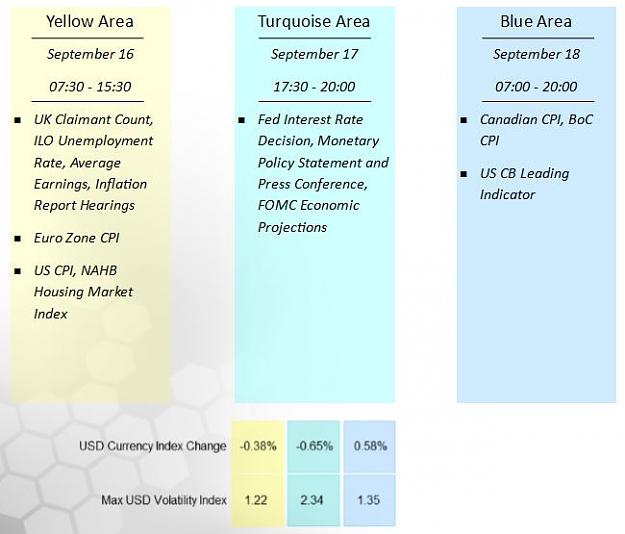

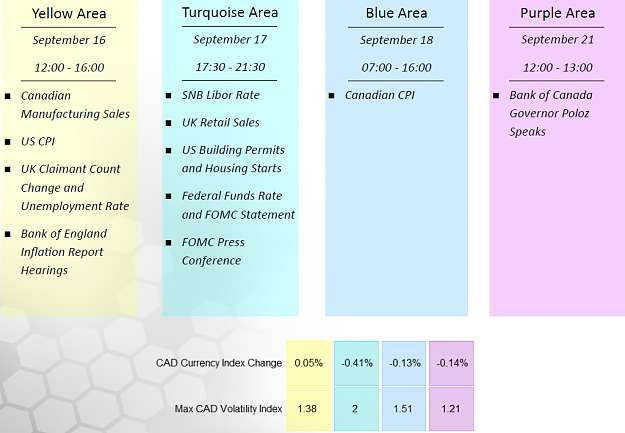

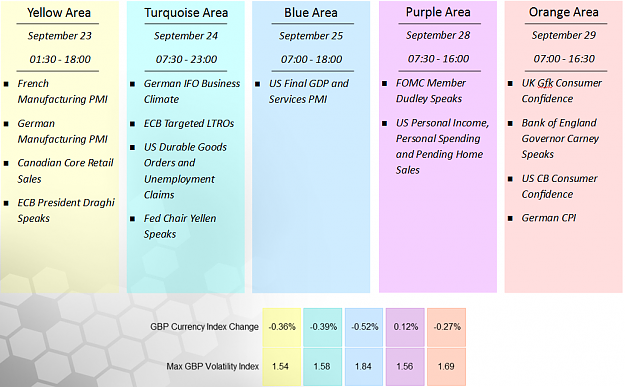

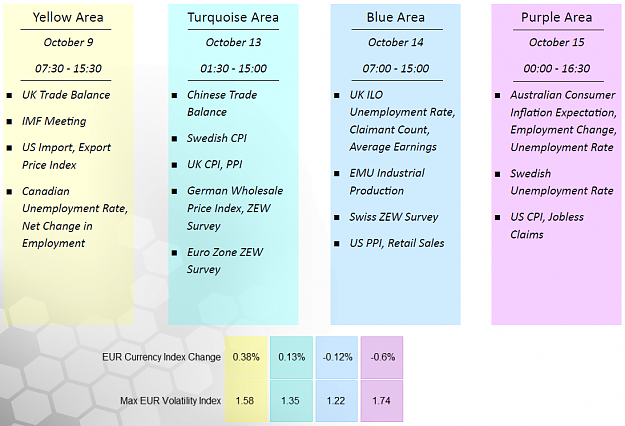

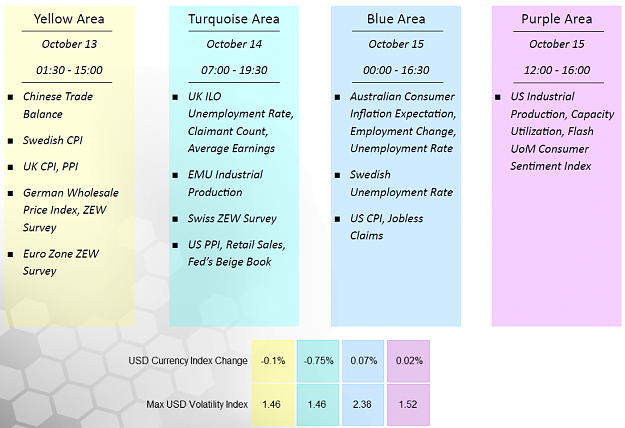

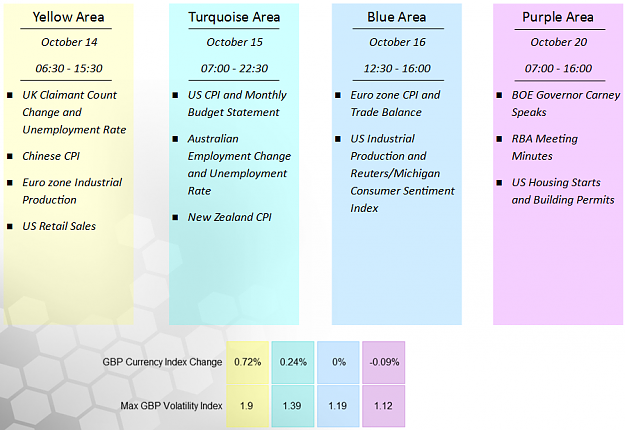

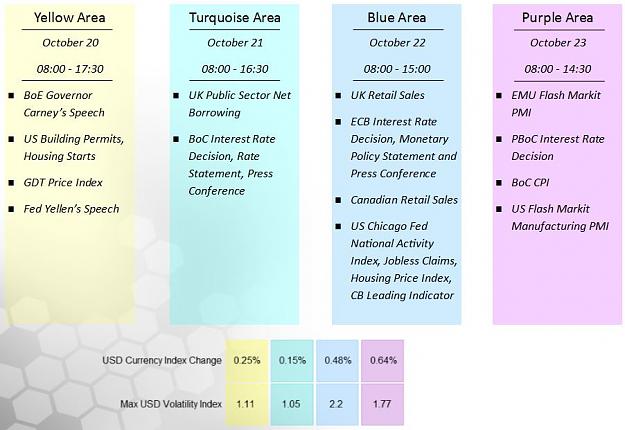

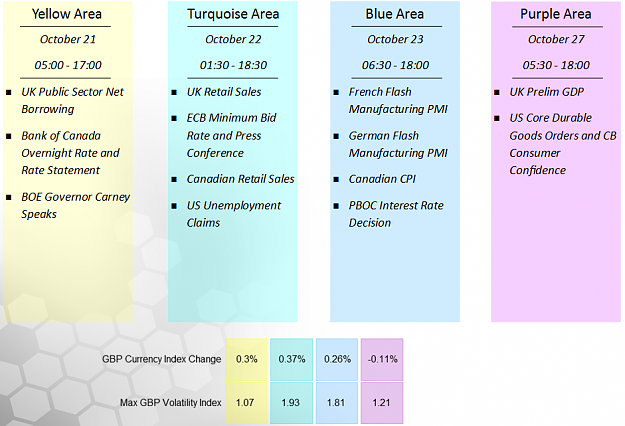

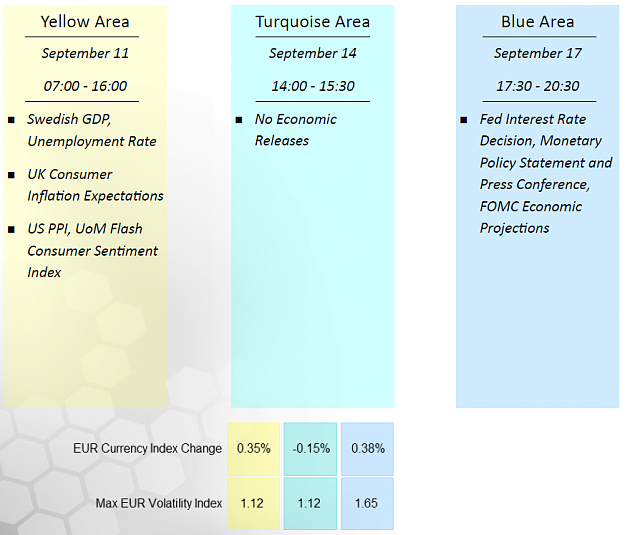

Highlights of the latest Market Research release on EUR.

Full research available here.

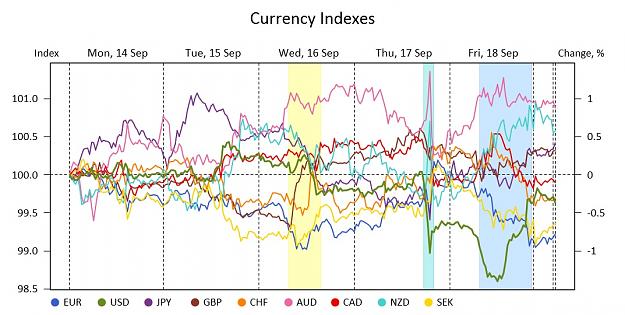

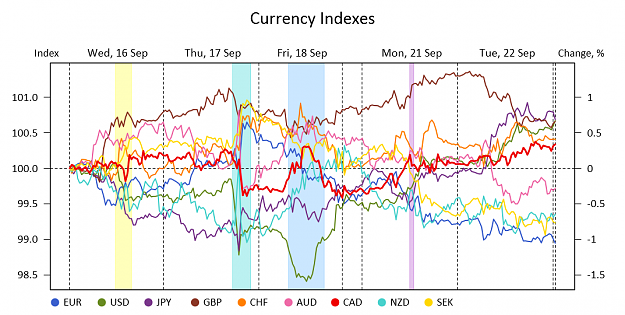

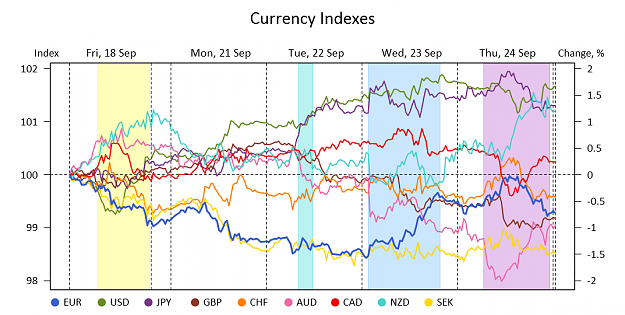

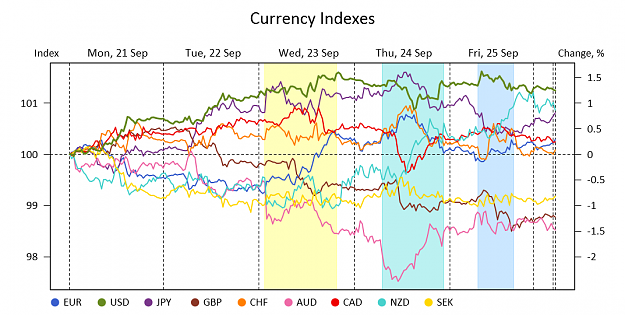

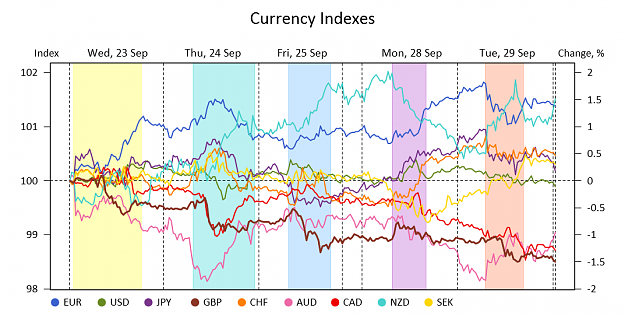

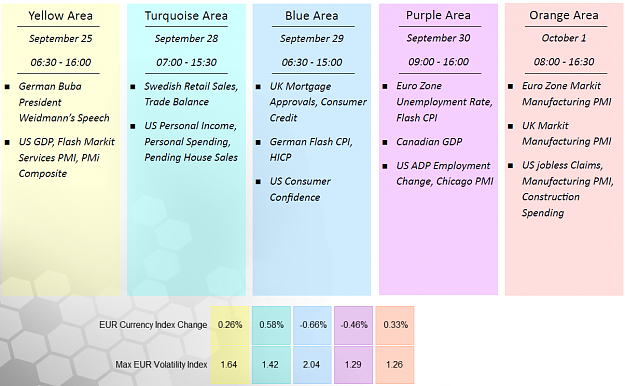

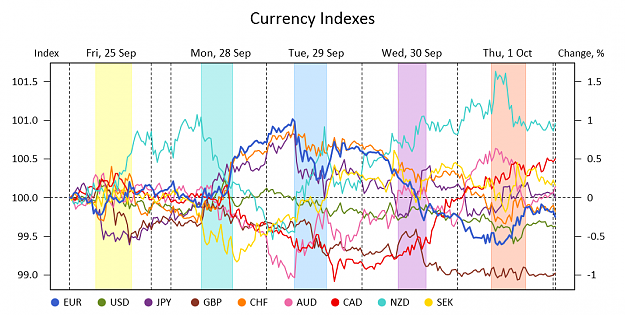

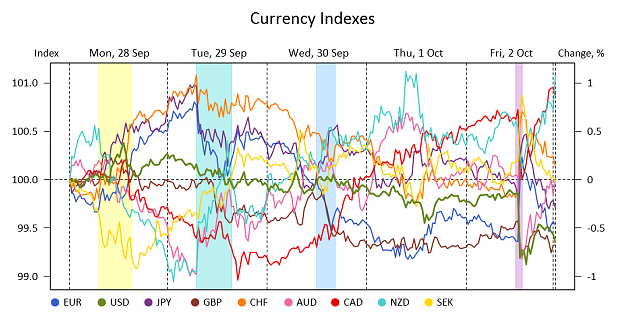

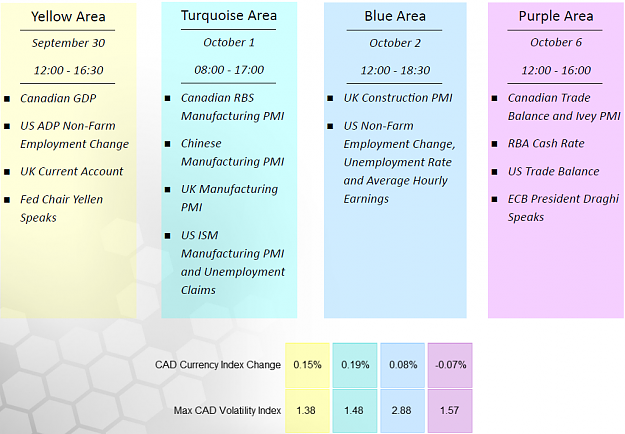

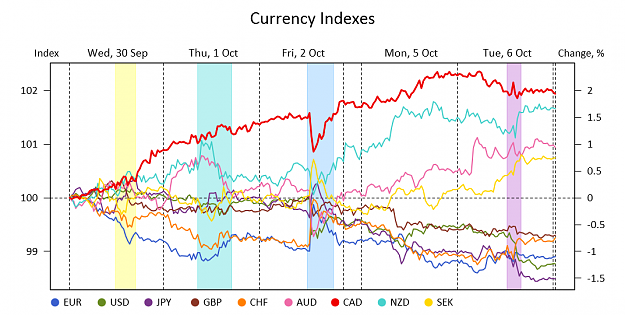

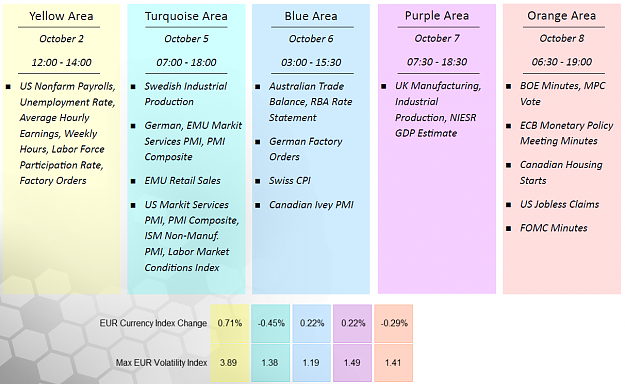

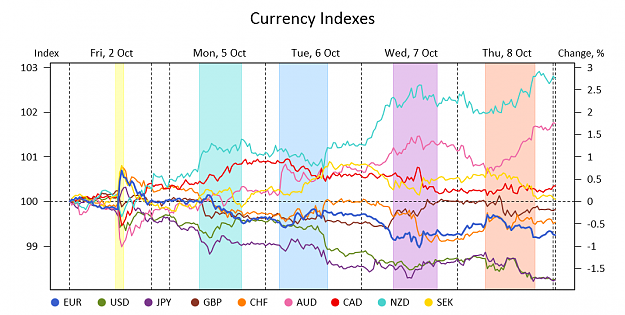

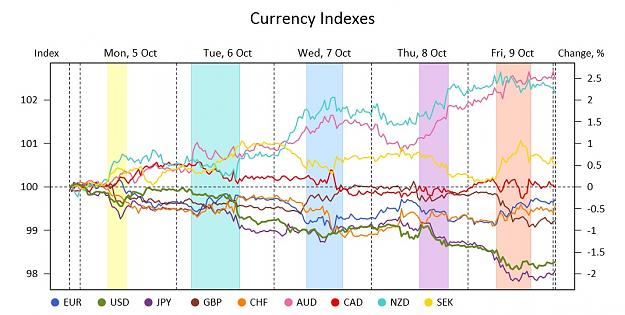

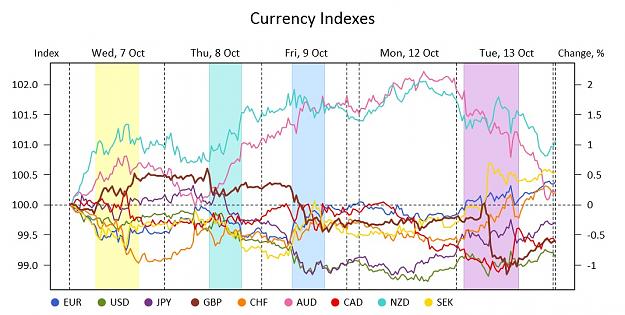

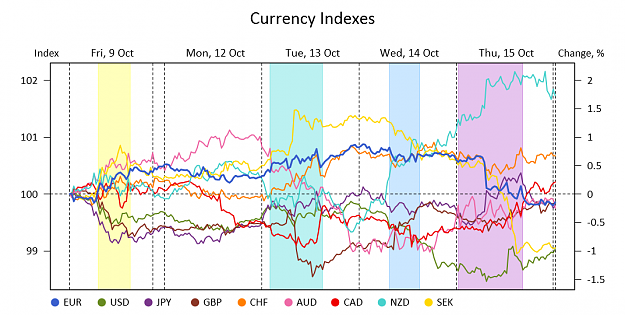

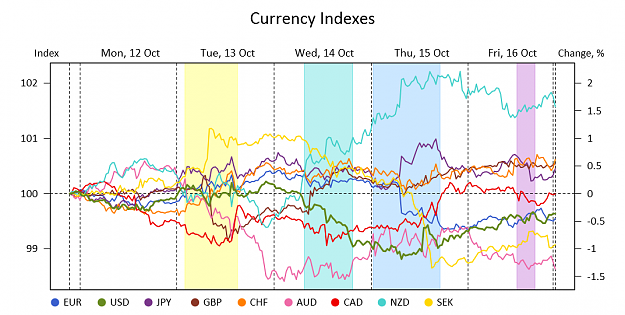

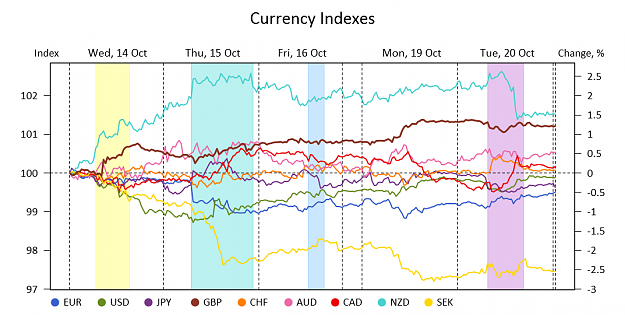

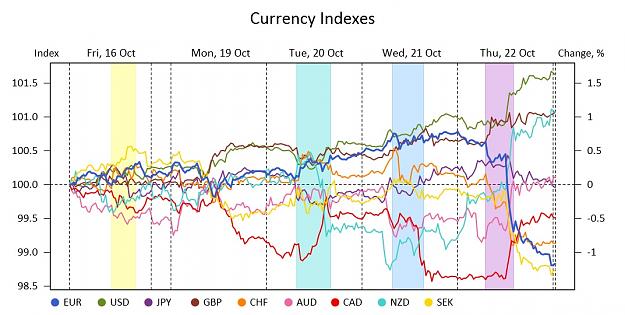

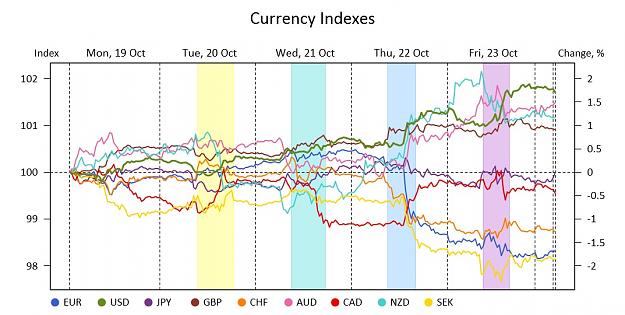

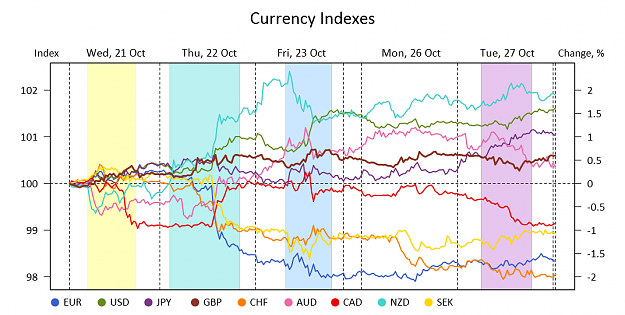

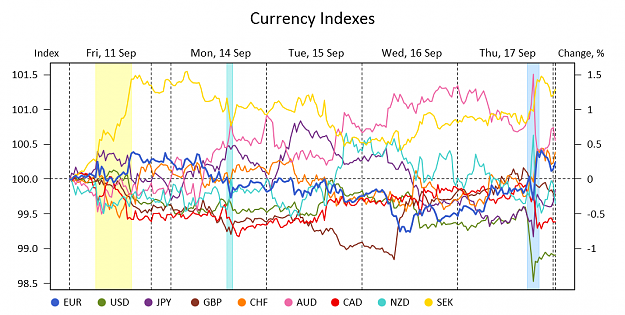

The past period was all about sharp moves, as most of the indexes changed their positions abruptly and otherwise wavered around the reached levels. The main shifts took place on Thursday, when all eyes were on the Fed and its interest rate decision. The USD Index started to lose points a couple of hours before the announcement, and, after the long-awaited hike was pushed further towards the end of the year, went into a dive to the period’s absolute low of 98.5. The Pacific indexes produced the sharpest surges, but also went into the deepest dives after the press conference, yielding more than they managed to gain. Meanwhile, the krona’s gauge, which showed the week’s broadest surge as it burst above its peers with the improved GDP and unemployment data released on Friday, was gaining ground all throughout the blue area, surpassing its Australian counterpart and posting the period’s greatest gain. The only index to show virtually no reaction to Thursday’s events was the pound’s measure, which made its big move amid solid jobs report on Wednesday and kept close to the baseline during the last day of the period.

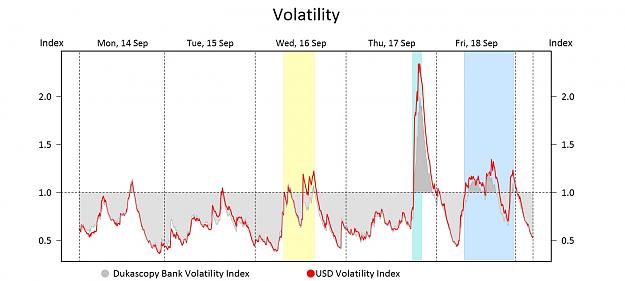

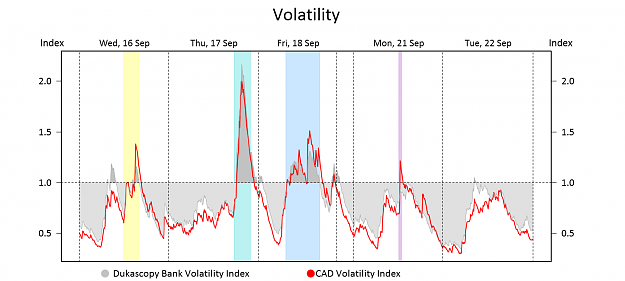

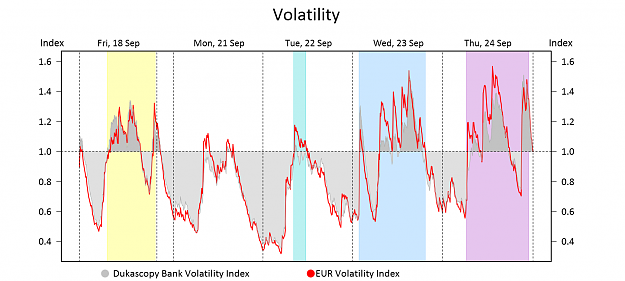

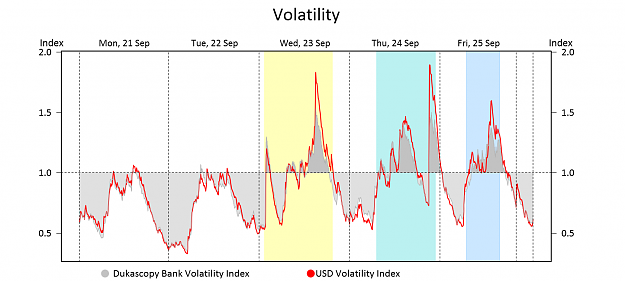

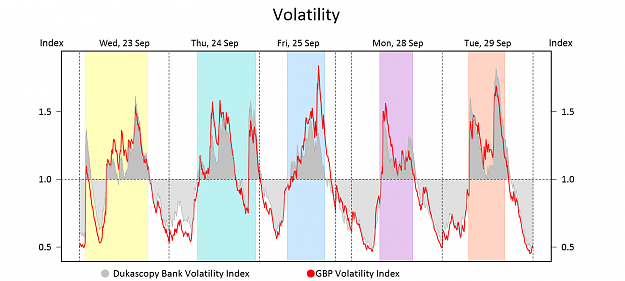

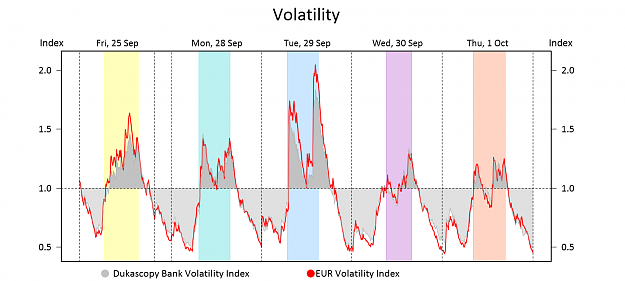

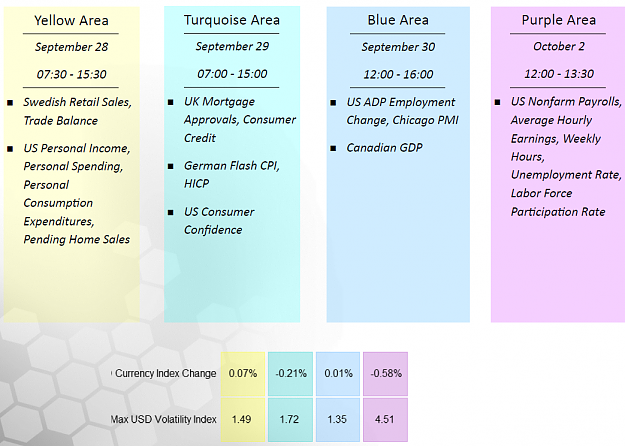

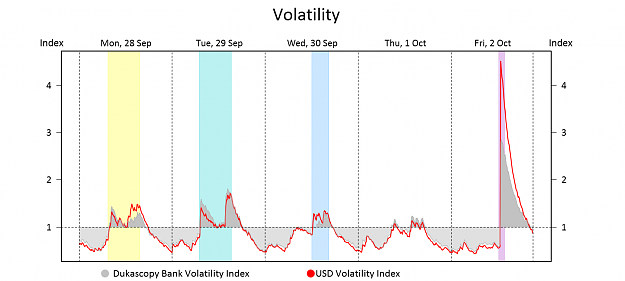

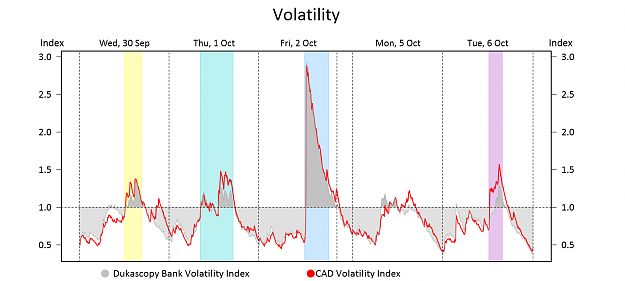

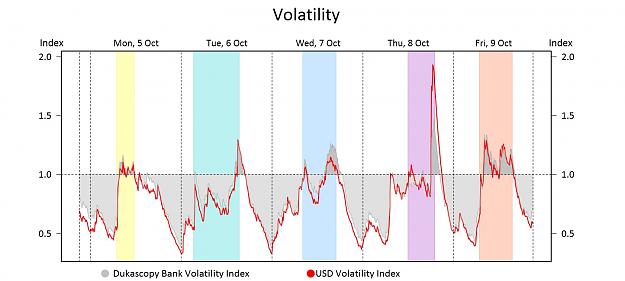

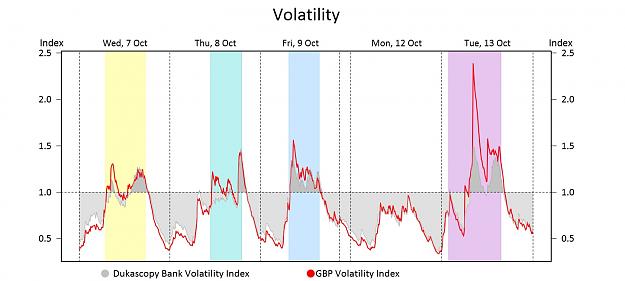

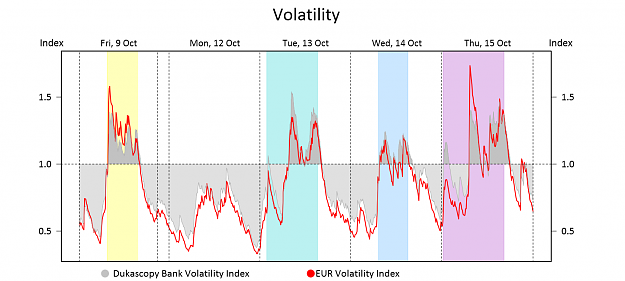

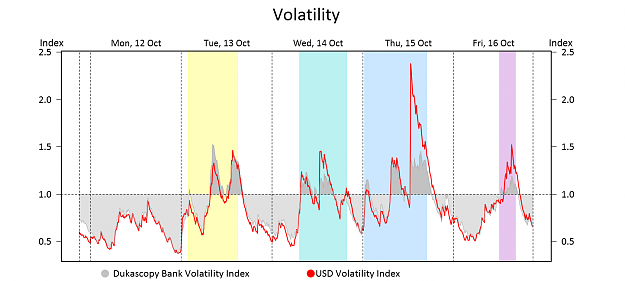

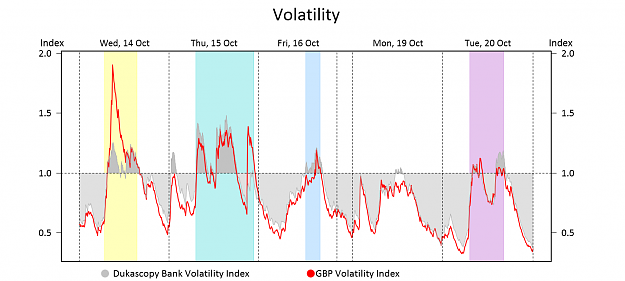

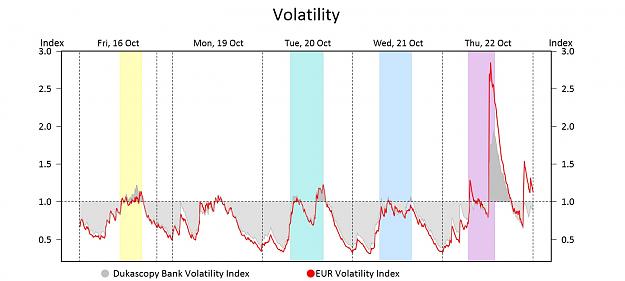

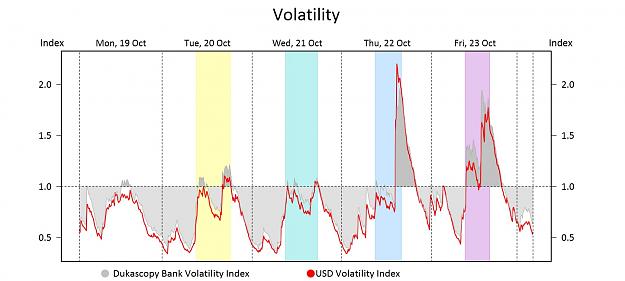

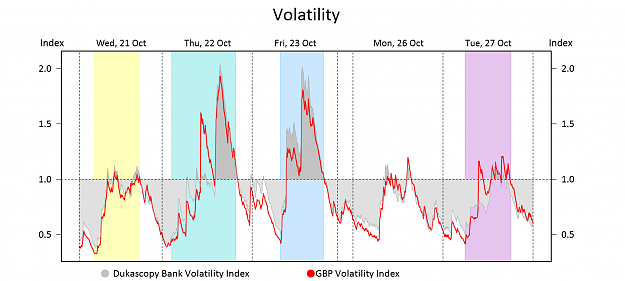

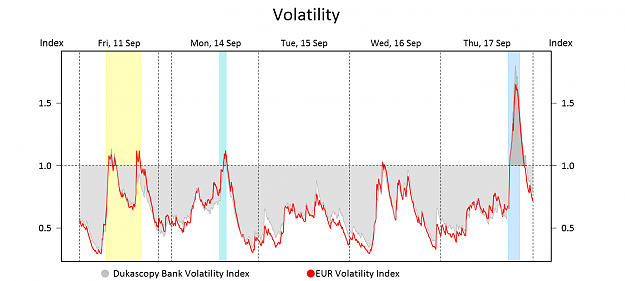

As anticipation of the FOMC meeting grew heavier, activity on the market continued to decline. The portions of elevated volatility lost some more points from the previous period’s already subdued values, with the aggregate reading standing at 6%, and the separate currencies’ measures varying from 3% to 11%. Amid the overall tranquility, even the period’s main event failed to provoke extraordinary splashes of volatility. Here, the highest peak was taken by the Aussie’s measure, but even that reached only as high as 2.3 points.

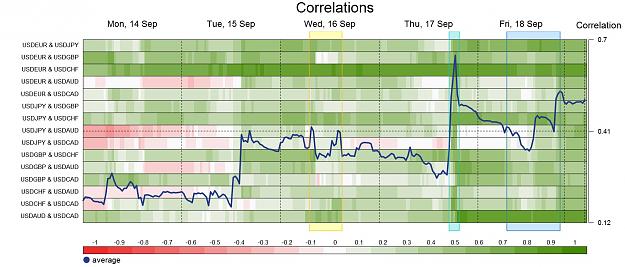

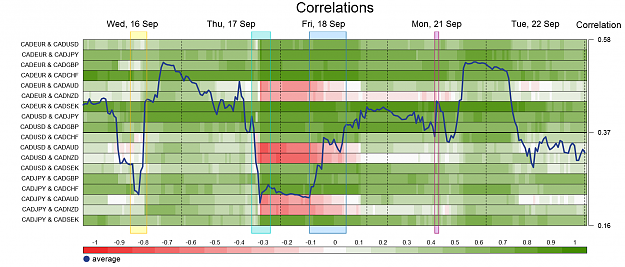

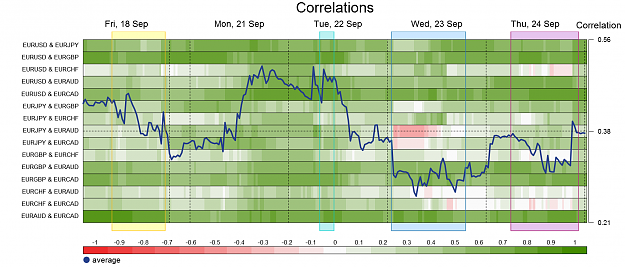

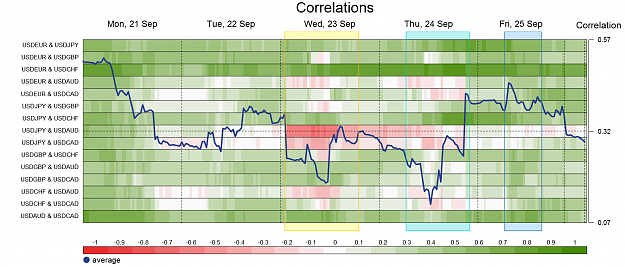

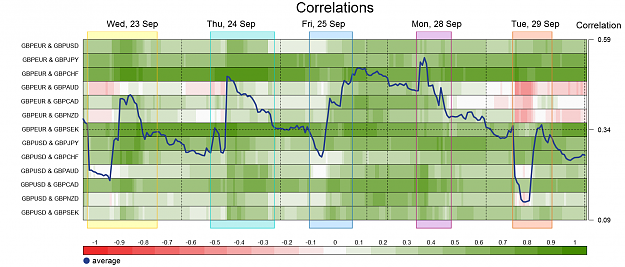

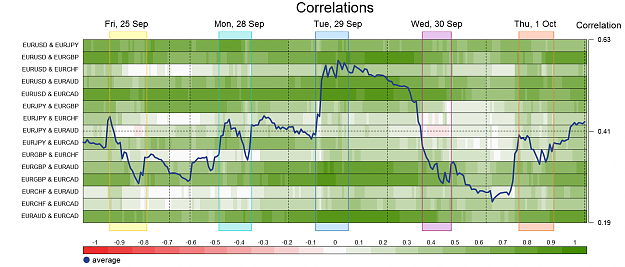

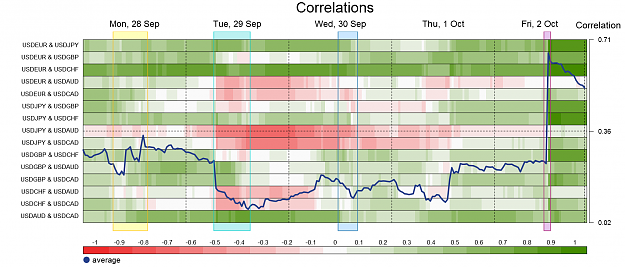

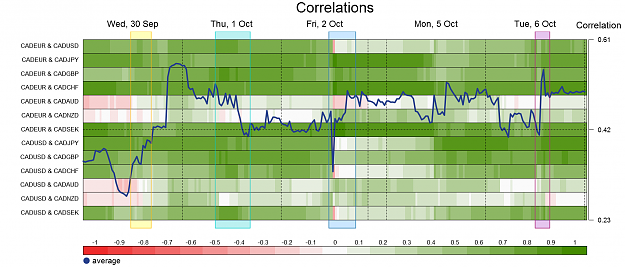

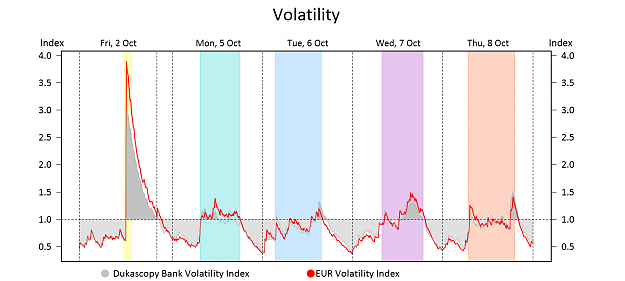

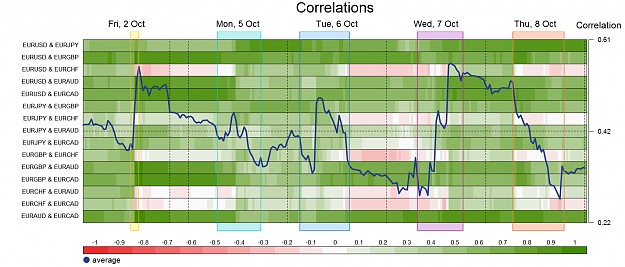

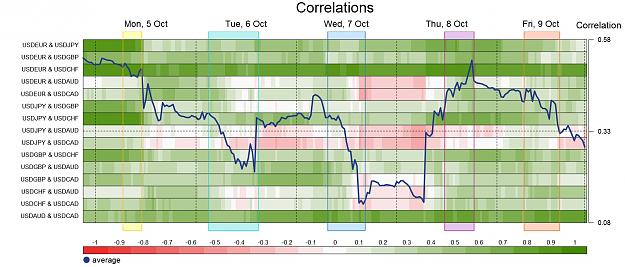

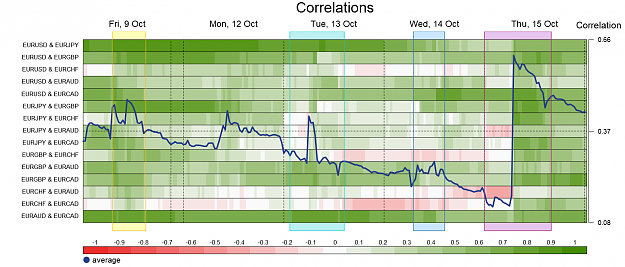

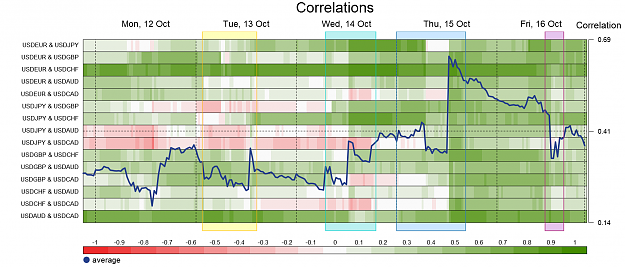

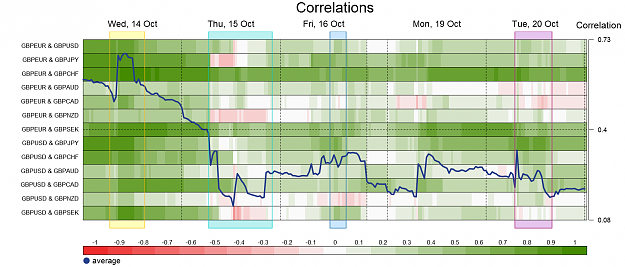

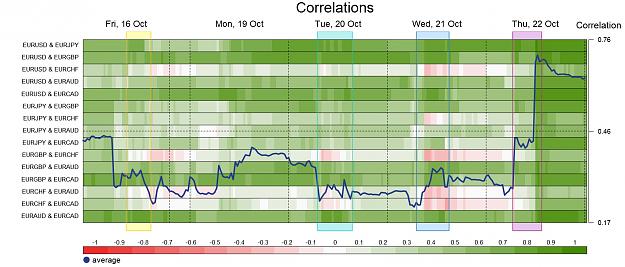

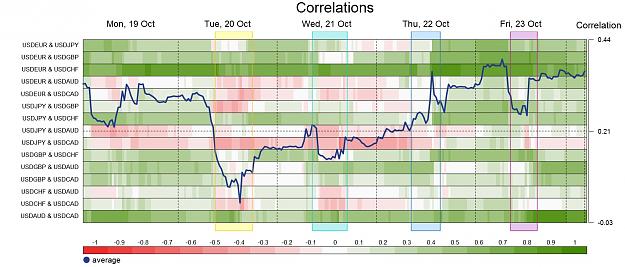

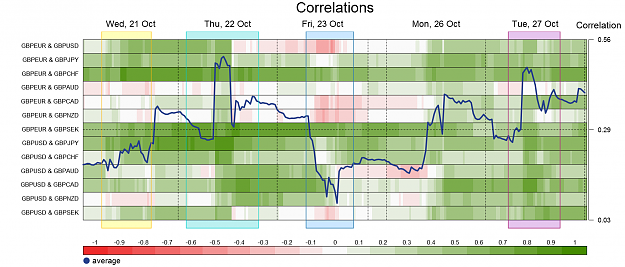

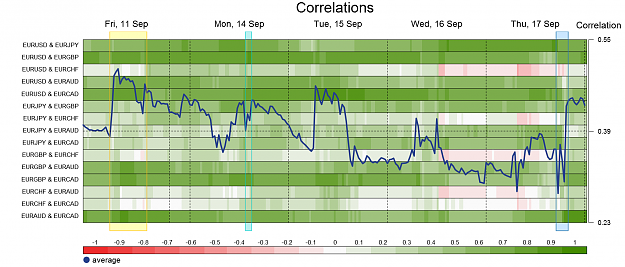

Despite the abnormal tranquility on the market and the main focus of the period being aimed at the US, the Euro’s correlation composite remained firmly within its usual boundaries. Notably, some shifts did happen in the EUR/USD components. Thus, the pair’s bond with EUR/JPY lowered its average to 0.49 from the previous week’s closer-to-long-term 0.68, while the mean correlation with EUR/CHF, on the contrary, moved closer to usual by strengthening from 0.14 to 0.32. Nevertheless, the EUR/USD-EUR/CHF component still brought a substantial amount of red into the aggregate, with its values holding heavily on the downside of the 20-day distribution.

Full research available here.

Attached Image (click to enlarge)

The past period was all about sharp moves, as most of the indexes changed their positions abruptly and otherwise wavered around the reached levels. The main shifts took place on Thursday, when all eyes were on the Fed and its interest rate decision. The USD Index started to lose points a couple of hours before the announcement, and, after the long-awaited hike was pushed further towards the end of the year, went into a dive to the period’s absolute low of 98.5. The Pacific indexes produced the sharpest surges, but also went into the deepest dives after the press conference, yielding more than they managed to gain. Meanwhile, the krona’s gauge, which showed the week’s broadest surge as it burst above its peers with the improved GDP and unemployment data released on Friday, was gaining ground all throughout the blue area, surpassing its Australian counterpart and posting the period’s greatest gain. The only index to show virtually no reaction to Thursday’s events was the pound’s measure, which made its big move amid solid jobs report on Wednesday and kept close to the baseline during the last day of the period.

Attached Image (click to enlarge)

As anticipation of the FOMC meeting grew heavier, activity on the market continued to decline. The portions of elevated volatility lost some more points from the previous period’s already subdued values, with the aggregate reading standing at 6%, and the separate currencies’ measures varying from 3% to 11%. Amid the overall tranquility, even the period’s main event failed to provoke extraordinary splashes of volatility. Here, the highest peak was taken by the Aussie’s measure, but even that reached only as high as 2.3 points.

Attached Image (click to enlarge)

Despite the abnormal tranquility on the market and the main focus of the period being aimed at the US, the Euro’s correlation composite remained firmly within its usual boundaries. Notably, some shifts did happen in the EUR/USD components. Thus, the pair’s bond with EUR/JPY lowered its average to 0.49 from the previous week’s closer-to-long-term 0.68, while the mean correlation with EUR/CHF, on the contrary, moved closer to usual by strengthening from 0.14 to 0.32. Nevertheless, the EUR/USD-EUR/CHF component still brought a substantial amount of red into the aggregate, with its values holding heavily on the downside of the 20-day distribution.

Attached Image (click to enlarge)