

There's a few more details to this simplified example and if you're skeptical (which you should be), go ahead and ask me.

The biggest question that comes up is how can you guarantee you will reduce your stop to -0.5R on average? I'll try my best to discuss this in the second section.

I feel like this should explain the money management part of this method but I'll be happy to edit this post over time if you think this doesn't make sense. Ask questions or tell me if you think it's unclear, so that people reading this for the first time can get the hang of it quickly. There's clearly tons of scenarios that can unfold, so if you think something's missing, let me know.